Personal Wealth Management / Politics

Scotland’s Election and the ‘Risk’ of IndyRef2

A second Scottish independence referendum isn’t a given, but either way, the impact on UK stocks is likely limited.

Editors’ note: MarketMinder is politically agnostic, favoring no party or politician in any country. We assess political developments solely for their potential market impact.

Scotland holds elections for its semi-autonomous, devolved parliament on May 6, and with the Scottish National Party (SNP) polling well despite a scandal embroiling its current and former leaders, independence chatter is once again running hot. The SNP is reportedly planning to table legislation laying the groundwork for an independence referendum before the election even takes place, likely guaranteeing tough rhetoric dominates the campaign—and driving uncertainty afterward if the SNP wins an outright majority. In our view, it is far too early to assess the probable election results. But even if another independence push gets going, it should have only a limited impact on UK equities.

The independence drive has loomed large over Scotland for over 20 years and dominated the devolved parliament before 2014’s referendum. That vote, in which 55% of Scottish voters elected to remain in the UK, supposedly settled the issue for a generation. Nonetheless, here we are discussing it again, just six years later, thanks to Brexit.

While the UK overall voted 52% to 48% in favor of leaving the EU, 62% of Scots voted to remain, versus just 38% in favor of Brexit. Scottish politicians argue that if England and Wales could pull Scotland out of the EU against the majority of voters’ wishes, that is a meaningful enough change in circumstances to warrant a fresh independence vote. Polls have seemingly agreed, with most showing a majority of Scots favoring independence since mid-2020, although support has seemingly slid in recent weeks. That was enough to convince the SNP that independence is the people’s “settled will,” powering the looming push.

Yet holding a new independence referendum is easier said than done. Unlike EU member-states, the UK has no Article 50-like exit procedure allowing its constituent countries to hold independence referendums at their discretion. While the Scotland Act of 1998 gives its government significant authority over local matters, anything concerning the union of Scotland and the rest of the country is explicitly reserved for the UK national Parliament at Westminster. That means the UK government must approve a request from Scotland to allow it to vote on holding a referendum. Prime Minister Boris Johnson hasn’t tipped his hand on this, instead seemingly preferring to keep the referendum threat alive in order to give Scottish Tories some urgent campaign talking points. But he has on many past occasions reiterated his agreement that 2014’s vote was a once-in-a-generation event.

Failing UK government approval, Scotland could try to hold a referendum without Westminster’s support, allowing the UK Supreme Court to review the case in hopes of a favorable ruling. Some have suggested this alternative, but Catalonia tried this in 2017 and it didn’t go well, which may discourage SNP leadership.

In October 2017, pro-independence Catalan leaders held an independence referendum despite the Spanish government declaring it illegal. The referendum passed, 90% to 10%, but voter turnout was very low due to opposition boycotts and police intervention. The Federal government deemed the results illegitimate and jailed many pro-independence leaders. Importantly, EU leaders also viewed the referendum as illegitimate, deferring to the Spanish government and constitution to resolve the matter.

It is reasonable to expect the EU would react similarly to a Scottish independence referendum that lacks legal or UK government support. That is no small matter. Though the SNP wants independence, it wants world governments—particularly the EU—to view it as legitimate, considering part of the motive here is re-entering the bloc. As a result, Scotland’s options are limited. It would need approval from either the UK government or the courts, which is unlikely to play out quickly given the nature of legal challenges. This would give markets plenty of opportunity to digest the news, sapping any surprise power.

While the prospect of a second referendum may create some uncertainty, the long road ahead likely limits its surprise power over stocks. A sentiment overhang may dampen UK returns if the SNP wins outright in May, but we think the bigger headwind to the country’s equity performance is stylistic.

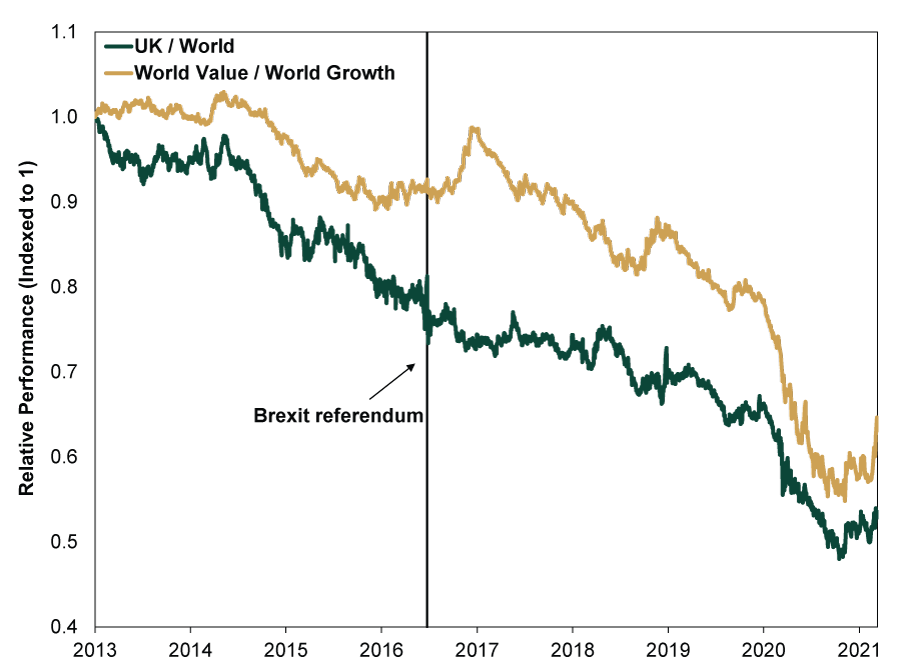

While UK stocks underperformed the world in the runup to 2014’s referendum, it is difficult to parse out how much—if any—was tied to referendum uncertainty. As the green line in Exhibit 1 indicates, UK equity underperformance began much earlier in 2013 and continued well after the vote, despite uncertainty falling. A big reason for this, in our view, is the UK’s heavy tilt to value stocks—particularly Financials and Energy. These sectors were 37% of UK market cap entering 2014, and they lagged badly worldwide.[i] Today, these two sectors still have an outsized footprint in British markets, with Financials and Energy comprising 19.6% and 10.4% of market capitalization, respectively.[ii] Both far exceed the world’s 13.6% and 3.2%.[iii]

This largely explains why UK relative returns have largely mirrored value’s returns relative to growth over the past several years, in our view. As long as Tech and growth stocks are leading worldwide, the UK—which has barely any Tech—likely lags global markets even if referendum uncertainty evaporates in seven weeks.

Exhibit 1: MSCI UK Relative Performance Tends to Track Value’s Performance versus Growth

Source: Factset, as of 3/10/2021. MSCI United Kingdom Index, MSCI World Index, MSCI World Value Index and MSCI World Growth Index, 12/31/2012 - 3/10/2021. Indexed to 1 at 12/31/2012.

When the lines are falling, the UK/World Value are underperforming.

Still, the potential for a second referendum creates a pocket of uncertainty—one of only a few in the developed world, alongside Hong Kong. While it is noteworthy, its impact is likely isolated and short-lived as the issue of Scottish independence remains a localized, legal issue within the UK.

[i] Source: FactSet, as of 3/17/2021. MSCI UK Index Financials and Energy sector weights, 12/31/2013.

[ii] Source: FactSet, as of 3/16/2021. MSCI UK Index Financials and Energy sector weights, 2/28/2021.

[iii] Source: FactSet, as of 3/16/2021. MSCI World Index Financials and Energy sector weights, 2/28/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today