Personal Wealth Management / Market Analysis

Searching for Meaning in Bouncy Tech

For all the ink spilled over Tech's pullback, sector-specific volatility is normal.

How do you know when it's a slow news stretch in the world of finance? Easy: When one sector has a bad day and headlines still haven't stopped talking about it three days later. So it went after S&P 500 Tech stocks fell -2.7% Friday, sparking fears that the trend was no longer investors' friend and this crowded momentum trade had hit a wall, or some such jargoney mumbo jumbo.[i] Media even spilled more pixels Monday, when Tech opened down and finished the day -0.8% lower, a daily move even the media probably wouldn't point out without Friday's.[ii] We wouldn't normally devote space to such short-term swings in one sector, but there is an avalanche of coverage trying to draw forward-looking conclusions, and we believe it is our duty to attempt to set the record straight. One day's volatility simply isn't predictive, even if the sliding sector is the market's year-to-date leader.

Tech has been hogging headlines most of the year-partly because it has done quite well, and partly because five of its largest constituents were responsible for 41% of the S&P 500's year-to-date market cap increase until they took a pounding Friday. That pounding, we're warned, is potentially evidence investors are out of cash or unwilling to "buy the dips," sapping these Tech giants' ability to prop up the market moving forward. Never mind that Tech has had steeper falls since this rally began on February 11, 2016, when the last correction ended. Observers argue those don't count, since they occurred during broad-based drops. Friday was unique, we're told, because it was out of the blue and otherwise a mostly fine day for markets, with 7 of the S&P 500's 11 sectors positive.

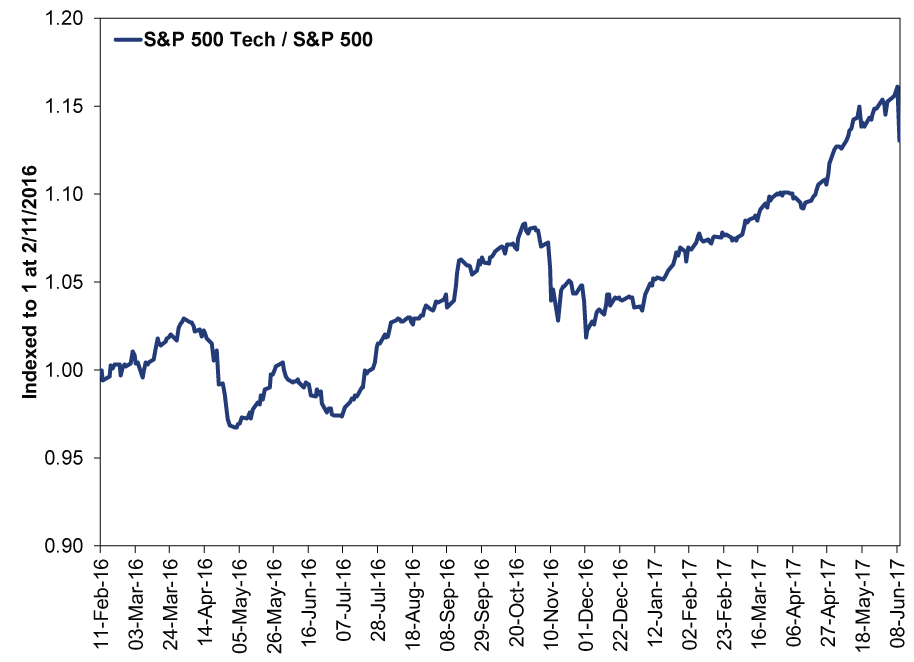

Now, we didn't buy into the "five Tech companies are driving the market while everyone else stinks" story, so don't take any of our next 535 words as an argument for five firms' continued dominance. That isn't what we do. But we also don't think it's fair to declare Tech's longer run dead based on one day. This isn't the only time Tech has had a short burst of underperformance since last February. Exhibit 1 shows the S&P 500 Information Technology Index's returns since February 11, 2016, divided by the S&P 500. When the line is rising, Tech is outperforming. As you'll see, there are steep, deeper drops in November and April 2016. Neither prevented Tech from outperforming moving forward, because past performance does not predict or drive future returns. Often a blip is just a blip.

Exhibit 1: Tech's Relative Returns During This Rally

Source: FactSet, as of 6/12/2017. S&P 500 Information Technology and S&P 500 total returns, 2/11/2016 - 6/9/2017. Indexed to 1 at 2/11/2016.

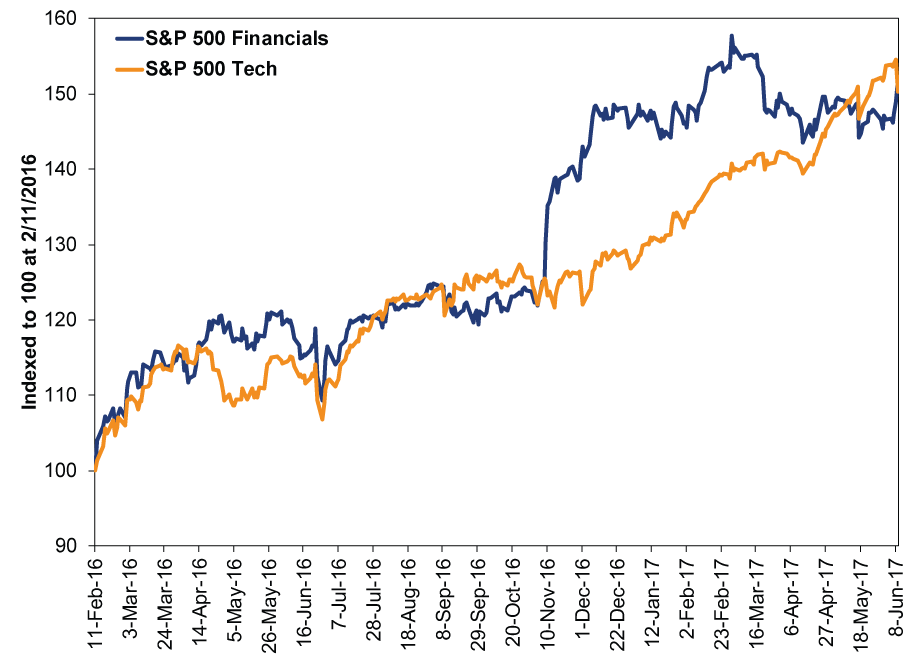

What we find a bit funny is that, for all the chatter about Tech, it is virtually tied with Financials for the title of Best Performing Sector Since This Rally Began. Yet Financials didn't receive nearly as much ink or credit for the S&P 500's gains, perhaps because it's only 14.2% of the index's market cap-still good enough for second-largest, but not as big as Tech's 22.8% share.[iii] Regardless, it seems fairly clear to us that hype is arbitrary.

Exhibit 2: Where Was the Financials Hype?

Source: FactSet, as of 6/12/2017. S&P 500 Information Technology and S&P 500 Financials total returns, 2/11/2016 - 6/9/2017. Indexed to 100 at 2/11/2016.

We've seen all manner of guesses as to why Tech had a bad day, each one as useless for investors as the others. Friday's movements register investors' emotions on one day. That's it! How many times has the broad market had a bad day, only to carry on over the next several months? Volatility happens. It's a fact of life, whether it's broad or sector-specific. Searching for meaning in these swings-good or bad-is myopic and futile.

As ever, we encourage longer-term thinking. Tech firms are big and global, and the global economy is growing-even accelerating in several key markets. S&P 500 tech companies' earnings jumped 17.6% in Q1, trailing only Energy (mathematically impossible to calculate), Financials (18.7%) and Materials (17.8%).[iv] Analysts presently expect another 8.4% in Q2, second only to Energy, and 9.8% for the full year.[v] Stranger things have happened, but it seems difficult to envision any sector's stocks enduring a bloodbath if their earnings are growing apace-particularly when all we keep hearing is that Tech is up only because investors are chasing heat and ignoring sluggish US growth. If investors are actually chasing fundamentals, and the media is too skeptical to realize it, that would seem to us to be a sign sentiment lags reality. That in turn argues for Tech to keep doing fine.

As for those fears that a rally isn't sustainable if the vast majority of stocks aren't joining the party, market breadth-the percentage of stocks outperforming the index average-usually shrinks as bull markets mature. When breadth is high, it usually means small cap is leading-usually early in a bull market, when smaller firms reap the biggest earnings boost from recessionary cost-cutting. Later in the cycle, large cap usually takes the reins, and there are simply fewer big firms than small cap-hence, fewer firms lead. This is a typical, healthy feature of maturing bull markets. When folks so broadly fear the market's usual behavior, in our view, it's likely just one more sign the bull has plenty of room to run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today