Personal Wealth Management / Market Analysis

Searching for Meaning in Tame Times

A flattish start to 2015 has some pundits wondering where US stocks go from here.

US stocks have been impersonating Kansas thus far this year. Photo by Tetra Images/Getty Images.

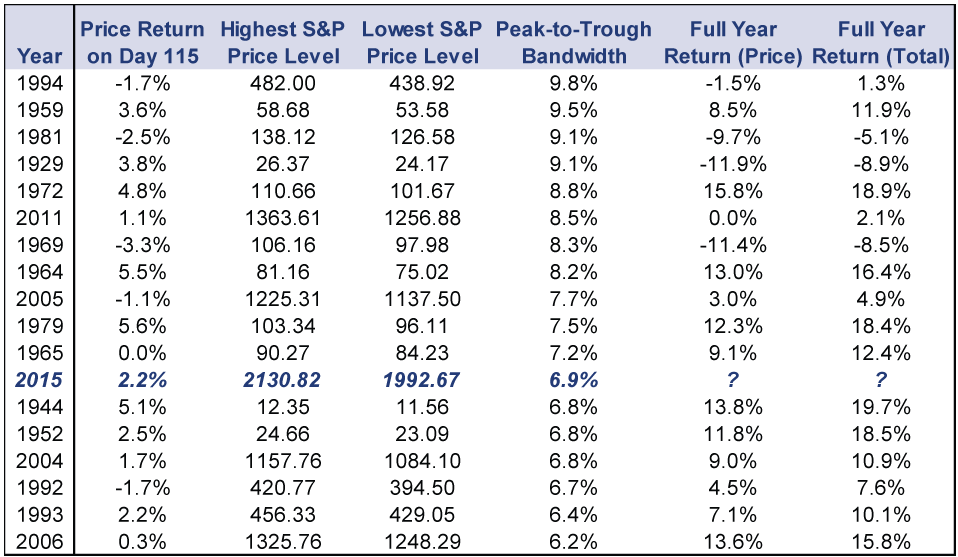

With 115 trading days in the books as of Wednesday's close, 2015 has proven placid for US stocks, with the S&P 500 eking out a small gain year to date while trading in a tight channel between highs and lows. On a price basis, US stocks are up 2.2% year to date (3.2% if you factor in dividends).[i] The year's high was 2130.82 and the low was 1992.67-a measly 6.9% spread between them.[ii] The media-and investors-have noticed, with many pondering this flat, "range-bound" market. Others speculate investors are frozen like "deer in headlights" ahead of a possible Fed rate hike or Greek default or other bad thing.[iii]Recalling 2014, one analyst suggested sideways is the new down, and what we're looking at presently is a correction. (We don't think so.) Still others seem to be adjusting return expectations due to this flatness. But in our view, fixating on how 2015 has begun-and attempting to draw forward-looking implications-is folly. Our advice? Let the herd react to past returns-opt out, then game them.

Yes, it has been a tame start to the year, but it isn't as placid as some suggest. One widely cited analysis claims this is the S&P 500's tightest trading range since at least 1995. But the data are flawed-they compare 2015's 115 days with full-year data from the last two decades. There are between 260 and 262 trading days in every year since 1928, so those earlier years have more than double the opportunity to out-fluctuate 2015.

An apples-to-apples comparison of the first 115 trading days shows 2015 is indeed trading in a tight channel-the seventh tightest since 1928-but tightness isn't so unseen in recent years. Both 2004 and 2006 traded in even tighter ranges thus far in the year, and both had similarly small positive returns at this point. In 2004, the S&P 500 price index rose 1.75% in a 6.8% peak-to-trough bandwidth through the 115th trading day.[iv] 2006 was up a fraction (0.3%) in the smallest bandwidth on record-6.2%.[v]

Yes, both of those years finished with positive returns-double-digit positive returns, no less. (Including dividends, they were up 10.9% and 15.8%, respectively.[vi]) But that doesn't mean tight bandwidth = bullish. There are 17 years with a smaller than 10% peak-to-trough swing at day 115, and there isn't any pattern to them. 1929, 1969 and 1981 are all in that collection, and none were particularly wonderful times to own stocks. On the flipside, 1944 and 1952 were well above average years for stocks. 1992 and 1993 were early in history's longest bull market-an overall excellent time to own stocks. There are some above-average positive years and some ho-hum ones. Not much you can glean from this. Table 1 shows you these "range-bound" years.

Table 1: Years With Peak-to-Trough Moves Less Than 10% on Trading Day 115

Source: Factset, Global Financial Data, Inc., as of 6/11/2015.

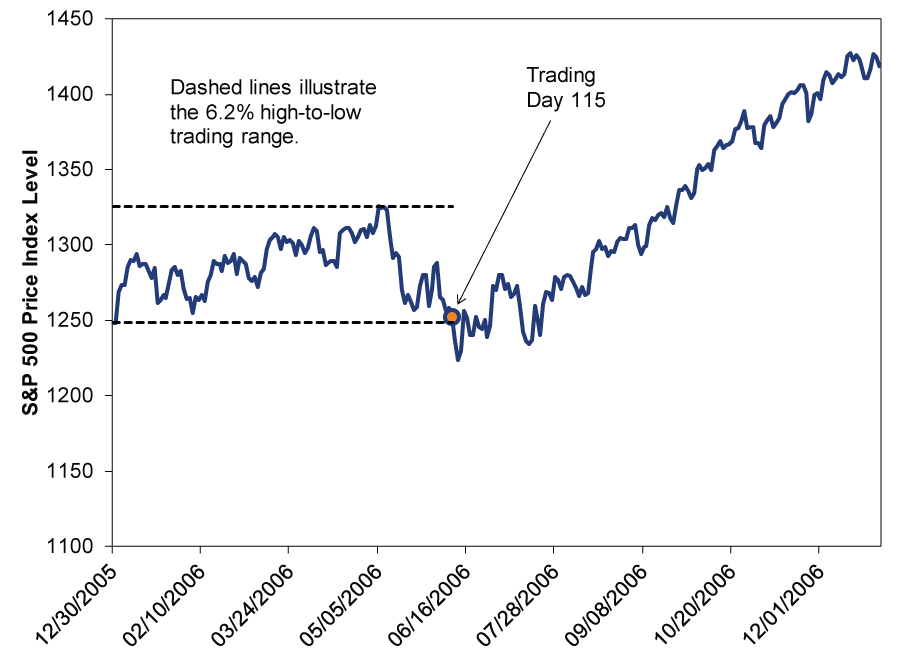

Perhaps one thing you can take away is flattish starts to years don't presage flat returns ahead. 2006 is a good example. Not only was it flatter at this point than 2015, but stocks broke out of the range by falling, only to turn higher and finish up squarely in the double digits. We aren't suggesting a 2006 repeat is in store. We are merely suggesting things are only non-volatile and flattish until they aren't, and stocks can run a long way in about half a year.

Exhibit 2: 2006's Tight Trading Range at Day 115 Didn't Foretell What Followed

Source: Factset, S&P 500 Price Index, 12/31/2005 - 12/31/2006.

However, this won't stop some pundits and investors from allowing their expectations to be swayed by recently ho-hum returns. The American Association of Individual Investors' weekly sentiment survey has recently shown dipping optimism and rising pessimism, which many are connecting to the flattishness. Professionals, too, have a tendency to extrapolate recent market conditions-forecasters remain tepid, expecting mid-single digits returns. Seeing the small gain and tight trading range thus far could inspire more pros to cut their outlook in the coming weeks. In May, Goldman Sachs revised its 2015 year-end forecast for the S&P 500 level down to 2100. Credit Suisse raised their forecast Thursday, but to a modest 4.5% gain by year-end.

Here is another thing you can take from 2015's start: Lowered expectations and reduced optimism are another sign sentiment isn't overextended. Other than that, we'd suggest all the articles drawing conclusions from the flat start to 2015 are much ado about nothing.

[i] Source: Factset, as of 6/11/2015. Global returns are bigger, with the MSCI World up 3.9% on a price basis and 5.0% including dividends (net of Luxembourg withholding tax). And you should both invest globally and look at total (or net) returns. We used US and price a) because that is what the media is citing and b) because there is a much longer data set in this particularly series.

[ii] Source: Factset, as of 6/11/2015.

[iii] Which is a very odd claim, as it makes one think that low volatility is due to fear, which should really confuse folks who think the VIX is the "fear gauge."

[iv] Source: Factset, as of 6/11/2015. S&P 500 price returns and levels, 12/31/2015 - 6/9/2004.

[v] Source: Factset, as of 6/11/2015. S&P 500 price returns and levels, 12/31/2015 - 6/9/2006.

[vi] Frequent readers may recall that our outlook for this year is that double-digit returns are the most likely outcome. However, our forecast hinges on the MSCI World Index Net Returns, which again, are higher. See footnote 1 and invest globally.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today