Personal Wealth Management / Market Analysis

Sector Flash: Financials—US Bank Health Continues Improving

Banks are much healthier than they were just a few years ago and shouldn’t pose a serious threat to economic growth moving forward.

Two years after the credit crisis, many still fear potential macroeconomic fallout stemming from the banking industry. However, as the old adage goes, time heals all wounds—and that’s true for banks. Not only does time allow for recurring income to absorb bad assets and permit borrowers to find solutions to financial hardships (finding a job, home price stabilization, or reducing other expenses), but it also allows banks to adjust balance sheets and organically earn their way to stronger capitalization.

Some argue the industry and politicians have been kicking the can down the road—meaning issues in the banking industry have been ignored and a day of reckoning will eventually arrive. However, in many important ways, the banking industry today is much stronger than it was in 2007-2008, and many issues that arguably exacerbated the 2008 credit crisis have been addressed.

Major changes that have contributed to improving bank health include:

- Banks are profitable again

- Many legacy loans have already been charged off

- Fewer loans are going bad today

- Banks have much more capital

- Banks have de-risked their balance sheets

- Banks once again are relying on core funding (deposits)

The following graphs illustrate these changes and provide some perspective on how far banks have come since 2008.

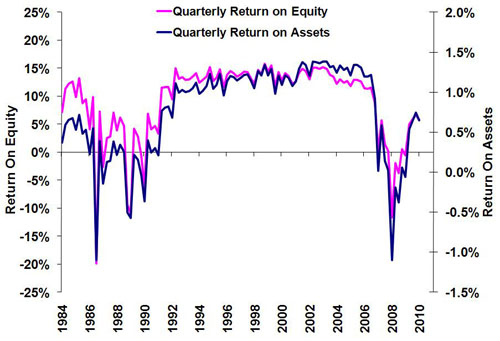

1. Banks are profitable again. US banks have posted $79.5 billion in profit over the last four quarters

Exhibit 1: US Banking Industry Return on Equity and Assets

Source: FDIC, as of 12/31/2010.

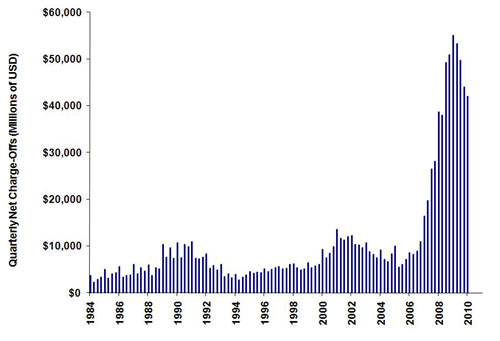

2. Many legacy loans have already been charged off. Cumulatively, US banks have absorbed $538 billion in bad loans since 2007.

Exhibit 2: Quarterly Net Charge-Offs

Source: FDIC, as of 12/31/2010.

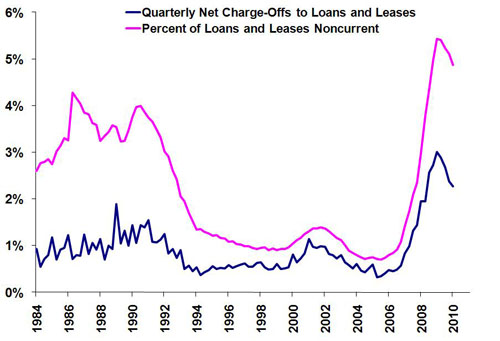

3. Fewer loans are going bad today. The noncurrent loan ratio peaked in Q4 2009 and has since trended lower.

Exhibit 3: Quarterly Net Charge-Offs and Noncurrent Loans and Leases

Source: FDIC, as of 12/31/2010.

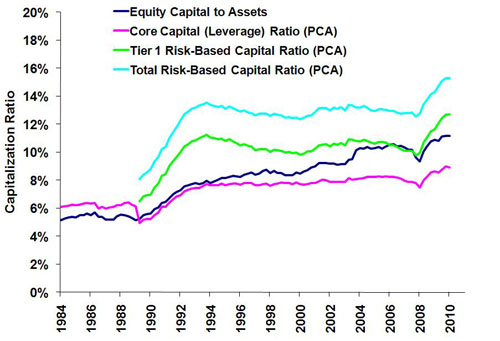

4. Banks have much more capital. US financial companies have raised $832 billion* in fresh capital since the onset of the crisis.

Exhibit 4: Various Measures of Bank Capital Ratios

Source: FDIC, as of 12/31/2010.

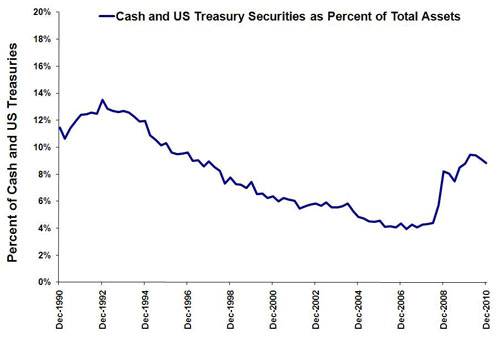

5. Banks have de-risked their balance sheets. Since early 2007, banks have increased their cash and US Treasury securities holdings by $700 billion.

Exhibit 5: Cash and US Treasury Securities as a Percent of Total Bank Assets

Source: FDIC, as of 12/31/2010.

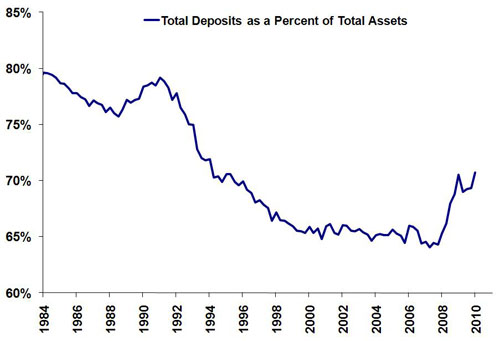

6. Banks once again are relying on core funding (deposits). Deposits are a much more reliable source of funding than other wholesale sources.

Exhibit 6: Total Deposits as a Percent of Total Bank Assets

Source: FDIC, as of 12/31/2010.

Banks have returned to profitability, they are very well capitalized, asset quality is improving, many bad assets have already been absorbed, funding has reverted back to traditional means and banks are starting to lend. Now, bank failures will likely occur moving forward based on company specifics, and none of these improvements mean bank stocks in general are poised for outperformance ahead. The industry continues to face regulatory and sentiment headwinds for the near future. But overall, the industry is stronger now than it has been in quite awhile, and, barring major changes not currently on the horizon, bank health is unlikely to hinder macroeconomic growth moving forward.

*Source: Bloomberg

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today