Personal Wealth Management / Market Analysis

Seeing Through the China-Slowdown Smog

Despite some widely reported weakness in China and elsewhere in Asia, global manufacturing remains in the black.

Global markets tumbled again Tuesday, and once again, headlines blamed weak Chinese manufacturing data, fretting the impact on China's major trading partners as manufacturing indexes throughout Asia fell and South Korean exports plunged. Yet for all the chatter, there is nothing really new or surprising here: China's latest readings met expectations and are largely in line with the last three years, and weakness in some Asian and commodity-dependent nations began creeping up a while back-South Korean and Taiwanese GDP slowed in Q2, after all. Moreover, while weak spots steal headlines, on balance, the latest numbers point to global growth. Seems to us markets are still trying to shake out the fearful, though only time will tell whether the correction re-tests last week's lows. Either way, we believe the bull market remains ongoing, with plenty of fundamental support.

The headline-stealing numbers were China's manufacturing purchasing managers' indexes (PMI) for August, which deteriorated and signaled contraction, with readings below 50. The Caixin/Markit PMI, which includes small private firms, hit 47.3, the lowest in more than six years. The official PMI, which focuses on large state-run firms, hit 49.7. South Korean, Indonesian and Taiwanese PMIs also registered contraction, while Vietnam's remained in expansion but slowed from August. Along with the -14.7% year-over-year slide in South Korean exports, all were deemed evidence China's slowdown is starting to hit the world.

But all these numbers come with several caveats. PMIs are surveys that give a rough estimate of the percentage of firms growing, but they don't measure the magnitude of growth. France's manufacturing PMI, for instance, has contracted often since late 2013, yet French industrial output and GDP are up. China's manufacturing PMIs have bounced around 50 since 2012, but its economy has decelerated only modestly. Even if you don't buy official Chinese data, cross-readings from most of the rest of the world don't indicate a hard landing in the world's second-largest economy. Korea being an obvious exception, exports from many countries to China have grown year to date versus 2014.

China's PMIs come with an extra asterisk, as the government ordered widespread factory shutdowns to improve air quality around Beijing in advance of big military parades to commemorate the 70th anniversary of WWII's end on Thursday. China has a long history of shutting down industry to clear the air for major events, triggering temporary slowdowns. But, when factories get the all-clear, smog resumes and growth reaccelerates.

Finally, these PMIs cover manufacturing only. Not agriculture. Not mining. And, most importantly, not services-now the biggest chunk of China's economy and by far the biggest slice of developed-world output. Service PMIs will trickle out over the next couple days, but China's are in already, and both the official and Caixin services gauges remained in expansion.

South Korea's disappointing August trade figures have some mitigating factors as well. The biggest declines centered in exports of petroleum products and container ships, which fell -40.3% y/y and -51.5% y/y, respectively. Falling oil prices wear much of the blame for the former, and we suspect the global container ship supply glut has a lot to do with the latter-neither are signs of global economic weakness. Notably, exports of smartphones and semiconductors, two of Korea's biggest tech-related offerings, rose. So it seems odd to argue Korea is a victim of anything other than years of overzealous production in two industries-by now, well-known global phenomena.

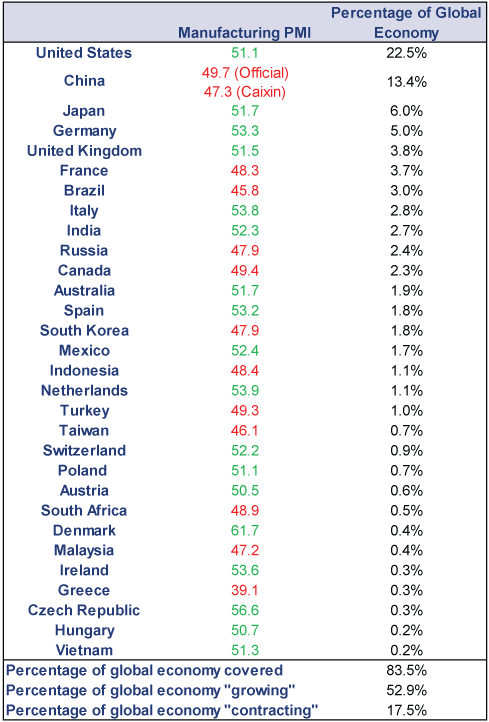

Still, for what it's worth, when you consider all the manufacturing PMIs released Tuesday, the good far outweighed the bad. Exhibit 1 shows all the PMIs we could round up, along with each country's share of the global economy. Over half the world reported growth, keeping JPMorgan's global manufacturing PMI above 50 (actual reading was 50.7). China aside, contractions were concentrated in small countries. For all the fear of weak Chinese demand hurting Germany-which counts China as its fourth-biggest export market-Germany's PMI rose from July. On balance, the world's factories are growing, and while manufacturing represents a minority of the global economy, if we were actually heading into a global recession, we would expect way more red on this table (and, likely, deeper in the red readings).

Pockets of strength and weakness throughout the world are nothing new, and it seems the strong are pulling the weak along, which should be plenty good enough to help global growth surpass expectations for a painful slowdown.

Exhibit 1: August Manufacturing PMIs

Sources: IMF, Markit, Institute for Supply Management, National Statistics Bureau of China, SVME Purchasing Managers Association, South Africa Bureau for Economic Research, DILF and the Hungarian Association of Logistics, Purchasing and Inventory Management. August 2015 Manufacturing PMIs and nominal GDP for 2014, as of 9/1/2015.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today