Personal Wealth Management /

Selling Retail Short?

What can we glean from the latest retail numbers?

Ladies and gentlemen, step right up to see the latest US economic data report! This week’s headliner—retail sales! Reviews have been mixed, but critics seem to be generally OK with the showing. And for good reason: Though overall September retail sales fell -0.1% m/m—primarily due to the -2.2% drop in auto sales—a look under the hood confirms sales are stronger than the headline figure suggests. Rather like the broader US economy—another indication reality is stronger than most investors appreciate.

Excluding car sales, retail sales grew 0.4% m/m, making September’s month-over-month growth the third fastest this year. Electronics (+0.7% m/m) and food and drink (+0.9% m/m) grew fastest, and 9 of the 13 major categories showed increases. Discretionary spending! These categories wouldn’t be leading the charge if the economy were weak or weakening—folks would be cutting back, not upgrading their smartphones and eating out. Nor, too, would retail sales (including autos) be up 2.6% for the year. Robust? No. But growth—and growth is better than many expected, not to mention better than many expect looking ahead.

And the auto sales drop isn’t necessarily a sign of weakness—seasonal factors may actually be at work. Labor Day fell earlier than usual this year--the long weekend's Friday andSaturday, typically big for auto sales--fell during August. That isn't to say September auto sales would have grown if some of the holiday demand hadn't been pulled into the prior month, but it does show how small quirks like a calendar page can influence monthly results.

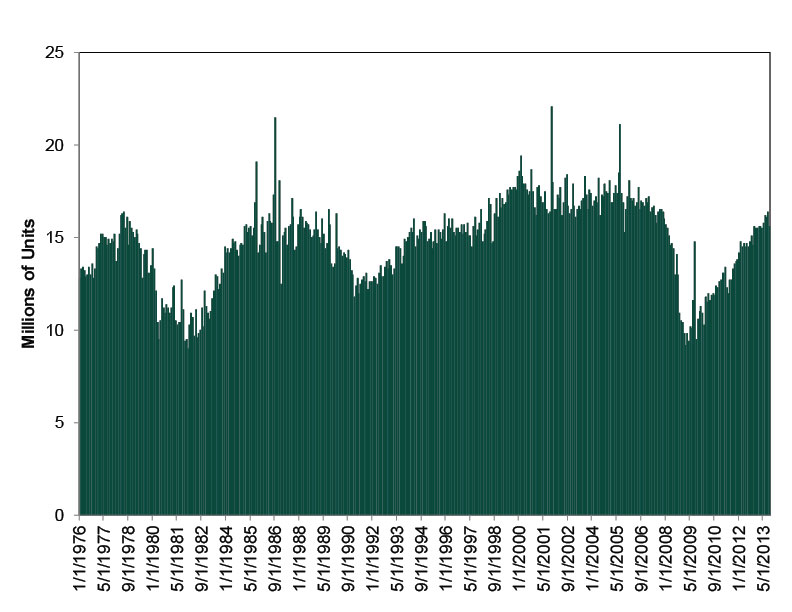

That’s just one reason we’d suggest looking at longer-term trends instead of getting hung up on one monthly data point. For one, current sales volumes are in line with previous cycles. (Exhibit 1) US auto sales have been strong this past year, particularly from June through August and have grown nicely throughout this entire expansion, even with some pretty big short-term dips along the way. September’s dip seems likely to prove a similar blip, not the beginning of a trend. Especially with fundamentals broadly (e.g., high and rising incomes and still-ultra-low interest rates) pointing to a rather favorable environment looking ahead.

Exhibit 1: Monthly US Auto Sales (Units of Vehicles Sold)

Source: St. Louis Federal Reserve, as of 10/30/2013.

Retail sales are just one piece of data that have grown on balance, though fitfully, throughout the year—rather like our broader slow-growing US economy. Yet investors continue to shrug off overall growth and instead fret what may lurk around the corner. Maybe it’s because headline data haven’t been robust—taking a deep look at each category’s underlying components is hard work, so many folks just accept headline results at face value. Sure, this time, media outlets looked past the headline figures and stripped out autos to find the underlying strength. But how often have they done so with lackluster reports on durable goods? Personal consumption? Manufacturing PMIs? Services PMIs? Industrial production? If media doesn’t tell the full story, it’s exceedingly difficult for folks to appreciate it.

Especially considering what folks do get from headlines. Like, say the fear (eventual) tapering back of quantitative easing (QE) will knock the economy off its “fragile” recovery track, thinking growth has been sustained by the Fed’s stimulus. Or, before its resolution two weeks ago, worries a breach of the debt ceiling—and a US default—would send markets into a tailspin. With fear abundant and economic growth—along with rising corporate earnings and revenues and a reaccelerating global economy—so little appreciated, it seems safe to say investors’ expectations are far below reality. This bull market still has a big wall of worry to climb.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today