Personal Wealth Management / Market Analysis

Seven Years Ago Today

A bull market was born.

Seven years ago today, on March 9, 2009, these were some of the top financial headlines:

Dow 5000? There's a Case for It

Obama's Radicalism Is Killing the Dow

UK Says Markets Need Crisis Plan

China Warns of Severe Fiscal Conditions

New Fears as Credit Markets Tighten Up

Collapse of the Financial Sector Harder, Deeper Than Tech Wreck

World Bank: Economy Worst Since Depression

Japan's Nikkei 225 Now at a 26-Year Low

Sarkozy Provokes Anger With Luxury Holiday in Mexico

On the next day, March 10, 2009, stock returns looked like this:

Source: FactSet, as of 3/9/2016. Index total returns on 3/10/2009. MSCI World and S&P 500 returns are in USD; all others are in local currency to remove the impact of currency swings. MSCI World returns are net of foreign withholding taxes; all other returns include gross dividends.

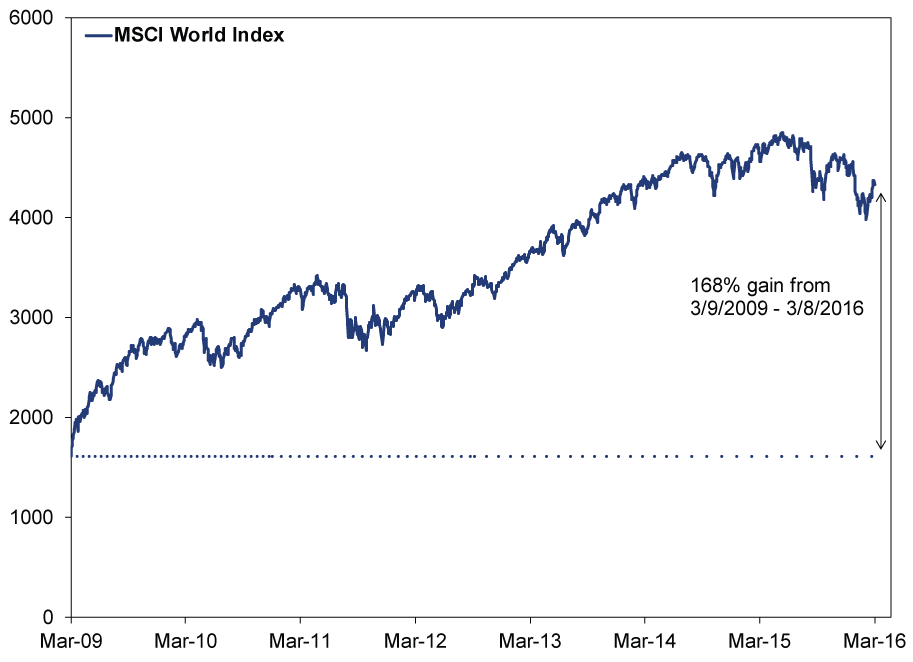

No one knew it then, but the next seven years would look like this:

Source: FactSet, as of 3/9/2016. MSCI World Index with net dividends, 3/9/2009 - 3/8/2016.

The ride has been bumpy, with six corrections and numerous smaller pullbacks along the way, but stocks have rewarded those who followed the sage advice of Warren Buffett and others[i] and hung on when the proverbial blood was in the streets. Sometimes the best time to own stocks is when it feels like the absolute worst, scariest thing to do. Back in late 2008 and early 2009, people feared the entire stock market could go to zero. Huge daily drops unnerved investors everywhere. It felt like a rollercoaster, with nothing to hang on to.

But then the tide turned. It always does. After all, for every buyer, there is a seller, and it doesn't take much for a bidding war to start pushing prices up. You don't need a wealth of good news. The economy can still be in recession, as it was in March 2009. Earnings can still be awful. But if even a few people see the potential for a bright future ahead and smell a bargain, that can be a powerful force lifting markets higher. Bull markets, as the late great Sir John Templeton said, are born in pessimism. The deepest possible end-of-the-world pessimism. They always have been and probably always will be.

These lessons are every bit as relevant now as they were seven years ago. It has been nearly 10 months since world stocks notched their most recent all-time high on May 21, 2015[ii], and they're still -10.8% below that peak despite some nice gains since February 11. Even tepid optimism is rare. Most observers expect dreary times ahead, citing a sluggish economic outlook, falling earnings, recessions in commodity-heavy nations, slowing growth in China, negative interest rates, the end of quantitative easing in the US, political risk in the US (insert any Presidential candidate's name here) and the UK (potential Brexit), and flatter yield curves. Many are fatigued with middling growth, seemingly stalled-out markets and low yields everywhere. Few are forecasting the apocalypse, but "Why should I own stocks?" is nearly as common a question as it was seven years ago.

If you're a long-term investor in need of equity-like returns for some or all of your portfolio, here is the answer: Getting those returns requires participating in bull markets, so not owning stocks is one of the biggest risks you can take. Right now, we think it would be an unwise risk to take because despite the volatility, despite the rampant skepticism, we believe we're still in a bull market. We expect historians to eventually look upon today as this bull's seventh birthday. Lengthy corrections aren't the most common thing in the world, but they aren't unheard of. After stocks hit a cyclical high in early May 2011, two corrections struck within days of each other, and stocks didn't hit another high for more than 16 months. Patience rewarded then, and we think it will do the same now.

Contrary to what you'll read most elsewhere, stocks have a lot going for them. Leading Economic Indexes from most of the developed world signal continued expansion, which should support revenues and earnings globally. Outside the Energy sector, earnings are growing-2.9% y/y in Q4 for the S&P 500's other nine sectors, and 6.2% for the year overall (compared to -3.4% y/y in Q4 and -1.1% overall when Energy is included).[iii] When oil prices stabilize and Energy earnings stop sliding, growth elsewhere should become readily apparent, lifting investors' spirits in the process. As for yield curves, while they've flattened in the US and UK, they still remain positive, and so far that appears to be good enough to stoke lending and money supply growth. Credit markets are flowing, and healthy firms have easy access to the capital they need to invest and grow. Corporate balance sheets are as cash-rich as they've ever been. Regulatory uncertainty in Health Care and US and UK Financials is largely in the rearview mirror, and gridlocked governments in both nations should keep regulatory risk low over the foreseeable future. That's true even with the US election and specter of potential Brexit on the horizon. Neither is as much of a fundamental issue as most believe. In or out of the EU, the UK is a strong, economically open nation with deep capital markets and a strong will to trade freely with as much of the world as possible. And regardless of who wins the US Presidency on November 8, a divided Congress likely provides a strong check on executive power and keeps legislative risk low. And over in Emerging Markets, China keeps adding huge sums to global GDP even with slower growth rates, and commodity-importing nations are growing nicely.

Enduring short-term volatility is the price we all must pay to capture stocks' long-term gains. There are always trade-offs. But the long-term rewards, in our view, are well worth the near-term dips and blips.

[i] We raise a glass to President Obama, who said the following on March 3, 2009: "What you're seeing now is, profit and earning ratios are starting to get to the point where buying stocks is a potentially good deal if you've got a long-term perspective on it." Now, a "profit ratio" isn't a thing, and price-to-earnings ratios were actually quite dismal, but it was indeed a very good time to buy.

[ii] If you're reading this in the UK, eurozone or Canada, your most recent all-time high was April 10, 2015; April 15, 2015; or December 29, 2015, respectively. Currency swings always add a wrinkle. Point of trivia: For UK investors, the bull market actually began on March 6, 2009.

[iii] FactSet, Earnings Insight for the week ending March 4, 2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today