Personal Wealth Management / Market Analysis

Shares Are Getting More Scarce

Fewer IPOs bullishly keeps equity supply in check.

Over seven years into the bull market, as US stocks flirt with all-time highs, fewer companies are going public. As a result, revenue from equity-based investment banking is at a 20-year low. But what's bad for banks is good news for investors: Net stock supply is falling-and that is bullish.

Through initial public offerings, privately held firms raise capital by creating shares and selling them to the public. But lately, this is happening less often. With borrowing rates at generational lows and venture capital firms and other private equity investors seeing big opportunities in the start-up arena, companies can raise capital easily and cheaply these days without going public. And they're doing this in droves, leading to fewer IPOs. Also, incentives to go public aren't what they used to be, adding to the dearth in IPO activity. Investor sentiment isn't hugely positive and market returns have been tepid, suggesting this might not be the best time for private ownership to sell and reap the biggest bang. Sarbanes-Oxley adds another wrinkle. By imposing a host of requirements on publicly traded firms in an attempt to prevent accounting misdeeds-including holding CEOs criminally liable for any inaccuracies in corporate reporting-privately held firms have less motivation to go public. At least for now, IPOs are more of a vehicle for early investors to cash out than for firms to raise working capital. With so much perceived growth potential for some of the most established, profitable private firms-and with so much liquidity sloshing around for new investments-investors probably see it as worthwhile to hang on and wait for a higher payout down the line.

And the numbers bear this out. According to FactSet, 78 firms have gone public so far this year, with $14.7 billion of new shares coming to market. That's down from 155 firms over the same period in 2015, which raised $30 billion. In 2014 through September 22, 227 companies tapped the IPO market, increasing overall stock supply by $74.4 billion.[i] Secondary offerings-publicly traded firms selling additional shares-are also down, as firms are sitting on record amounts of cash and raising more capital through the bond market due to ultra-low borrowing rates. This means less revenue for banks that underwrite new stock issuance. This doesn't mean, though, that investors should shun banks that engage in investment banking. Bond underwriting is booming, as cheap borrowing rates are fueling rising bond issuance. Also, the current landscape for equity underwriting may improve as the bull continues to mature. If so, investment bank stocks will likely anticipate such a shift.

But if IPO activity remains subdued, this is bullish for stocks. As is the case with any other asset, stock prices are a function of supply and demand. Over the short run, supply doesn't vary all that much, as the forces that drive supply changes are time-consuming and telegraphed well in advance. (Exhibit 1)

Exhibit 1: Drivers of Stock Supply

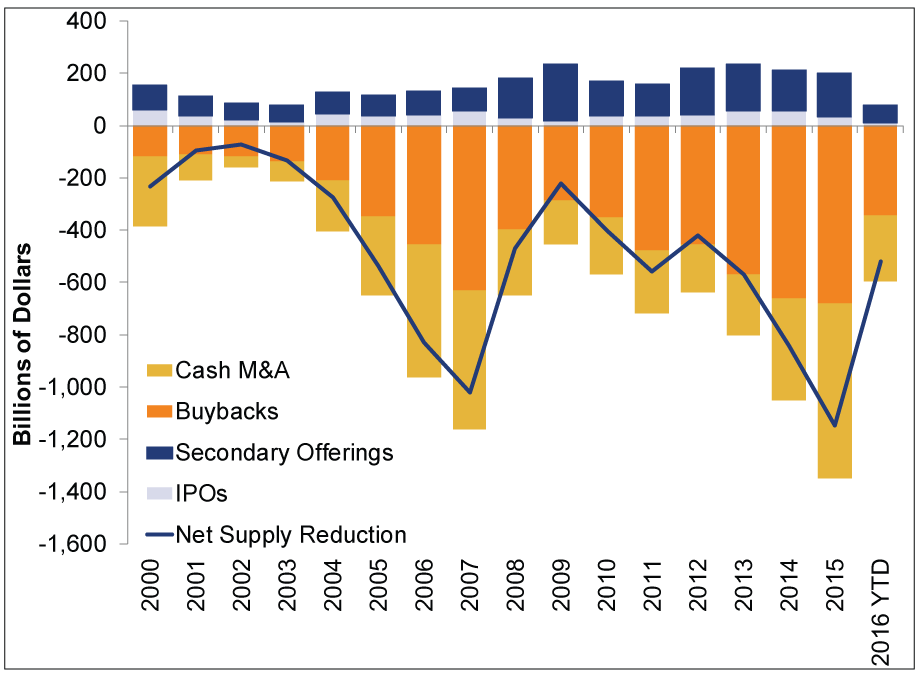

Hence demand holds more influence over stock prices in the short term, as investors respond to economic and political developments-often overreacting-causing sentiment, and thus stock prices, to be bouncy. Over the long term, though, stock supply holds more sway. If IPOs and secondary offerings boom, and companies issue lots of stock as part of employee compensation, overall supply can grow if these activities outpace the forces that shrink supply. Conversely, if cash-rich firms buy back a lot of their own stock or acquire lots of other publicly traded firms with cash-eliminating these shares-while many established privately held firms opt not to go public, overall stock supply likely contracts. This is exactly what's happened over the last few years. Stock supply is shrinking by hundreds of billions of dollars per year. (Exhibit 2)

Exhibit 2: Net Stock Supply Is Shrinking

Source: FactSet, as of 9/23/2016. US IPOs, secondary offerings, buybacks and cash M&As, 1/1/2000 - 6/30/2016. Buyback data for Q2 2016 are projected.

Of course, shrinking supply doesn't necessarily mean stocks will soon surge. We've had a backdrop of positive fundamentals and shrinking supply for most of this bull market. The last couple years, the combination of uncertainty and skepticism has weighed on returns. But that being said, tepid IPO activity is a positive fundamental factor and a sign investors remain entrenched in skepticism-a long way from euphoria or even optimism. If history holds, that implies a lot more bull market-in time and upside-ahead. Hence, investors should cheer slow IPO markets, not fear them.

[i] Source: FactSet, as of 9/23/2016. Total initial public offerings and gross proceeds, as of the offer date. 1/1/2014 - 9/22/2014. 1/1/2015 - 9/21/2015. 1/1/2016 - 9/20/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today