Personal Wealth Management / Market Analysis

Shinzo Abe’s Unstimulating Stimulus

Japan’s new $117 billion stimulus package may provide a short-term boost, but it doesn’t address Japan’s long-running economic issues.

New Japanese PM Shinzo Abe fulfilled a key campaign pledge last Friday, when he unveiled a ¥10.3 trillion ($117 billion) fiscal stimulus package containing earthquake recovery and damage prevention public works projects, measures to support small businesses and the first defense spending increase in a decade.

Officially, the package is a supplementary budget for fiscal 2012/2013, which ends March 31. Abe plans to release the 2013/2014 budget by January 31—given his campaign pledges, further stimulus wouldn’t surprise. Whether it’ll work, however, isn’t clear—the government estimates these measures will add 600,000 jobs and 2% to GDP, which may be a touch optimistic.Still, these measures could carry enough short-term pop to help lift Japan out of its latest recession.

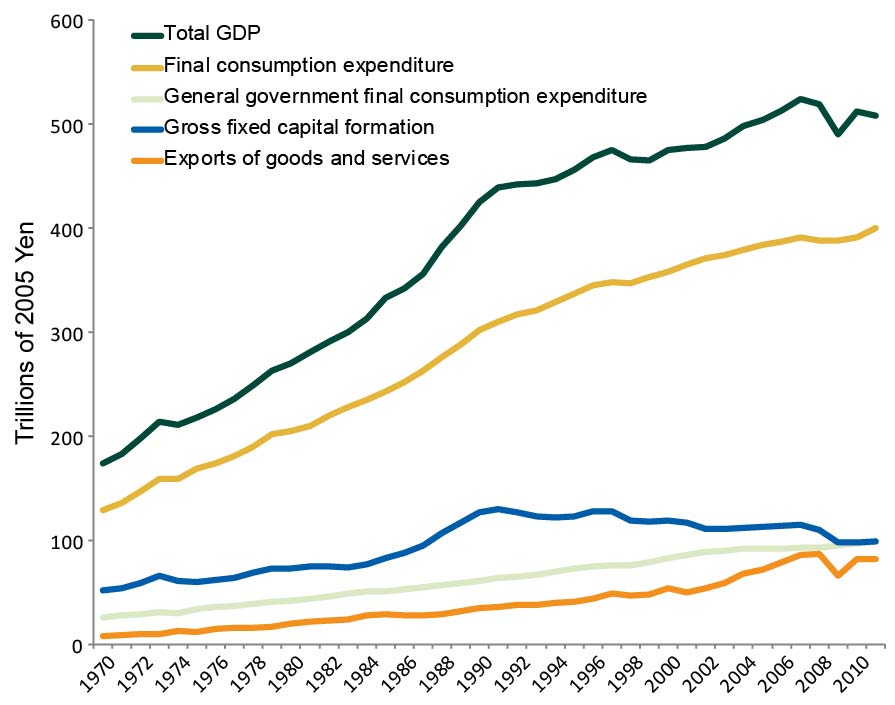

However, stimulus does nothing to address the structural issues that have long plagued Japan’s economy, like waning productivity, weak demographics, narrow labor force participation, high agricultural trade barriers and the negative feedback loop between bank holding companies and their unprofitable subsidiaries. Hence the economy’s lackluster performance over the past 20 years despite rising government spending—private-sector investmenthas fallen since1991 (see Exhibit 1).

Exhibit 1: Japanese GDP and Select Components (1970 – 2011)

Source: UN Statistics Division, as of 01/14/2013.

So why keep trying to boost the economy through fiscal stimulus? Stimulus does have its time and place, and it can give the economy a shot in the arm during a recession. Japan’s latest recession began in Q2 2012, and data suggest it continued through year-end. Perhaps more importantly though, stimulus is popular. According to polls released Monday, 68% of voters approve of Abe’s cabinet and 66% favor his economic policy plans. With elections in the upper house scheduled for July, Abe’s likely looking to curry enough favor to his Liberal Democratic Party to retake the chamber.

Thus, we can likely expect Abe to doggedly pursue his other economic pledge: unlimited monetary easing. Since taking office, he’s pressed the BOJ to increase its annual inflation target from 1% to 2%, adopt a 3% nominal GDP growth target and a ¥90 to the dollar exchange rate target, and stop paying on excess bank reserves. Though the BOJ has full independence and autonomy—important features of any well-run central bank—Abe’s administration released a statement saying “we’ll build a framework for strengthening cooperation between the government and the Bank of Japan. ...We strongly expect the BOJ to conduct aggressive monetary easing with a clear price target.” Whether that means Abe will try to amend the BOJ’s charter or replace current governor Masaaki Shirakawa when his term’s up in April isn’t clear—and bears watching, as infringing on central bank independence is a perilous path.

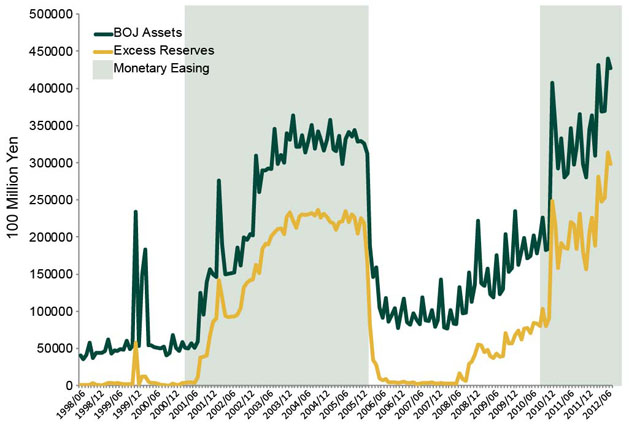

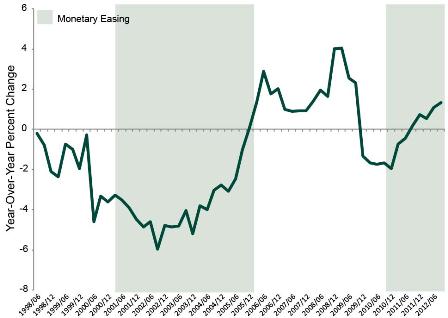

Setting aside the potential means to the end though, aggressive monetary easing would likely have a limited impact. Japan’s current monetary policy isn’t exactly hawkish. Interest rates have been near zero since 1999, and the monetary base has tripled since then. The current QE program, Comprehensive Monetary Easing, launched in November 2008 and is up to ¥101 trillion (¥25 trillion in government-backed loans, ¥66.5 trillion in government bond/bill purchases and about ¥9.5 trillion in other securities). But lending’s been weak while bank reserves have skyrocketed. A similar phenomenon occurred during Japan’s first QE program, which ran from March 2001 through March 2006—reserves rose and lending fell (Exhibits 2 and 3).

Exhibit 2: Bank of Japan Assets and Excess Bank Reserves

Source: Bank of Japan, as of 01/14/2013.

Exhibit 3: Japanese Lending (Year-Over-Year Change)

Source: Bank of Japan, as of 01/14/2013.

As a result, monetary easing hasn’t much spurred growth or inflation—nominal GDP remains well under its 1997 peak. Simply removing the 0.1% payment on excess reserves likely wouldn’t change this—risk-averse banks would probably just shift more assets into Japanese debt, where they can earn a fine real return despite low nominal yields, rather than lend more aggressively. Without structural reform, it’s difficult to envision material, sustained improvement in lending, which remains well off its 1997 high. Ditto for economic improvement.

Which is why we’d suggest taking all the hullaballoo about Abe’s economic plans with a grain of salt—at best, they temporarily paper over some very deep cracks. On their own, they likely aren’t sufficient to help Abe keep his promise to break Japan out of two decades of deflation and slow growth. Unless he can apply the same energy to economic reform as he is to fiscal stimulus and unnecessary and potentially harmful central bank reform, Japan’s funk likely continues.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 22 - June 262026-06-29

-

Market Analysis Global Vs. Local: UK Bond Yield Edition2026-06-29

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-06-29

2026-06-29 -

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today