Personal Wealth Management / Market Analysis

Should the SEC Say Less Reporting Is More?

Would changing from a quarterly to a semiannual reporting system be better for investors?

It is the start of the school year, and President Trump has already given the SEC homework. Their assignment: Study the rule requiring public companies to report earnings quarterly. Trump suggested a “six month system” is the way to go because it would “allow greater flexibility & save money.”[i] Is he right?[ii] Though the argument might have some philosophical merits, we don’t think investors should overstate the potential change—it isn’t likely to radically alter how businesses operate.

Since 1970, the SEC has enforced federal securities rules mandating quarterly earnings reporting. President Trump was the latest critic, but he was far from first. During her presidential campaign, Hillary Clinton attacked “quarterly capitalism”—“excessively short-term thinking in which Wall Street considerations end up doing too much to drive Main Street business decisions.”[iii] But “quarterly capitalism” wasn’t even Clinton’s term—the Harvard Business Review first publicized it back in 2011. Since then, myriad folks, from academics to a certain beleaguered Tech impresario, have criticized the practice, and support for a semiannual system has been gaining steam. Proponents say fewer reporting requirements equal lower compliance costs as well as more time to plan for the longer term—both theoretical positives.

While we understand some of these hypothetical pluses, quarterly reporting isn’t a bugaboo holding businesses back, either. True, today’s quarterly reporting is largely a circus pointing eyeballs toward an ultimately backward-looking event—not meaningful for forward-looking stocks. However, less frequent reporting could exacerbate that circus and increase the hyperbolic focus on “earnings season.” As Barry Ritholtz recently wrote in Bloomberg:

Twice-a-year earnings reporting will make the event so momentous, with such focus on it, that any company that misses analysts’ forecasts will find their stock price shellacked. The twice-yearly focus on making the per-share number will become overwhelmingly intense.[iv]

While theory, it is a possible unintended consequence worth highlighting.

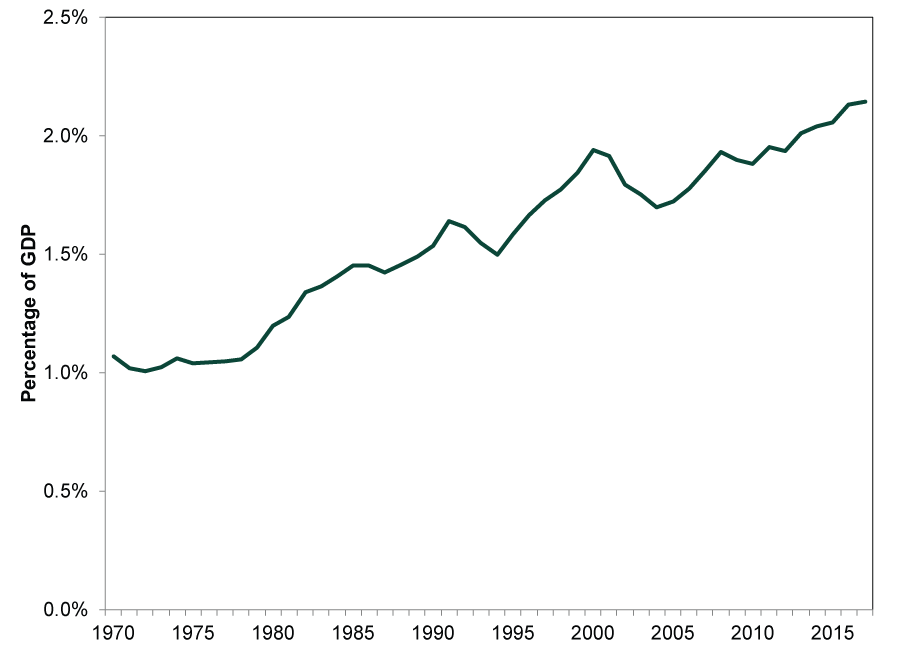

Plus, going from three months to six months isn’t that much more of a “long-term” view. A CEO announcing she has to open a new plant because her business has more orders than it can currently handle shouldn’t be a tough sell with shareholders. We also fail to see how a logistical change would meaningfully increase business investment, which is already high. Since quarterly reporting became mandatory in 1970, R&D has risen from 1.1% of US GDP to 2.1% in 2017.

Exhibit 1: R&D as Percentage of US GDP Since 1970

Source: BEA, as of 8/28/2018. Research & Development as percentage of US GDP, annual, 1970 – 2017.

Different reporting conventions haven’t proven to drive production or alter investor behavior. We aren’t aware of anyone arguing Europe is a bastion for business because the EU stopped requiring quarterly earnings reports in 2014. Private companies don’t have the quarterly reporting requirements of public companies, but that doesn’t make their shareholders less demanding. For example, in 2015 and 2016, some of Silicon Valley’s private tech firms started feeling pressure from investors to start showing profitability. As a Financial Times report noted in June 2016:

The region’s VC-funded innovation machine has always judged rising stars on the strength of their revenue growth rates. Suddenly, however, even the most high-profile unicorns—start-ups valued at more than $1bn—have started to obsess about a different metric: profits.

…

Even companies that can still raise cash are finding a new hardheadedness among investors. “Suddenly, profitability is huge,” says Brent Bellm, chief executive of Bigcommerce, a software company that raised $41m in May. “A couple years ago, they were just applying a multiple of revenues, and now they are looking for a path to profitability.”[v]

This push for changing reporting requirements strikes us as fodder for CEO marketing spin. Company leaders can complain about these “onerous” regulatory burdens crimping business while downplaying losing investments or other bad news. Or, for the glass-half-full camp, CEOs are succeeding despite excessive regulations.

Even if the SEC relaxed its quarterly requirement, public companies wouldn’t necessarily pull the plug. They already have the infrastructure to report quarterly numbers, so adjustments wouldn’t be arduous. Plus, though the rules mandate a certain amount of reporting, publicly traded firms could always provide more! Some big European companies—which aren’t beholden to SEC rules—produce quarterly figures for comparisons to their US peers. Companies could continue producing quarterly numbers in the name of transparency—more marketing spin. Many public firms already go above the requirements because investors want the information. The SEC doesn’t demand companies deliver conference calls, news releases, supplementary reports, GAAP and pro-forma earnings, earnings guidance and more. Companies deliver all this because investors want it—and the former want to keep the latter happy.

In general, we favor more transparency than less, all else equal. However, the potential shift seems to us like rearranging the furniture. Whether regulators recommend a change or no to the quarterly reporting system, we don’t see this meaningfully affecting the amount of information already available to investors.

[i] Source: https://twitter.com/realDonaldTrump/status/1030416679069777921

[ii] And whatever your answer is, we promise not to dress you down a la Professor Terguson.

[iii] Source: “Hillary Clinton wants to take on "quarterly capitalism" — here's what that means,” Matthew Yglesias, Vox, 7/24/2015.

[iv] Source: “Reporting Profits Daily Would End Corporate Short-Termism,” Barry Ritholtz, Bloomberg, 8/20/2018.

[v] Source: “Unicorns: Between myth and reality,” Richard Waters and Leslie Hook, Financial Times, 6/27/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility By the Numbers: 2026’s ‘Volatility’2026-06-12

-

Expert Commentary This Week in Review | IPOs, US Inflation, ECB Rate Hike

2026-06-12

2026-06-12 -

Market Analysis Are World Oil Reserves Dangerously Low?2026-06-11

-

Expert Commentary Think Twice Before Buying an IPO

2026-06-11

2026-06-11

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today