Personal Wealth Management / Economics

Sinking Fortunes in the Land of the Rising Sun

Not even a recession can dent investors' optimism for Japan. That's a problem.

No word on whether Australian PM Tony Abbott was giving Japanese PM Shinzo Abe election tips or just making a funny. Maybe both? Photo by Ian Waldie, Pool/Getty Images.

Pop quiz: What do you get when you hit a struggling country with higher prices and a three percentage point sales tax hike? Give up? Recession! At least, according to Japanese GDP released Monday that's what Japan got, with the second straight GDP contraction placing the archipelago into recession by one common definition. Globally, this doesn't mean a ton-growth elsewhere is more than enough to offset Japan's -1.6% annualized Q3 drop. But the causes and domestic fallout reiterate why we've long thought investors' expectations for Japan are too high and better opportunities lie elsewhere.

In our view, the only thing shocking about Japan's back-to-back contractions is that anyone was surprised-when consumers get whacked with higher taxes and prices while wages stagnate, they spend less. When businesses face higher input costs as an import-reliant nation's currency weakens, they spend and invest less. With the yen weakening and investment and spending largely stalling in Q3, it seemed a given that you could mark your calendar for "Recession Day" on November 17 a couple months ago. Yet, when The Wall Street Journal rounded up analyst forecasts, the median projection was 2.25% growth, and not one forecast a decline. Bloomberg's panel of experts was similarly flummoxed.

We don't mean that as a knock on the pros. It just illustrates where sentiment is on Japan-too high. We had the same view back in August, after most observers and Japan's government greeted the 7.3% Q2 contraction with optimism. A Bloomberg survey conducted last week provided further evidence. 54% of respondents were "optimistic" about Prime Minister Shinzo Abe's economic policies. 68% believed Japan's economy is stable or improving. 42% believe monetary policy is "about right," and 33% believe the same about fiscal policy-both are pluralities. BoJ Governor Haruhiko Kuroda seemed to agree two weeks ago, saying the economy "continued to recover moderately as a trend" (though that didn't stop him from boosting quantitative easing). All the while, most monthly data disappointed, Japan's Leading Economic Index slid and the yen weakened further, jacking up import costs for already-strained households and businesses. The writing was on the wall. Most just didn't see it.

Funnily, the only person apparently unsurprised at the news was Abe. For months, he has called the weak yen a burden for consumers and small businesses, implying an economic threat. Last week, cabinet insiders leaked word he would likely delay tax hike part deux (slated for October 2015), which the law stipulates can be shelved only if economic conditions deteriorate. We'll likely get his final decision this week-perhaps as early as Tuesday, when his panel of experts meets. Should they delay the hike, word is Abe will dissolve Parliament and call a snap election in order to get a mandate supporting their move-vote for us so we can prevent another recession in a year!

This seems like pure political gamesmanship. A distraction. Call us cynics, but if ever there were a time that an election could cement Abe's power, that time is now. Sans election, the Liberal Democratic Party (LDP) would be in power just two more years. Abe's term as leader expires in September 2015, and his political capital is waning. If he wins an election now, the LDP gets to stay another four years, and his leadership campaign probably gets more support. Seems to us this is all about staying in power-always and everywhere a politician's top goal, in our experience.

Of course, that isn't the official marketing. The powers that be call it a referendum on Abenomics. But that opens another problem: Abenomics is unfinished. It is supposed to be a three-part plan: Monetary stimulus, fiscal stimulus and sweeping economic reform. Monetary and fiscal stimulus are in the books, and one cabinet minister is already pressing for more fiscal stimulus (this time with cash handouts and personal tax cuts, not infrastructure spending).[i] But reform remains in a holding pattern-all talk, (almost no) action. Abe has made three big reform pronouncements (June 2013, September 2013, June 2014), but all lacked actual reforms. They were broad lists with vague goals of boosting growth, improving corporate governance, cutting corporate taxes and broadening the labor force, without legislation or even a road map to get there. So we ask: How can you make an election a referendum on something that hasn't been done yet? We are fairly sure you can't, because there is nothing to judge and no results to weigh, which means the conversation likely centers on fiscal and monetary measures. This makes sense considering voters tend to like stimulus. Voters tend not to like politically contentious issues like free trade, labor market reform, deregulation and restarting nuclear power plants.

If our hunch is right and the campaign ignores reform, momentum likely shifts for the worse. Even with strong support early in his term, Abe either couldn't or wouldn't pursue tough change. He talked a lot! He promised to "drill" through all the entrenched interests in his way! But nearly two years in, his drill is on the shelf. We fail to see how a snap election centered on the sales tax, short-term economic results and fiscal and monetary measures would change matters for the better. It would only reinforce support for stimulus, which is already clearly not a net benefit or economic fix.

Even if a successful election does reinforce Abe's political capital, it is an open question how he'll spend it. The long-festering issue of national security legislation and revising Article 9 of Japan's constitution-the anti-war clause-appears poised for a comeback. Nationalist party members are salivating at the prospect of having more clout to push through that controversial change. Abe is mum on the subject, but it's well-known that rewriting that clause is his lifelong ambition-and a family dream going back to his grandfather, former Prime Minister Nobusuke Kishi, who served under Tojo during World War II. Abe has pressed this issue repeatedly since he took office, actually doing more on that front than on the reform front. Actions speak louder than words.

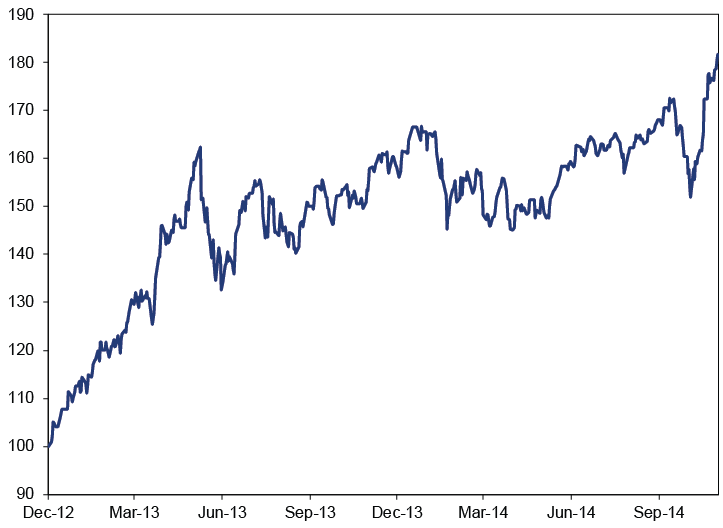

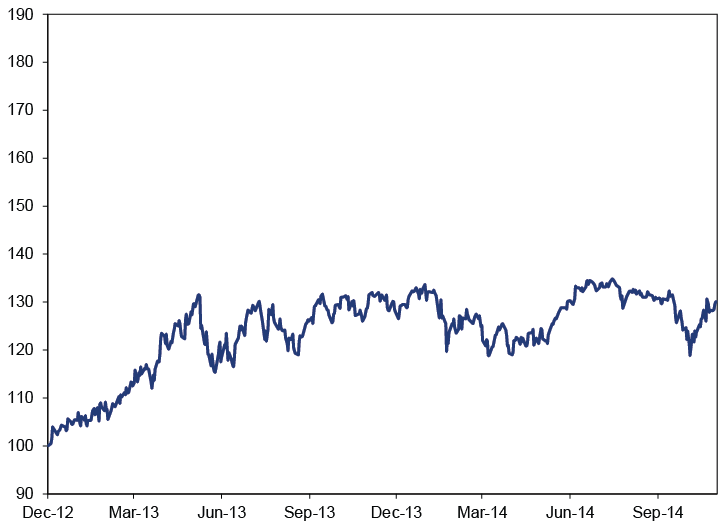

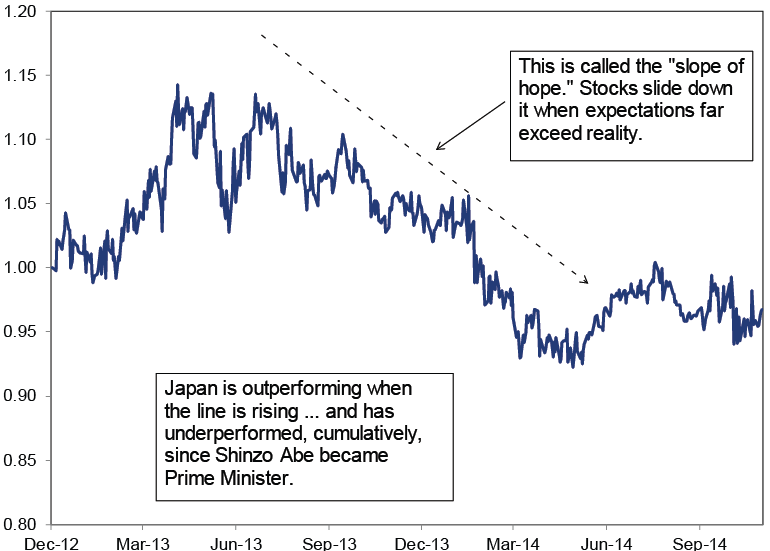

In short, our outlook on Japan is about the same as it has been since Abe took over in December 2012. Expectations are too high, and reality likely disappoints. Pundits keep lauding Japanese stocks' amazing rally, citing the eye-popping gain since Abe was elected, in Exhibit 1. They don't bother mentioning you only got that gain if you invested in yen-in dollars, the gain is far smaller (Exhibit 2) and lags world stocks (Exhibit 3). That tells you all you need to know about the present disconnect. The more time elapses without reform while sentiment stays high, the more Japan appears set up for continued disappointment.

Exhibit 1: MSCI Japan Index (in Yen)

Source: FactSet, as of 11/17/2014. MSCI Japan Index returns with net dividends, in JPY, 12/14/2012 - 11/17/2014.

Exhibit 2: MSCI Japan Index (in Dollars)

Source: FactSet, as of 11/17/2014. MSCI Japan Index returns with net dividends, in USD, 12/14/2012 - 11/17/2014.

Exhibit 3: MSCI Japan/MSCI World

Source: FactSet, as of 11/17/2014. MSCI World Index and MSCI Japan Index returns with net dividends, in USD, 12/14/2012 - 11/14/2014.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i]The definition of insanity, they say, is doing the same futile thing again and again. Not that we are calling politicians insane. That would be an insult, and not just to politicians.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | April CPI, Prediction Markets, Financial Fraud2026-05-11

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 4 - May 82026-05-11

-

Politics UK Stocks and the Starmer Scuttlebutt2026-05-08

-

Expert Commentary This Week in Review | Tariff Update, National Debt Concerns, April Jobs Data

2026-05-08

2026-05-08

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today