Personal Wealth Management / Market Analysis

Sizing Up Sterling's Swoon

12 months past the Brexit vote, let's put the weak pound in perspective.

Happy Brexitiversary, everyone! Yes, a year ago Friday, the UK voted to leave the EU, unleashing a tidal wave of media hyperventilation. Among the most frequent sources of angst in the 12 months since is the pound, whose drop fueled fears aplenty. Yet putting the pound's gyration in some context may be valuable-and, in the process, shed light on a few media theories about what's ahead.

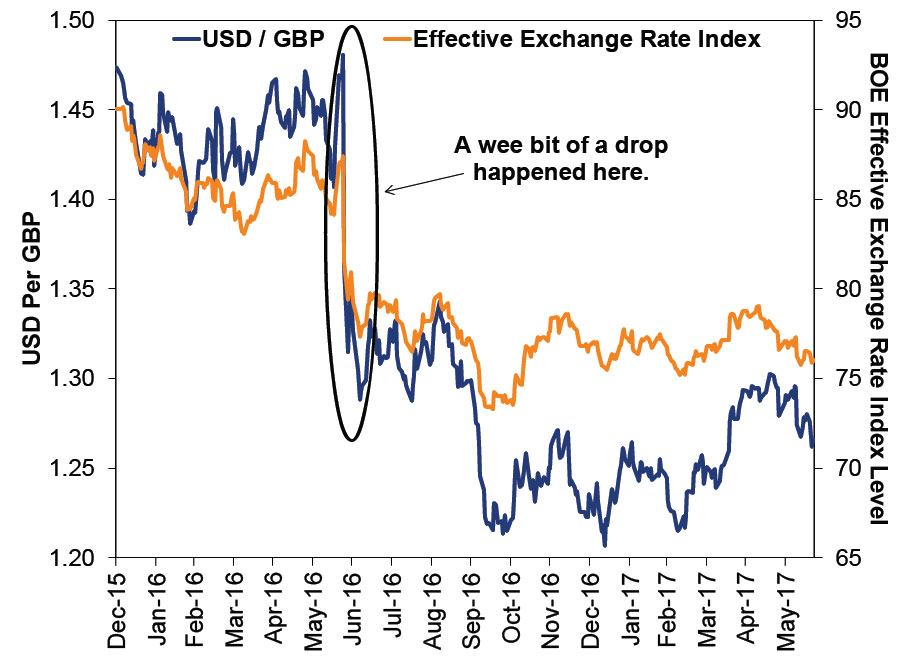

As Exhibit 1 shows, the pound's post-Brexit decline occurred mostly between June 23 and July 6, 2016. During this eight-trading day stretch, the BoE's Broad Effective Exchange Rate Index-a measure of the pound's value against 21 trading partners' currencies-dropped -11.6%.[i] The pound also fell -13.0% against the US dollar.[ii]

Exhibit 1: Not So Sterling

Source: FactSet, as of 6/23/2017. USD per GBP spot rate and BoE Nominal Effective Exchange Rate Index (Broad), 12/31/2015 - 6/22/2017.

As the chart shows, since July 6, the pound is down merely -1.7% against the dollar-small!-and was actually up as recently as June 8. Similarly, the sterling index is off -1.8% from July 6, 2016 to the present, vacillating between periods of strength and weakness.[iii]

To us, the directionless drift since last summer's brief bout suggests three things for investors.

1. It shows weak pound-driven inflation fears are likely overwrought. While it could take time to work through supply chains and impact downstream product indexes, the pound's weakness should fall out of year-over-year data in the coming months. We're already seeing anecdotal signs of this in PMI surveys.

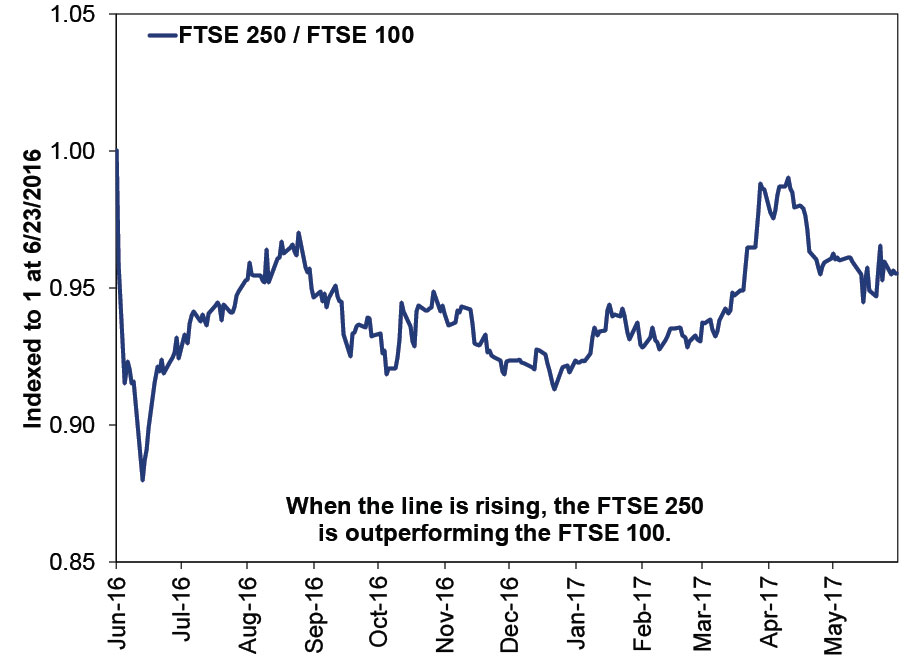

2. Claims that UK stocks are up due primarily to multinationals benefiting from the weak currency are off target. If this were true, one would presume the FTSE 250-a gauge of mostly domestically oriented British firms-would persistently lag the FTSE 100. Yet, as Exhibit 2 shows, after the initial shock wore off, those domestic firms more or less held their own.

Exhibit 2: Pound Weakness Isn't the Full Story

Source: FactSet, as of 6/23/2017. FTSE 250 divided by FTSE 100 with gross dividends, indexed to 1 at 6/23/2016. 6/23/2016 - 6/22/2017.

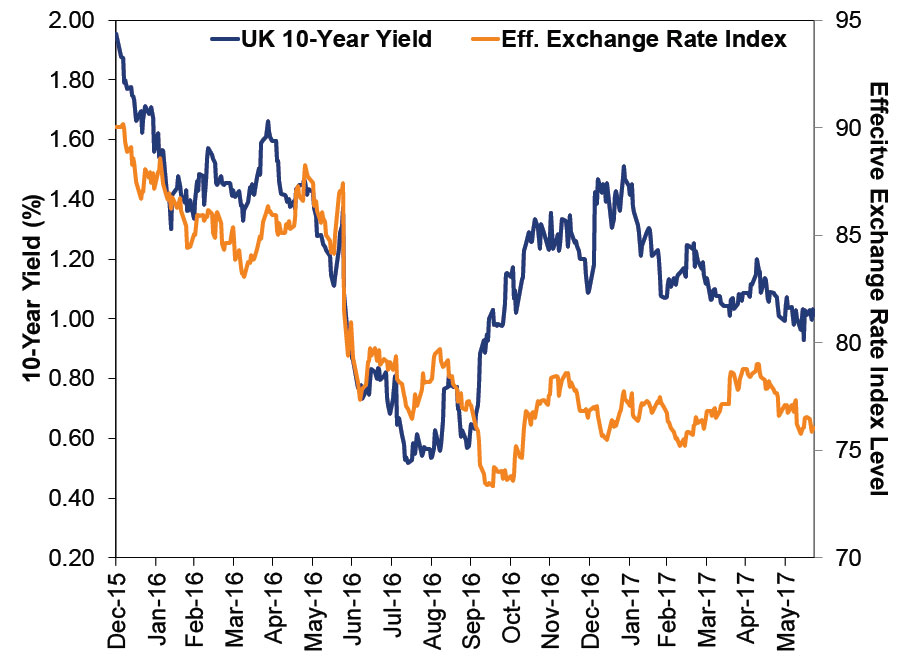

3. Many Brexit doomsayers argue the pound has further to fall, as uncertainty over Brexit terms persists. Now, we are not in the currency-forecasting business and have no outlook to share, but we can look back and assess whether the decline is necessarily so Brexit-centric. As Exhibit 3 shows, the steep drop in rates coincides with the steep drop in sterling. This makes sense-global currency markets are about as liquid and fungible as can be. If rates fall fast in Britain-or are expected to remain low for long-then currency investors will likely teleport their holdings elsewhere-America, Canada, Australia, you name it. There was likely more at work than merely Brexit last year-so looking exclusively at talks now seems fallacious.

Exhibit 3: Yields Pound Sterling

Source: FactSet, as of 6/23/2017. UK 10-year gilt yields and BoE Broad Nominal Effective Exchange Rate Index, 12/31/2015 - 6/22/2017.

[i] Source: FactSet, as of 6/23/2017. BoE Broad Nominal Effective Exchange Rate Index, 6/23/2016 - 7/6/2016.

[ii] Ibid. USD / GBP spot rate, 6/23/2016 - 7/6/2016.

[iii] Source: FactSet, as of 6/23/2017. USD per GBP spot rate and BoE Nominal Effective Exchange Rate Index (Broad), 7/6/2016 - 6/22/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today