Personal Wealth Management / Economics

Skepticism About a Simmering Economy

Many doubt the strength of the US economy—are those concerns justified?

The revised estimate of Q2 US GDP hit Thursday, and under the hood, data show the private sector is humming along. Headline reactions tell an even more powerful story. US GDP has been setting consecutive record high levels since Q2 2011, but lately, headlines have largely interpreted growth as a negative. If it’s slow, it’s too weak. If it’s faster, it means QE will end soon (a GOOD thing, in our view, but most disagree). But Thursday, overall reactions were neutral at worst and positive at best, suggesting the QE hyperfocused investor sentiment may be easing up—a positive force for stocks in our view.

Perhaps investors are finally starting to realize just how healthy the US is. Q2 growth was revised up quite a bit, from a 1.7% seasonally adjusted annual rate (SAAR) to 2.5% SAAR. Once again, the private sector led the charge. Private investment was particularly hot, rising 9.9%, with business spending alone up 4.4%. Exports were also revised up, and while import growth was downwardly revised, it was still solidly positive—demand at home and abroad is alive and well. Add in housing’s ongoing recovery and still-growing consumer spending, and it’s clear the US private sector is in pretty darned good shape.

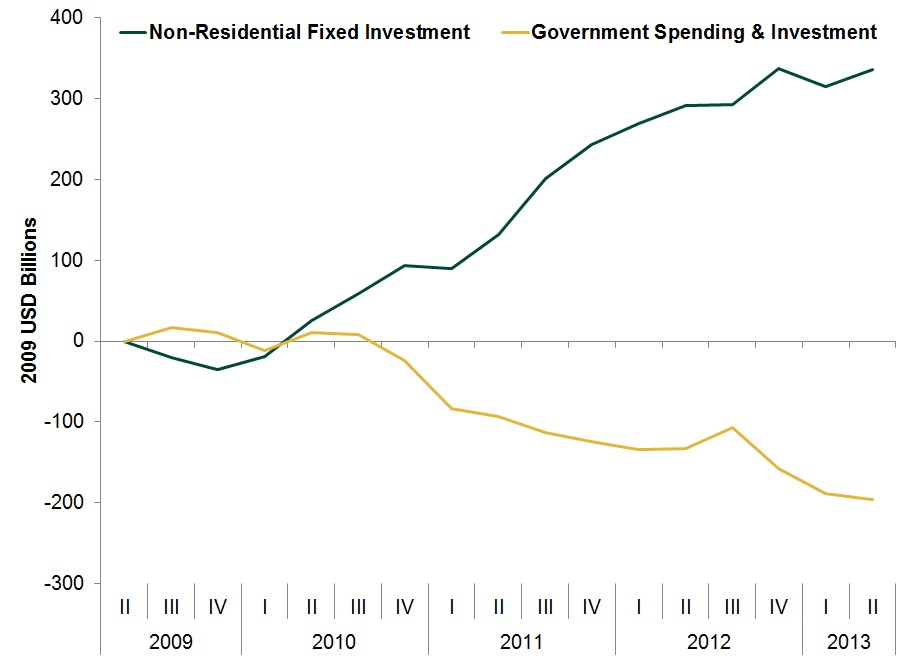

Public sector cuts, however, continued weighing on headline growth, as government spending and investment fell -0.9%. Shrinking government outlays likely remain a headwind for some time, given the sequester seems here to stay. Yet, so far, rising private investment has more than offset the public sector’s negative impact (Exhibit 1).

Exhibit 1: Change in Business and Government Spending Since the Recession Ended

Source: Bureau of Economic Analysis, as of 8/29/2013.

It seems less government involvement in the economy has been filled by private sector growth, plus some. That’s a net benefit to the economy, as the much larger and generally more efficient private sector is a more sustainable economic growth engine. And that private sector is cash rich, providing fodder for future earnings growth.

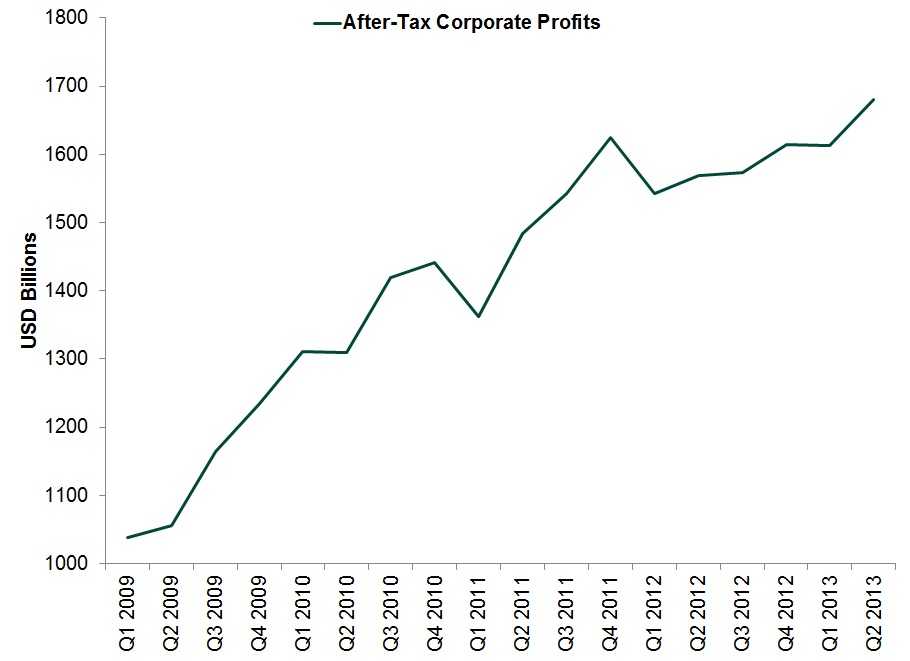

That cash is coming from growing corporate profitability. The Bureau of Economic Analysis also released Q2 corporate profits Thursday, and they were huge—up $78 billion (+3.9% q/q), more than erasing Q1’s $26.6 billion decline. This is largely in line with profits’ steep-yet-uneven growth during this bull market—making Q1’s dip seem more like a blip. (Exhibit 2)

Exhibit 2: After-Tax Corporate Profits

Source: St. Louis Federal Reserve, as of 8/29/2013. After-Tax Corporate Profits with Inventory Valuation and Capital Consumption Adjustments, Q1 2009 – Q2 2013.

With investment high and rising, sales growing and cost pressures overall tame, profits look set to continue growing—bullish for stocks, which track businesses’ future earnings. As sentiment improves and investors gain more confidence in future earnings growth, they bid more and more for a share of it. Hence why the largely optimistic reactions to Q2’s GDP revisions are so noteworthy—they suggest sentiment is perhaps starting to get a bit more optimistic. The more sentiment improves, the more investors are willing to pay for stocks, and the more stocks rise.

This could go on for some time—sentiment remains far from uniformly optimistic. Pockets of skepticism remain. One recent example is the popular reaction to ongoing UK economic improvement. Last week, UK GDP growth was revised up to nearly 3% annualized rate (0.7% q/q). All three sectors (manufacturing, construction and services) grew and business investment notched its first consecutive quarters of growth since 2007. But reactions to the revision were muted—to most, growth is either too slow to matter or the “wrong kind” of growth since consumer spending is leading the charge, not exporters. Broad acceleration is underappreciated—skepticism persists.

Which means sentiment has plenty of room for improvement—and a ways to go before it reaches bull markets’ typical euphoric heights. Just one more indication this bull has room to run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—December 8 - December 122025-12-15

-

Expert Commentary 3 Things You Need to Know This Week | Central Banks, US Jobs, Japan Gov. Bond Yields

2025-12-15

2025-12-15 -

Expert Commentary This Week in Review | Fed Rate Cut, China Trade Balance, Reshoring Manufacturing

2025-12-13

2025-12-13 -

In The News A Lesson on Financial Risk, Leveraged Lending Edition2025-12-11

Learn More

Learn why 190,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 9/30/2025

New to Fisher? Call Us.

Contact Us Today