Personal Wealth Management / Market Analysis

Slow Down on Slow Growth Fears

Recent fretting over slow US economic growth is-and has been-overwrought, in our view.

Slow US economic growth concerns are rampant today, as they have been for this entire expansion. Headlines bemoan the "slowest US recovery since WWII," and to make matters worse, some surmise growth is "wilting." Myriad folks, from the Democratic and Republican presidential candidates to big supranational outfits, aren't very keen on the world's biggest economy right now. However, the data don't support this dour narrative. While growth is by no means gangbusters, the US economy is doing better than most appreciate-an underappreciated bullish positive.

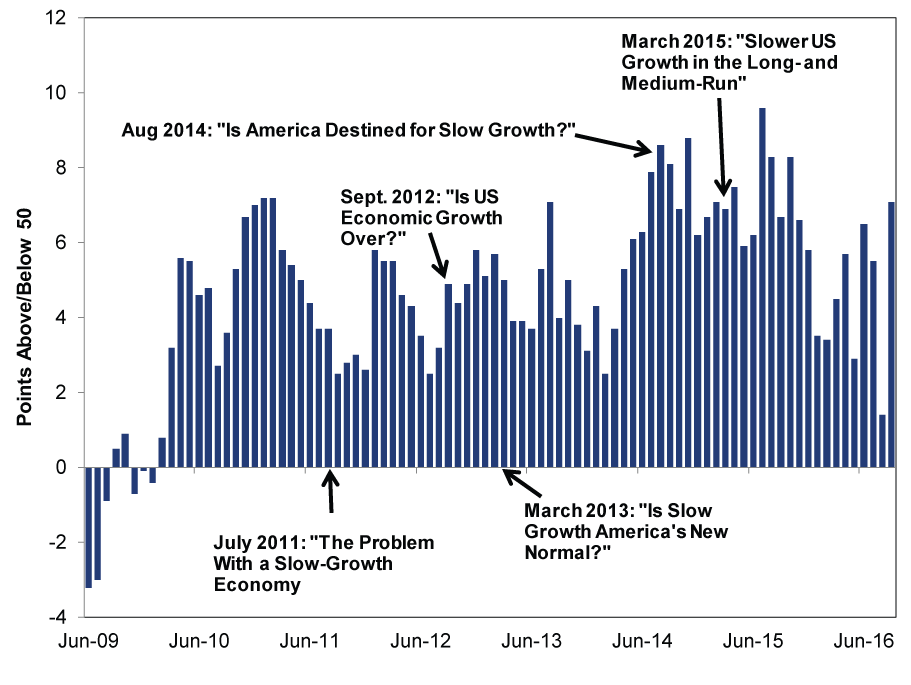

First, the most recent data: The Institute for Supply Management's (ISM) Non-Manufacturing Purchasing Managers' Index (PMI) rose to 57.1 in September, up from August's 51.4. This was the highest reading since October 2015, and out of 18 surveyed industries, 14 reported growth. Another positive: The forward-looking New Orders subindex also jumped, from August's 51.4 to 60.0. Today's orders are tomorrow's production, suggesting a majority of businesses probably keep producing more.

Now, a little background on PMIs: These monthly surveys track business activity, with respondents reporting whether business was better, worse or about the same. PMIs above 50 indicate more respondents grew than not; below 50, more contracted. While PMIs provide a quick and timely snapshot of recent economic activity, they aren't perfect. They give a sense of breadth of growth, not magnitude-we don't know how much firms grew, just that a majority think they did. Data can also be volatile month-to-month. A strong September report doesn't necessarily mean growth will zoom, just like one sub-50 reading doesn't automatically bode ill. These limitations aside, the non-manufacturing[i] PMI is broad and useful. It includes a wide swath of services industries, ranging from Finance & Insurance and Real Estate to Retail Trade and Health Care & Social Assistance-notable, given services industries comprise about 70%[ii] of US GDP.

The ISM non-manufacturing PMI has steadily signaled growth throughout the current expansion, amid constant chatter about worrisome "slow growth" prospects.

Exhibit 1: Non-Manufacturing PMI's Ascent in a "Slow Growth" Economy

Source: FactSet, as of 10/5/2016. Articles are here, here, here, here and here.

Or, if you prefer words: September's report marks the 80th straight month of growth for the non-manufacturing sector.

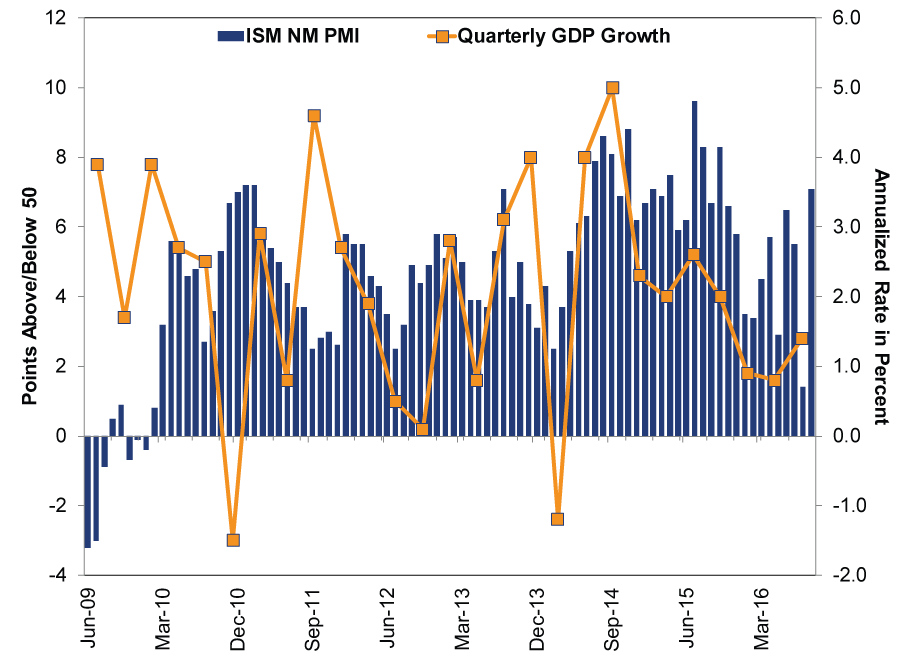

As the US' non-manufacturing businesses have largely grown, so has GDP. Here is the same PMI chart with quarterly GDP readings highlighted.

Exhibit 2: Don't Doubt the Growth

Source: FactSet and the Bureau of Economic Analysis, as of 10/5/2016.

Of course, we would be remiss if we myopically zeroed in on just one indicator. But other data also show the US economy is on solid footing. Markit's September US Services PMI hit 52.3, beating its flash estimate and August's 51.0. ISM's manufacturing PMI rose to 51.5 from August's 49.4. Though manufacturing has flipped in and out of contraction over 12 months, sparking recessionary fears, heavy industry isn't indicative of the broader economy. Moreover, it has also largely rebounded from its late 2015-early 2016 contractionary stretch. Beyond that, businesses continue importing and exporting, a sign of healthy demand both here and abroad. In August, exports rose 0.8% m/m while imports climbed 1.2%. While higher imports mean a larger trade deficit, this isn't a negative. (See the logistics and retail industries with any questions about that.) Rather, rising imports and exports mean higher total trade overall: a positive.

While we won't get the advance estimate of Q3 GDP until the end of the month, some have fretted recent downward revisions to a couple GDP forecasts (e.g., Atlanta Fed's GDPNow, NY Fed's Nowcasting Report). However, not only do both still signal growth-albeit a bit slower than projections from a month ago-data released in October could very well boost those forecasts, too. Even if the most recent readings prove prescient, growth of 2.2% (per the Atlanta Fed) is still fine, and up from Q2. Plus, while most economic reports are inherently backward-looking, nothing is out of the ordinary here: Growth continues.

By no means are we saying US growth is robust and everyone is missing it, as the current expansion's average annual growth is indeed the slowest in the postwar era. While some pundits try and explain it all with grand theories (e.g., secular stagnation), reality is more nuanced. Quantitative easing (QE), for instance, was more of a headwind than economic stimulant, and therefore a self-inflicted wound. But also, GDP-the most commonly cited statistic for economic growth-is an imperfect measurement. It originated back in the 1930s, when the US economy looked much different than it does now. Then, industry and manufacturing were much more prominent; today, services comprise the lion's share of economic activity. Plus, GDP doesn't yet possess the language to capture the developments of the Information Age-the productivity gains unleashed by the Internet aren't as easily quantified as factory orders. And, hey, certain components less connected to the actual economy are exacerbating the weakness. These details aside, investors shouldn't miss this more important point: Stocks don't require robust economic growth to rise higher. Rather, they move on the gap between expectations and reality. The steady stream of dour, skeptical news has weighed on investor sentiment, and it doesn't take much to beat expectations. People worry about a weak recovery, not realizing that we've been in expansion since 2011, when GDP surpassed its pre-recession high. When folks whisper about recession and the economy keeps chugging along instead, that positive surprise is bullish. Against this backdrop, we expect this unloved bull market to continue grinding higher.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today