Personal Wealth Management / Market Analysis

Some Friendly Facts on Wednesday’s Wild Ride

Beware the sensationalist coverage of foreign indexes-it should come with some asterisks for global investors using their home currencies.

Ouch. That's about the only word we can use to sum up Wednesday's volatility, which saw many indexes globally hit new lows. Some-namely the UK's FTSE 100 and Japan's Nikkei 225-breached -20% from their prior highs when measured in local currencies, prompting shouts of "bear market!" in their home countries. Fear and gloom are everywhere. But don't give in. During corrections, it is fairly normal for some narrow benchmarks to enter "bear territory." It doesn't mean world stocks are actually in a bear market-and even after Wednesday, they aren't[i]. It just illustrates the importance of global diversification.

When the financial news sites discuss international returns, they usually cite legacy benchmarks in local currency. For UK markets, we get the FTSE 100 in sterling. For Germany, we get the DAX in euro. The Nikkei is always quoted in yen. If you're investing in those countries using any other currency, those returns aren't relevant to you, as currency translation would impact your results. For example, the Nikkei 225 is down -21.7% since 6/24/2015 in yen.[ii] In dollars, it is down less, -16.4%.[iii] Some articles will compare a bunch of benchmarks, each in their local currency. Yet any proper comparison must also account for currency moves. All are big reasons why we think much of Wednesday's sensationalism missed the target. It shunned measured analysis for eye-popping numbers.

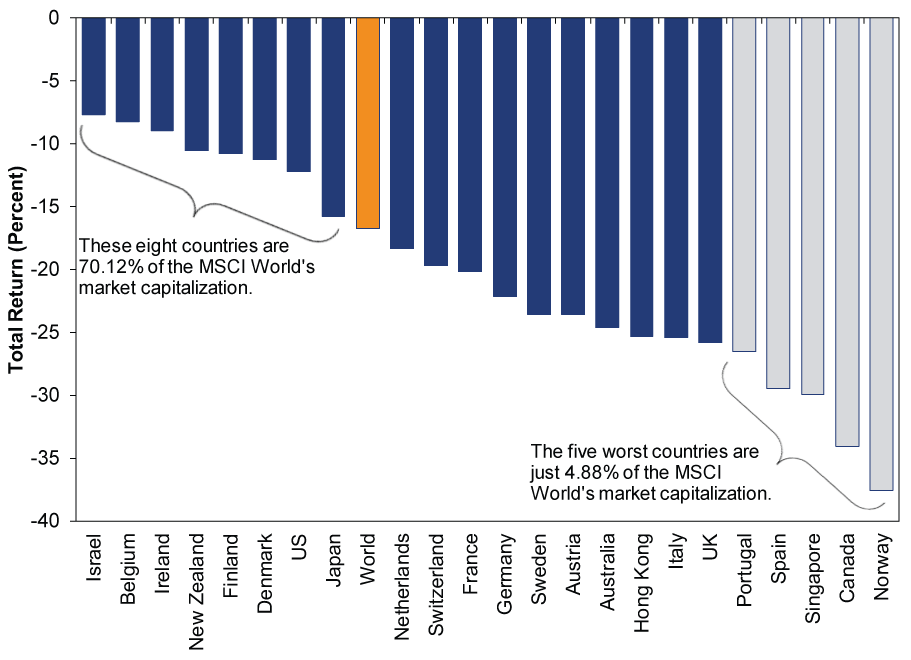

In doing so, it also overemphasized some very small pieces of the global stock market. Indexes like the FTSE 100, Germany's DAX and the Nikkei 225 are, to varying degrees[iv], loosely fair representations of their countries' broad stock markets. But compared to global markets, they are very, very narrow. They represent blue chip stocks in countries that are 7.3%, 3.4% and 9.0% of the MSCI World Index by market cap, respectively.[v] A general rule of thumb is that the narrower the index, the wilder the ride. During corrections and "normal" bull market stretches, individual countries regularly diverge from broader global returns. Particularly those whose markets have only a few companies or sectors, like Norway, Ireland and Denmark. During this correction, some countries have held up far better than the world. Others, especially those with heavy Energy and Materials exposure, have done far worse.

Exhibit 1: Total Returns Since World Stocks' Most Recent High

Source: FactSet, as of 1/20/2016. MSCI index returns from 5/21/2015 - 1/20/2015 in USD. MSCI USA returns include gross dividends; all others include net dividends.

This is why global diversification is vital. A more market-like portfolio generates more market-like returns, usually with less expected volatility than a geographically narrow portfolio. Those jarring country-specific moves tend to cancel each other out. During this correction, Ireland's 0.16% share of the MSCI World has helped offset Norway's 0.21% share. All of these extremes meld together into the MSCI World's return, which is well within correction norms.

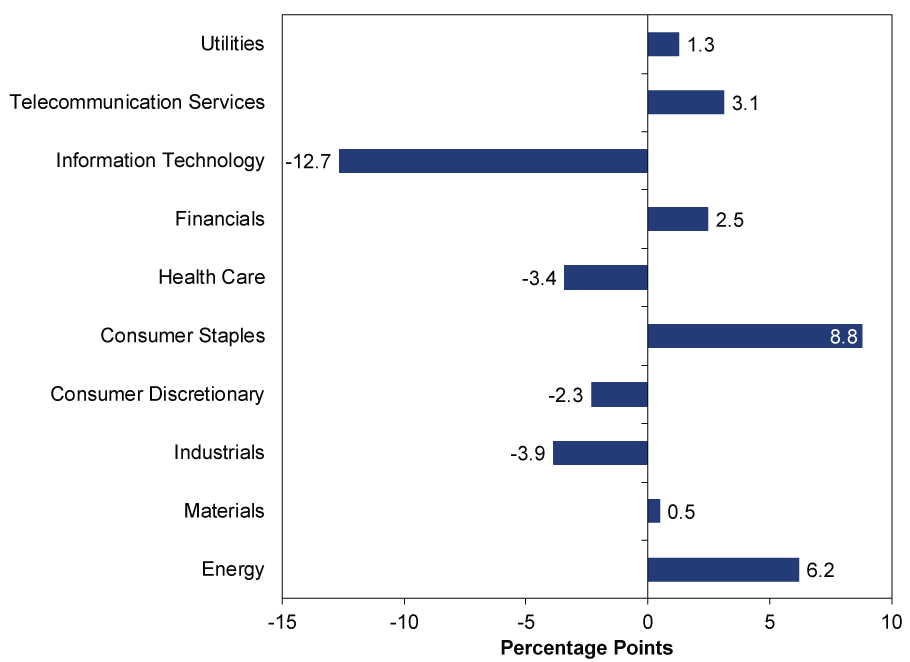

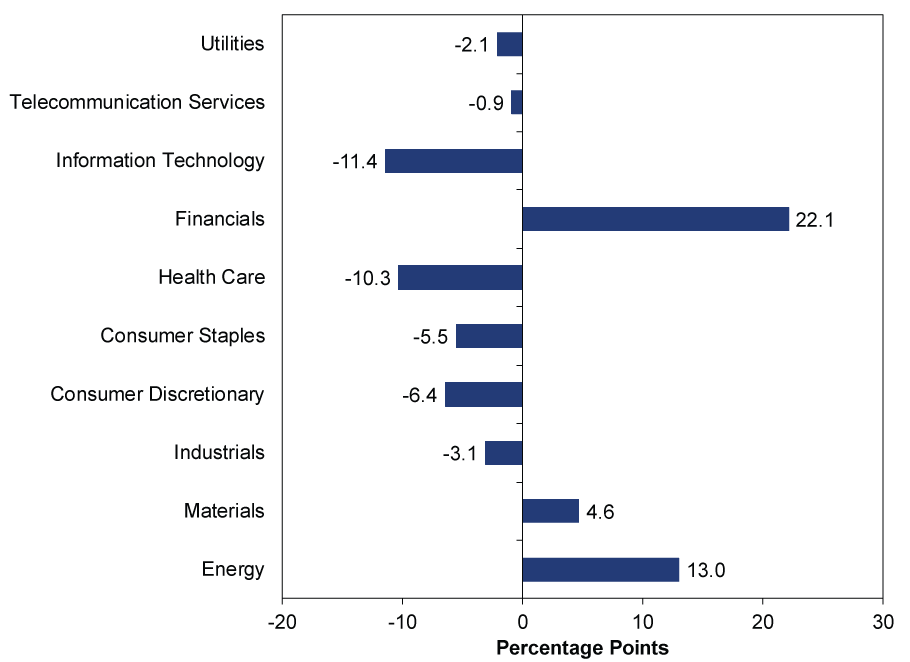

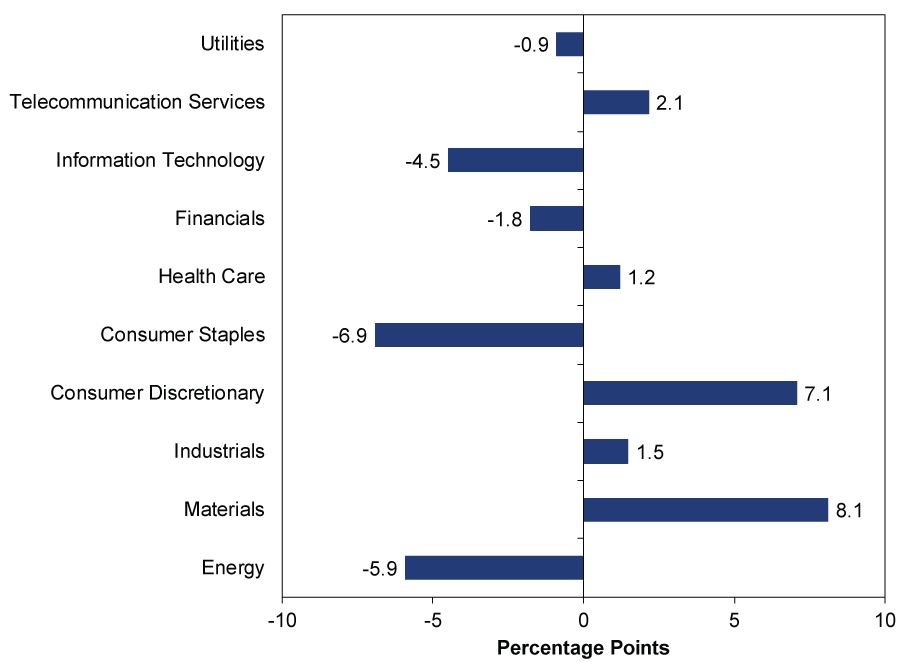

Now, if you're American, then the notion of investing only in one small European country might sound, well, foreign-that's because your home-country bias points to the U-S-of-A. But for investors elsewhere, it's different. Humans naturally gravitate toward the familiar, and domestic stocks are familiar. Many UK investors have an affinity for UK stocks. Many Canadians give top preference to Canadian stocks. Any investor in any country on earth is subject to this tendency, and proper diversification isn't always intuitive. Even when folks do invest globally, they might put 20%, 30%, 40% or more in their home country. In any country except the US (58.9% of the MSCI World Index), this is a huge overweight, adding risk. Not just on a country level. Small countries' sector weightings are usually quite disconnected from the world. Heavily overweighting your home country could make your sector weightings severely out of whack. The MSCI Norway, for example, is more than 40% in commodities (Energy and Materials), which have been hammered by falling oil and metals prices. Even the UK, Canada and Germany, which have much bigger markets, have some big sector divergence. British markets are severely underweight Technology and overweight Energy, Materials and Staples. Canadian markets are hugely overweight Financials, Energy and Materials. German markets have outsized Materials exposure.

Exhibit 2: MSCI UK Sector Weightings Relative to the MSCI World

FactSet, as of 1/20/2016. MSCI UK sector allocation minus MSCI World sector allocation on 1/19/2015.

Exhibit 3: MSCI Canada Sector Weightings Relative to the MSCI World

FactSet, as of 1/20/2016. MSCI Canada sector allocation minus MSCI World sector allocation on 1/19/2015.

Exhibit 4: MSCI Germany Sector Weightings Relative to the MSCI World

FactSet, as of 1/20/2016. MSCI Germany sector allocation minus MSCI World sector allocation on 1/19/2015.

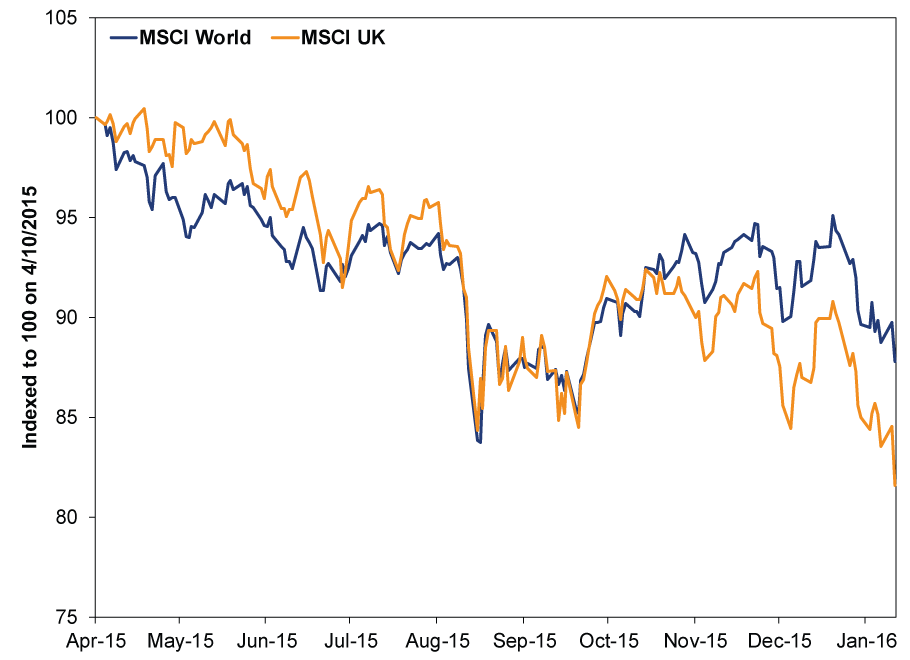

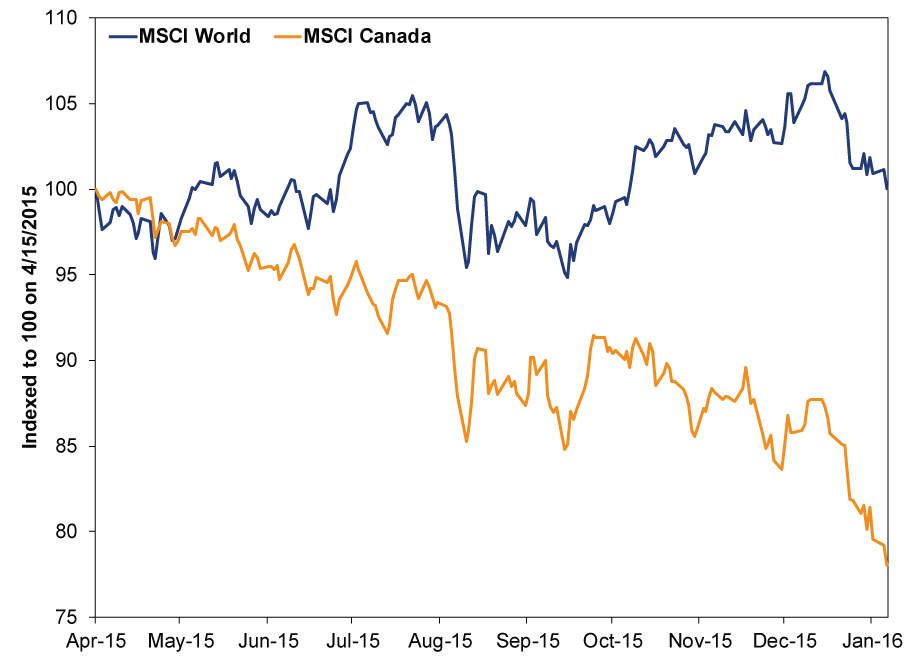

Returns during this correction underscore the importance of diversification. If you're British and investing globally in sterling, your returns are probably much better than that widely cited FTSE 100 bear market (Exhibit 5). That's triply true if you're a Canadian investing globally with Canadian dollars (Exhibit 6). Home country bias might feel great when it works in your favor, but when it doesn't ...

Exhibit 5: The Correction From a British Viewpoint

Source: FactSet, as of 1/20/2016. MSCI World and MSCI UK Index returns in GBP, 4/10/2015 - 1/20/2016. MSCI World returns include net dividends; MSCI UK returns include gross dividends.

Exhibit 6: The Correction From a Canadian Viewpoint

Source: FactSet, as of 1/20/2016. MSCI World and MSCI Canada Index returns in CAD, 4/15/2015 - 1/20/2016. MSCI World returns include net dividends; MSCI Canada returns include gross dividends.

We suspect much of this commentary is cold comfort in the throes of a correction. But perspective is one of your greatest tools at times like this, when fearful headlines drive the temptation to make hasty decisions. Facts can seem cold, but facts are also friendly, and the fact that much of Wednesday's market coverage doesn't totally mesh with reality is a friendly, hopefully comforting, fact. This still has all the hallmarks of a sentiment-driven correction, and corrections often end as suddenly as they begin, sometimes for no apparent reason. The ride down is painful, but if you can separate fact from fearful headline and stay disciplined, you should be well-positioned to catch the ride back up.

[i] Eagle-eyed readers might point out that the MSCI All-Country World Index has breached -20%, but this index includes Emerging Markets, which have long been mired in a bear market. Our analysis here focuses on the MSCI World Index, which spans 23 developed-world countries and 76.6% of the global investible equity market. (FactSet, as of 1/20/2016, MSCI World market cap as a percentage of MSCI All-Country World Investible Market Index market cap.)

[ii] FactSet, as of 1/20/2016. Nikkei 225 price return in JPY, 6/24/2015 - 1/20/2016.

[iii] Ibid. In USD.

[iv] The DAX is probably the furthest off, as it has only 30 firms and excludes Technology. The FTSE 100 and Nikkei 225 are broader and more representative, though they still include a fraction of their countries' investable markets. The MSCI Indexes are broader, but like the Dow Jones Industrial Average in America, these legacy indexes are headline favorites.

[v] FactSet, as of 1/20/2016. MSCI World Index country weightings for the UK, Germany and Japan on 1/19/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today