Personal Wealth Management / Market Analysis

Stocks’ Correction Churn Isn’t a Call to Action

Renewed volatility this week shouldn’t change things for long-term investors.

Thanksgiving is just three days away, and as Americans brine their turkeys (or denounce brining as like soooo 2015), there is one thing they can’t yet add to their list of things to be thankful for: a fast rebound from last month’s stock market drop. Instead, stocks spent most of November drifting sideways before having a rather rough day Monday. Now the S&P 500 sits about 2% above October’s low point, and the MSCI World Index is 1.8% above its October 29 mark, the year-to-date low.[i] Rough patches like this are always frustrating. But they also serve as an important reminder: Corrections’ ends are as impossible to predict as their beginnings. In our view, keeping a long-term view remains paramount for long-term growth investors at this juncture. Instead of twisting yourself in knots over when this rocky spell will end, remember double-bottom corrections aren’t unusual, and that absent new, fundamental, huge negative developments, the bull market should ultimately reassert itself. Being ready for that, in our view, is more important than pinpointing the date it happens.

It would be great if every correction (sharp, sentiment-driven pullback of -10% or worse) were a fast, perfectly shaped V. Being able to trust that any rebound off a low would sustain itself and lead to quick new heights would make investing far more comfortable. But in the real world, markets are bouncy and unpredictable. They zig and zag. Sometimes they zig-zig-zag-zig-zag-zig-zig-zig-zag. There is no pattern, rhyme or reason to short-term volatility.

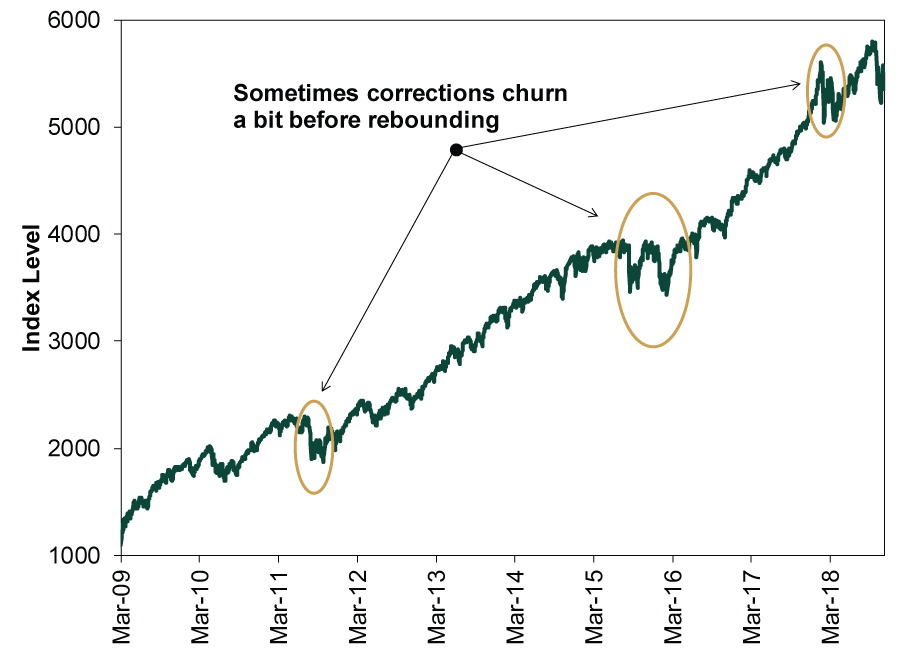

There is, however, history—history showing corrections frequently test their low two or more times before rebounding. The S&P 500’s wintertime correction featured two bottoms—one in early February and one in March. Earlier in this bull market, the 2015 – 2016 correction was more of a W than a V, and 2011’s twin corrections also resembled a large W. Both were painful at the time but now look like mere speedbumps on the way to further gains.

Exhibit 1: S&P 500 Vs and Ws During This Bull Market

Source: FactSet, as of 11/19/2018. S&P 500 total return index, 3/9/2009 – 11/19/2018.

With every correction comes the possibility it could actually be a bear market—a deeper, longer grind worse than -20%. But magnitude isn’t the only difference between a correction and a bear. Corrections start for any or no reason—they are products of investor sentiment. Bear markets, however, have identifiable fundamental causes. One of the reasons they typically start more slowly than corrections is that investors are generally in better moods and don’t see the fundamental negative. So as stocks start rolling over, folks see it more as a buying opportunity than a reason to panic—the mentality they would ideally muster in a correction but don’t, because controlling emotions around money is hard.

Therefore, whenever stocks get rocky, the right move is to survey the landscape and see what markets are grappling with. Are headlines full of well-worn ghost stories and the same alleged negatives they have pondered for months or even years? Or are they rosier and potentially missing something big and ugly? Today, nearly everything we see is the former. Many of Monday’s headlines dwelled on the lack of a formal statement emerging from the weekend’s Asian economic summit—and reports the US/China trade tiff was the reason why. But nothing in this saga is fundamentally new. The US and China have been mired in fitful trade negotiations for the better part of a year. Headlines have warned of a trade war wrecking the economy and stocks since the 2016 presidential campaign. The Trump administration threatened to tax virtually all Chinese imports months ago. A little behind-the-scenes squabble over whether to include a sentence about fighting protectionism in a summit statement isn’t a radical fundamental shift—it’s normal geopolitical squabbling and inside baseball.

Elsewhere, headlines dealt with Brexit—this time in the form of some blowback to last week’s deal from other EU member-states. Consider that the European version of typical squabbling, rather than a meaningful shift. Especially since EU leaders have spent more than two years now grousing about negotiations and sticking points like Gibraltar. So Monday’s objections from Spain, France, the Netherlands and Belgium over Gibraltar, the length of the post-withdrawal transition period and EU shippers’ access to UK waters, respectively, are just more of the same.

So are the litany of economy-related worries, from Fed rate hikes and falling oil prices to weak home sales and shaky GDP in Germany. We are hard-pressed to think of any time during the eurozone’s five and a half year-long expansion when headlines didn’t think it was sputtering out. Germany has blipped weaker before, and we rather doubt a small Q3 contraction spurred largely by auto production hiccups as manufacturers adapted to new emissions tests is a deeply negative forward-looking indicator. Not when loan growth, yield curves and other leading indicators still point positively. As for Fed rate hikes, investors have been dealing with this since 2015—and the economy has grown fine throughout this tightening cycle. Falling oil prices? 2014 – 2016 already proved that while cheap oil creates winners and losers, it isn’t a global recession trigger.

Note, none of these issues has the power to shave a few trillion dollars off global GDP, which is what it would take to spark a global recession. All current tariff threats amount to around 0.3% of world GDP, using the IMF’s latest estimate of output. That isn’t nearly large enough to offset this year’s projected growth. Rate hikes aren’t contractionary unless they invert the yield curve, which the Fed remains reasonably far from doing. Cheaper oil hurts some Energy firms’ earnings, but it can benefit many other industries. Oil refiners benefit from lower input costs—chemicals firms too. Heavy consumers of plastics benefit alongside Consumer Discretionary, as folks can shift purchases from gas to other things. (Perhaps well-timed, considering holiday shopping is basically upon us.) Firms with high shipping or fuel costs likely aren’t fretting falling oil, either. Not that you should ditch Energy stocks and hoard winners from a short term oil price swing, but it does show how the plusses and minuses can largely offset each other. Finally, we think it is unrealistic to presume a messy Brexit makes all commerce between the UK and EU stop. If anything, just getting on with it will enable businesses to know which contingency plans to execute, which should help unleash some pent-up activity.

Overall, we think stocks have far more positives going for them than negatives. Uncertainty is high right now. But as it fades, relief should ultimately power stocks higher, in our view. Maybe not today, tomorrow or next week. But at some point the tide should turn. Being invested in accordance with your long-term goals, rather than trying to dance around volatility, is the best way to be ready.

[i] Source: FactSet, as of 11/19/2018. S&P 500 total return, 10/29/2018 – 11/19/2018. MSCI World Index return with net dividends, 10/29/2018 – 11/19/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today