Personal Wealth Management / Economics

Tax Reform Gridlock

Many believe this rally is based on tax cut excitement. We disagree. Here is why.

Sunny skies for stocks at the corner of Government and Gridlock. (Photo by JamesBrey/iStock.)

Editors' Note: MarketMinder does not recommend individual securities. The below merely represent a broader theme we wish to highlight.

A widely believed theory-hard to confirm[i]-argues stocks' rally since the election owes itself, in large part, to anticipated corporate tax cuts. Accordingly, proponents believe that if tax reform doesn't pass, stocks will surrender their gains. We see a few holes in all these arguments, and if tax reform doesn't pass, stocks should be fine.

If markets were rallying on high hopes for business-friendly tax plans, one would expect said tax plans to actually be uniformly business-friendly. Yet they aren't. They would create winners and losers, and there is some evidence the losers would outnumber the winners. For example, while there is no "Trump tax plan" per se, on the campaign trail he promised to slash corporate tax rates to 15% from 35% and let corporations repatriate foreign profits held abroad at a special, one-time 10% rate. Sounds pretty pro-business! Except he also pledged to end deferred taxation of future foreign profits. They'd be taxed immediately, regardless of whether firms brought them home-a pretty radical change that isn't to many companies' benefit. And hey, even if the 20 percentage point reduction to statutory rates happens, other changes he talked up-closing loopholes and reforming the tax code broadly-could mitigate the benefit.[ii] Few corporations pay anywhere near the statutory rate, using tax code wrinkles to lower their bill. If an eventual plan closes them, firms could pay more, not less.

Since the inauguration, President Trump has allowed Congress to take the lead on crafting a tax reform package. The main House proposal would lower corporate rates to 20%, but also includes a "border-adjustment tax" that places a 20% tax on imports. Theory being, this tax will fund the broader rate reductions while boosting US competitiveness. However, this is dubious theory. It is highly likely importers would pass the tax on to American consumers and businesses. Now, House proponents argue the US dollar would likely appreciate substantially-making imported goods cheaper for US consumers and offsetting the tax. But that is an uncertain forecast of a possible outcome that could be influenced by a wide array of variables. A border-adjustment tax risks negatively impacting broad swathes of the US economy, namely retailers and US consumers, but also many manufacturers that source parts and materials from abroad, like automakers and oil refiners.

To those arguing stocks are pricing in a tax cut, what of this aspect? A border tax could hurt Walmart, which imports much of what it sells. And yet, Walmart is approaching all-time highs. Similarly, GM-the US's largest car producer (whose supply chain extends globally)[iii] and Valero-the largest US refiner (which imports crude oil a fair bit)-are both near record levels. Incidentally, if a border tax were imposed, Valero's CEO said they'd just, "move the price onto the consumer." Raising gas prices at the pump and angering constituents are probably not high on House Republicans' to-do lists. Similarly, Congressmen from border states and in port areas likely have a strong incentive not to rock the boat. For every person who sees tax reform through a very bullish lens, it seems likely an equal number fear import taxes and the loss of deductions.

Business Unfriendly Tax Reform Isn't Likely to Pass

But none of this seems all that close to becoming signed legislation. Treasury Secretary Steven Mnuchin talked about an August passage last week, but in the same breath announced that he understands the concerns over proposed legislation and "we're going to have a plan that addresses these concerns." President Trump also expressed reservations about the border tax, but has since contradicted himself on its merits. Talk is cheap.

Whether the border tax is a red herring or no, tax reform including it faces a tough road. The House and Senate are far apart, and the administration has made little effort to bridge the divide in this regard. And it takes only three GOP Senators to block it. So far Senators Tom Cotton (R-Arkansas), David Perdue (R-Georgia), Mike Lee (R-Utah) and John Cornyn (R-Texas) have all signaled their opposition.

Don't Overrate Tax Changes

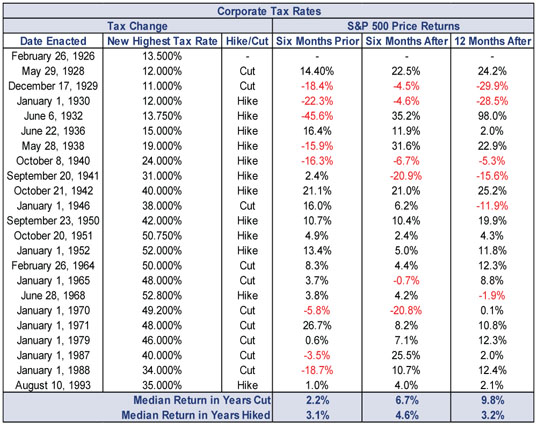

Finally, those who argue the market is pricing in big action on taxes now presume there is a powerful bullish reaction to historical corporate tax cuts-yet there isn't. We get why people think corporate tax proposals matter to stocks-tax changes do impact the bottom line. However, historically, tax cuts (corporate, individual or capital gains) haven't been inherently bullish (or bearish), and tax hikes aren't inherently bearish (or bullish). Because tax cuts are subject to endless debate[iv] before they ever get passed-if they ever get passed-by the time any changes go into effect, markets have probably discounted them. Looking at Exhibit 1, whether there was a corporate tax cut or hike, overall and on average, stocks rose over the next year. And while the 12-month forward return following corporate tax rate cuts is higher, it's worth noting that it is right around average for stocks-not hugely positive.

Exhibit 1: Stocks Aren't Too Affected by Corporate Tax-Rate Changes Regardless

Source: Global Financial Data, Inc., Internal Revenue Service, as of 9/16/2016. S&P 500 price returns, 12/31/1925 - 9/15/2016. Data are weekly from 12/31/1925 - 12/31/1927 and daily thereafter.

Tax rates and rules are only one input to corporate profitability. Interest costs, depreciation, capital investments and, of course, sales matter, too. At any given time, operations influence earnings a whole lot more. Plus, it's a big world. US tax rates are even less of a market driver when you think globally. And it isn't like US stocks have suffered for having the developed world's highest corporate tax rate for the last few decades.

Whatever your view of the specific measures that may or may not eventually emerge, it's a mistake to think tax cut expectations are the key market driver today. Those arguing otherwise are offering an opinion, but in our view, that opinion overlooks the fact not all the ideas are plausible, positive or politically popular.

[i] And the harder to confirm, the more widely believed.

[ii] Like capping tax deductible corporate interest expenses.

[iii] With many parts sourced from NAFTA partner Mexico.

[iv] Like now!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today