Personal Wealth Management / Market Analysis

The Correction Returns

Global markets have renewed their correction, but we believe this isn't a time to sell.

It's official: Global markets breached September's low this week, renewing the correction that began last year. On paper, things aren't drastically worse than they were at the prior low. On September 29, the MSCI World Index closed -14.4% below its prior high (May 21, in US dollars).[i] Wednesday, it closed -14.7% below that peak.[ii] For UK folks investing in sterling, the decline is smaller-a -12.0% drop from the peak, still above the late-summer low.[iii] If you're Canadian, investing globally in Canadian dollars, world stocks are down just -5.6% from a record high set December 29.[iv] Yet for many, the decline feels much worse-probably because most media commentary is far less calm. Then, "stay cool" was the media's rallying cry. Today, fear is surging and apocalyptic forecasts abound, making it difficult to stay disciplined. That's all the more reason to take a deep breath, remember volatility is normal, and avoid the temptation to sell. In our view, if you're investing for long-term growth, the risks of getting out far outweigh the risks of staying in.

We still have every reason to believe this is a correction (sharp, sentiment-driven drop of -10% or worse), not a bear market (longer, deeper, fundamentally driven decline). As far as we can see, there is no identifiable fundamental cause-just rehashed, long-running false fears. China's situation hasn't changed. Officials are still allowing the economy to slow gradually as they transition from heavy industry and investment to services and domestic consumption. They're also still taking a haphazard approach to stabilizing the domestic stock market, which remains isolated from the rest of the world and isn't a leading indicator for their economy. Neither development means the long-feared hard landing has finally arrived. Manufacturing and trade have slowed globally, but this isn't new, and the global economy is still growing. Commodity-heavy countries like Brazil and Russia are deep in recession, but growth elsewhere more than offsets their troubles. S&P 500 earnings are projected to decline again for Q4, but the Energy sector remains the culprit. Excluding Energy, earnings continue rising. And not once has sentiment gotten too far out over its skis. Investors have largely been too skeptical, not overly optimistic.

Unless you have a strong, fundamental reason to be bearish-unless you can see real, sizable negatives few others see-staying in stocks is probably wisest. Volatility is normal in bull markets. Pullbacks happen regularly. So do corrections. Sometimes corrections are short, a quick V-shaped move. Sometimes they are longer and double-bottom, like this one and 2011's. They have no set length or pattern. This correction might feel extra-severe after markets went about three years without a single correction, but it isn't unusual. It is markets being markets, trying to fool and shake out the weak and nonbelievers.

Corrections begin without warning, but they also end without warning. The recoveries are often as steep as the declines. If you have ridden out the correction thus far, we think the biggest risk you can take is to sell now. It would lock in your losses, and you would face a high likelihood of missing the rebound. In marketspeak, this is called getting whipsawed, and it is painful. You might get short-term relief from selling out. But the deep regret of seeing stocks rise past you often dwarfs it, and then you face a tricky question: When to get back in. It also makes your long-term goals that much harder to reach. As Allan Roth wrote in Thursday's Wall Street Journal: "Despite our instincts, it is actually better to buy stocks after they have gone on sale than after a surge. Not to overstate the obvious but it is still a good idea to buy low and sell high." Friends: A time to buy is also a time to hold on.

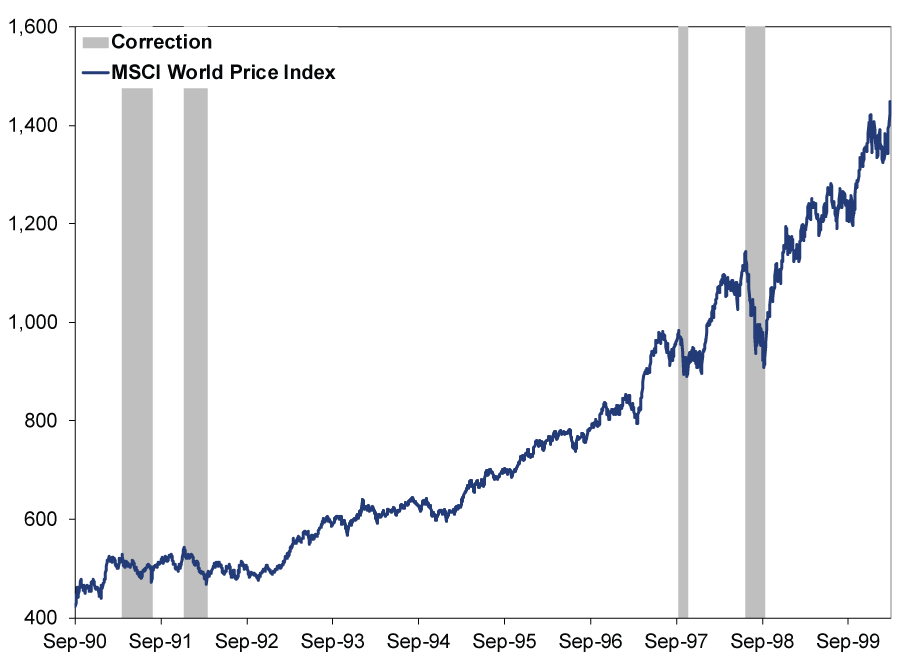

Bull markets' average annualized return is about 20%. That 20-ish percent includes many, many corrections. As they happen, they can feel like a sucker punch. The rug being ripped out from under you. But then they end, and stocks carry on, and when you look back on the entire bull market, those corrections-even the big ones-look like small blips. The long 1990s bull markets illustrates this to a T. Those big full bull-market returns were the reward for riding some big short-term ups and downs.

Exhibit 1: 1990s Bull Market and Corrections

Source: FactSet, as of 6/18/2014. MSCI World Index price level, 9/28/1990 - 3/27/2000.

If you've stayed invested for this entire correction, we tip our cap. Good job thus far, but know that it may not be over. Short-term moves are unpredictable, and no one can know when this correction will end. The S&P 500 finished Thursday up nicely, and we would love it if this were day one of a rebound. But the bottom will be clear only in hindsight, and another leg down could lurk. It is impossible to time any of this with precision, hence why it's so important to think in broad brushstrokes: If the market is down over -14%, and there is no visible, fundamental reason for a bear market, then we must be in a bull market. That being the case, whatever downside might lie ahead should be far smaller than what we've just endured. Trying to skirt a potential small drop just isn't worth the transaction costs and likely missed upside.

In investing, like life, trials test us but ultimately make us stronger. Developing steely nerves and a long-term perspective during this correction can help equip you for those that follow. So take a deep breath, mute the TV punditry, log out of your online account, and put some distance between yourself and that "sell" button. It might feel weird today, but in the long run, you'll thank yourself.

[i] Source: FactSet, as of 1/14/2016. MSCI World Index price return in USD, 5/21/2015 - 9/29/2015.

[ii] Source: FactSet, as of 1/14/2016. MSCI World Index price return in USD, 5/21/2015 - 1/13/2016.

[iii] Source: FactSet, as of 1/14/2016. MSCI World Index price return in GBP, 4/10/2015 - 1/13/2016.

[iv] Source: FactSet, as of 1/14/2016. MSCI World Index price return in CAD, 12/29/2015 - 1/13/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 1 - June 52026-06-08

-

Market Analysis Latest Tariff Threats Lack Terror for Markets2026-06-08

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, Global Trade, ECB Meeting

2026-06-08

2026-06-08 -

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today