Personal Wealth Management / Market Analysis

The Curious and Fallacious Case of the All-Powerful Fed

The Fed’s powers to impact the economy are overstated and overrated, in our view

Did you hear? Some experts believe the Fed looks vulnerable and unprepared to deal with the next crisis, so it should update its policy toolkit.[i] With new Fed head Jerome Hayden Powell waiting in the wings (and outgoing Chair Janet Yellen departing the central bank when he takes over), the time may seem ripe for change. In our view, though, this is yet another example of the folly of seeing monetary policy as an all-powerful tool that directly and immediately impacts the economy. Investors shouldn’t overstate what the Fed can and can’t do.

Folks within and outside the Fed have different ideas about how to “improve” monetary policy to meet today’s needs. Some have argued for raising the Fed’s target inflation rate above 2% while others, like San Francisco Fed President John Williams, have suggested “price level targeting” (meaning the Fed will keep short-term rates low until CPI or PCE reaches a place policymakers deem appropriate). Some financial market experts claim the Fed needs to revamp its “forward guidance” communication and become less predictable in order to remove market complacency.[ii] While some of these ideas are well-intentioned, they also seem to be overcomplicating matters. We don’t think it’s necessarily a bad thing for the Fed to target inflation—pursuing price stability is a fine aim for a central bank—but obsessing over the level isn’t necessary. A specific CPI or PCE level doesn’t determine when things go from good to bad. Not only that, the Fed’s existing targets and framework are arbitrary to begin with.

Consider that annual 2% inflation target. Part of the Fed’s congressional statutory mandate is maintaining “stable prices,” but that doesn’t specify what the “right” amount of inflation is. Rather, the FOMC formalized a 2% inflation target in 2012 because they determined that to be “most consistent over the longer run with the Federal Reserve’s statutory mandate.” Yet there is nothing magical about 2% in and of itself. Inflation has mostly lagged 2% since 2012, but that hasn’t stopped the US economy from expanding. Plus, going back several years before the Fed formalized its target rate, inflation was as high as 3.8% in 2005—right in the middle of another economic expansion.

Moreover, the Fed's preferred inflation measure is the PCE price index, which is another arbitrary choice. In US inflation stories, media usually cite the Bureau of Labor Statistics’ Consumer Price Index—why not use that? Also, which prices are best to track? Why not use “core” inflation, which excludes volatile energy and food prices? The plunge in oil prices starting in 2014 wreaked havoc on all-price indexes, but core inflation gauges didn’t gyrate much. Should an oil crash dictate monetary policy? And if not—and the Fed writes it off as “transitory” (as they did)—what’s the point of targeting a headline index? And are we to believe the Fed will suddenly get better at meeting a target if it’s a higher arbitrary number? Or cutting rates to meet the old target while still missing the new one? So many questions!

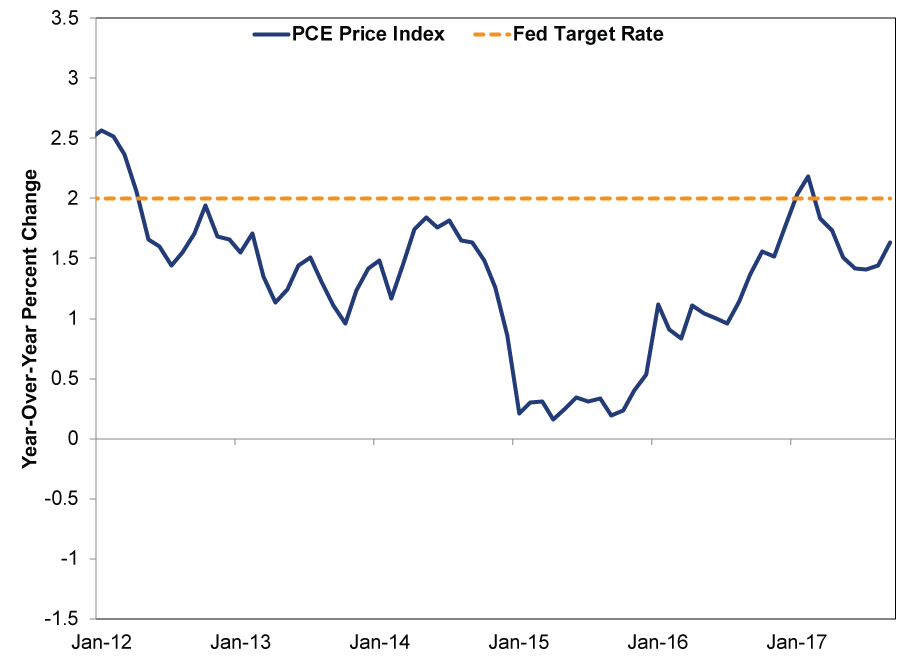

Besides the sheer arbitrariness of the Fed’s criteria, we have doubts monetary policymakers could do what they set out to do. They just aren’t as powerful as commonly perceived. For example, despite the Fed’s best efforts, they haven’t been able to hit that 2% target rate since establishing it almost six years ago.

Exhibit 1: PCE Price Index Since January 2012

Source: FactSet, as of 11/21/2017.

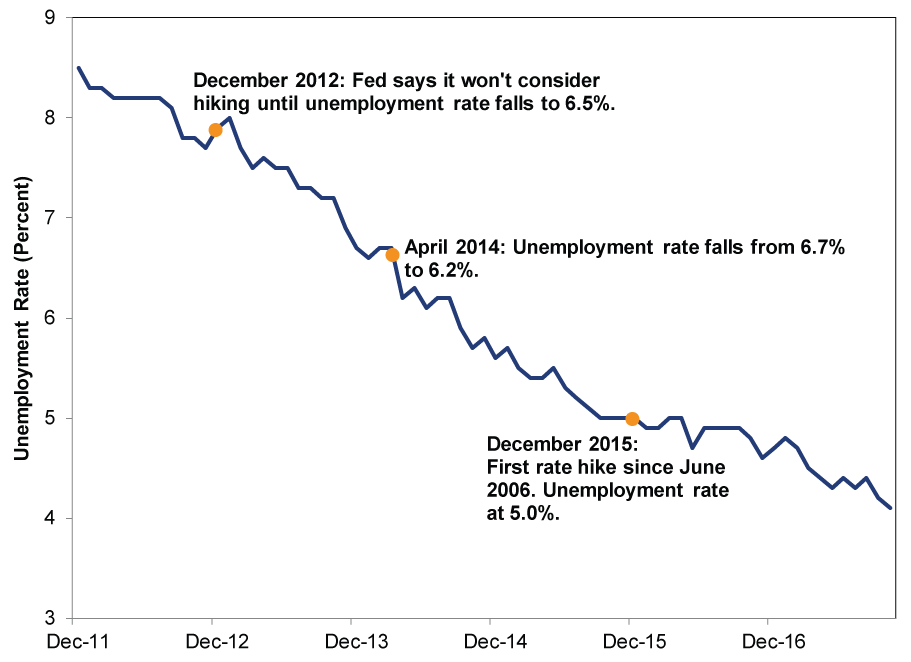

Another example: The Fed has said it would act once certain gauges hit specific levels—only to backtrack later on. Back in December 2012, the Fed said it wouldn’t consider an initial rate hike until the unemployment rate hit 6.5%. Well, unemployment fell faster than they anticipated, leaving the Fed to hem, haw and change their minds.

Exhibit 2: The Fed’s Fickleness With Unemployment

Source: FactSet, as of 11/20/2017.

These are just two recent examples, but the Fed hasn’t shown any ability to fine-tune policy. Yet many seem to believe the Fed can control economic output by simply pulling a lever or pushing a series of buttons, like the Wizard of Oz fiddling with his flashing lights and fog machine. If it were that easy, we believe policymakers—both in the monetary and political realm—would have discovered it and used it to their advantage by now. Push the big friendly button while pulling the green lever and hopping on one foot to get faster growth! Yank the chain if things overheat! Instead, we agree with the wise Milton Friedman, who once noted, “The Fed has had very few periods of relatively good performance. For most of its history, it’s been a loose cannon on the deck, and not a source of stability.” Given the Fed’s inability to hit its stated goals and targets, why should anyone be confident in them nailing new ones?

Moreover, this overlooks and overcomplicates the Fed’s original purpose—not to mention an already sufficient toolkit. While the Fed seems to be watching everything from unemployment to asset bubbles these days, it was originally created in 1913 to serve as lender of last resort in the event of a financial crisis (e.g., step in when a solvent bank lacks liquidity to prevent a broader bank run). While the Fed today has plenty of new policy prescriptions and an alphabet soup of solutions, it also has simple, tried and true ways to fulfill that lender of last resort role. For example, the Fed could lower the discount rate below the fed-funds rate. This means banks can borrow more cheaply from Fed, lend to other financial institutions at a slightly higher rate and keep the spread. Besides offering an incentive for financial institutions to borrow and lend from and to each other, it would help boost liquidity and get money moving—one of the primary issues during a recession. Yet when the financial system was liquidity-starved in 2008, the Fed didn’t even use this readily available tool. Instead, it outsourced its crisis-management role to the Treasury. We aren’t trying to pile on or put the onus on the Fed to be perfect and never make a wrong decision. But it has proven to be a very imperfect institution—so we don’t see why folks should bestow so much faith in its abilities.

While we don’t know how a Powell Fed may act in the future—nobody knows, despite what plenty of analyses today claim—we don’t believe the Fed needs to revamp itself to better perform its role in the future. It already has some simple—and effective—tools at its disposal that have fallen by the wayside.

[i] Perhaps they were able to find something at a Cyber Monday sale!

[ii] You might say they want the talking Feds to stop making sense.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today