Personal Wealth Management / Economics

The Curious Tale of Mario Draghi’s Helicopter

Inside the wacky world of "helicopter money."

What if these helicopters dropped a lot of money? Photo by Mark Wilson/Getty Images.

Look out, "bazooka," you're about to be replaced by a new central bank buzzword: "helicopter." With the eurozone still battling supposed deflation and sluggish growth after a year of quantitative easing (QE), many fear the ECB's much heralded monetary rocket launcher has about as much punch as a pea shooter, and more firepower is in order. Enter the metaphorical helicopter, in which ECB chief Mario Draghi could fly over the eurozone, dropping free new money for the entire populace. This, according to conventional wisdom, could juice spending, growth and inflation, finally rescuing the bloc from falling prices and a lackluster economic recovery. It isn't the most outlandish idea in the world, and unlike QE, it would raise the quantity of money in circulation. But there isn't much evidence it would provide a lasting boost, and it wouldn't address the fundamental cause of falling prices in the eurozone: cheap oil. For now, all the helicopter talk is just that-talk-and probably won't become reality any time soon, which should be just fine for markets.

The concept of "helicopter money" has been around for decades. It entered economic pop culture in 1969, when Milton Friedman discussed it in his essay, The Optimum Quantity of Money. Friedman asked readers to imagine a hypothetical society where nominal national income is $10,000 per year, and society chooses to hold $1,000-or 5.2 weeks' worth of income-in cash. Then, one day, a helicopter flies over and drops $1,000 in bills over the community, which the residents scoop up. In his first scenario, each resident gathers the same amount of money:

If every individual simply decided to hold on to the extra cash, nothing else would happen. Prices would remain what they were before, and income would remain at $10,000 per year. The community's cash balances would simply be at 10.4 weeks' income instead of 5.2.

But this is not the way people would behave. Nothing has occurred to make the holding of cash more attractive than it was before, given our assumption that everyone is convinced the helicopter miracle will not be repeated. (In the absence of that assumption, the appearance of the helicopter might increase the degree of uncertainty anticipated by members of the community, which, in turn, might change the demand for real cash balances.) ...

We know only that each individual will seek to reduce his cash balances at some rate. He will do so by trying to spend more than he receives. But one man's expenditure is another man's receipt. The members of the community as a whole cannot spend more than the community as a whole receives-this is precisely the accounting identity underlying the multiple faces of national income. It is also a reflection of the capital identity: the sum of the individual cash balances is equal to the amount of cash available to be held. Individuals as a whole cannot "spend" balances; they can only transfer them. One man can spend more than he receives only by inducing another to receive more than he spends.

It is easy to see that the final position will be. People's attempts to spend more than they receive will be frustrated, but in the process these attempts will bid up the nominal value of services. The additional pieces of paper do not alter the basic conditions of the community. They make no additional productive capacity available. They alter no tastes. They alter neither the apparent nor actual rates of substitution. Hence the final equilibrium must be a nominal income of $20,000 instead of $10,000, with precisely the same flow of real services as before.

In the second scenario, the money isn't evenly distributed, but the result was the same. The winners would want to shed their excess cash, while the losers would want more of the loot. Thus the winners would spend more, transferring their spoils to the losers, but society as a whole wouldn't spend any more than in the first scenario. Hence the community would end up with a $20,000 nominal income as prices doubled. Presto, inflation!

But it's only a one-time boost. As Friedman went on to show, you get sustained, repeated growth and inflation only if you repeat the helicopter drops-or, as Friedman put it, money "raining down from heaven" at a steady and predictable rate. But in both cases, the growth isn't real, either in the tangible or inflation-adjusted sense. The economy might look bigger and richer, but production hasn't risen. People aren't better off. Living standards aren't improving. If higher prices are the sole goal, great, but everything else is a trick of the eye, which raises a question: What's the point? Answer: to jumpstart demand when the private sector has no mojo-usually in the depths of recession. That temporary boost is supposed to get money moving when it would otherwise stand pat, potentially accelerating the rebound a bit. Cycles always turn, with or without fiscal or monetary stimulus. But greasing the skids a bit can help.

The eurozone, of course, is not presently in recession. It has grown 11 straight quarters, and its business cycle dating committee has confirmed the recession ended after Q1 2013. But growth has been geographically uneven and low on an aggregate basis, and-more importantly, in the ECB's mind-consumer prices are weak. Many there hold the mistaken belief that falling prices create a "deflationary mindset," where people stop spending as they anticipate further price declines, creating a vicious circle of falling prices, falling spending and economic contraction. It isn't true. Consumers are spending just fine as prices fall. But the myth persists and so do the increasingly bizarre attempts to stimulate prices.

Sooooo...would helicopter money work? Meh, who knows. The primary culprit for falling consumer prices is energy, thanks to the commodities downturn. "Core" prices, which exclude energy and fresh food, are rising at an ok pace. So are service prices. As oil prices stabilize, inflation elsewhere in the economy should be more apparent. But the only thing the ECB could really do to accelerate the process would be to sabotage some oil fields, and we are pretty sure that isn't in Mario Draghi's remit.

As for the impact on economic growth, the very limited historical evidence suggests it would be as Friedman theorized: negligible and temporary. Note, this evidence excludes QE. Former Fed head Ben Bernanke earned the nickname "Helicopter Ben," but QE wasn't a helicopter drop in the literal or metaphorical sense. Helicopter money goes directly from the government to the people. QE used banks as an intermediary, under the assumption they'd use the new money to lend enthusiastically. But they didn't. Most of it sat on their balance sheets as excess reserves instead of backing new loans. The same happened in the UK and Japan, and now it's happening in the eurozone.

In practical terms, "helicopter money" would be a government handout financed by the central bank. Government issues bonds, central bank prints money to buy them, government doles out that money to people. UK Labour Party leader Jeremy Corbyn has called for a slight variance on this, dubbed "people's quantitative easing," through which the Bank of England would buy new infrastructure bonds from Her Majesty's Treasury, financing new construction projects nationwide. But this would still have a middle man, namely, the builders. Perhaps the closest analogous event is the US government's economic stimulus payments during the 2001 and 2008 recessions, which went to most low and middle-income households. Though the Fed didn't monetize these, they were widespread cash drops, so they mostly fit Friedman's parameters.

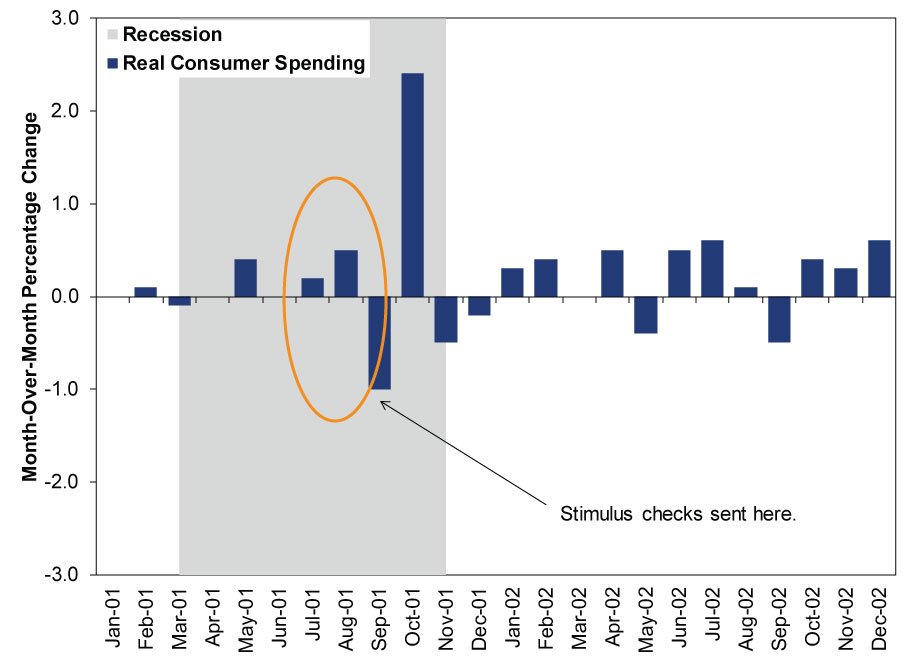

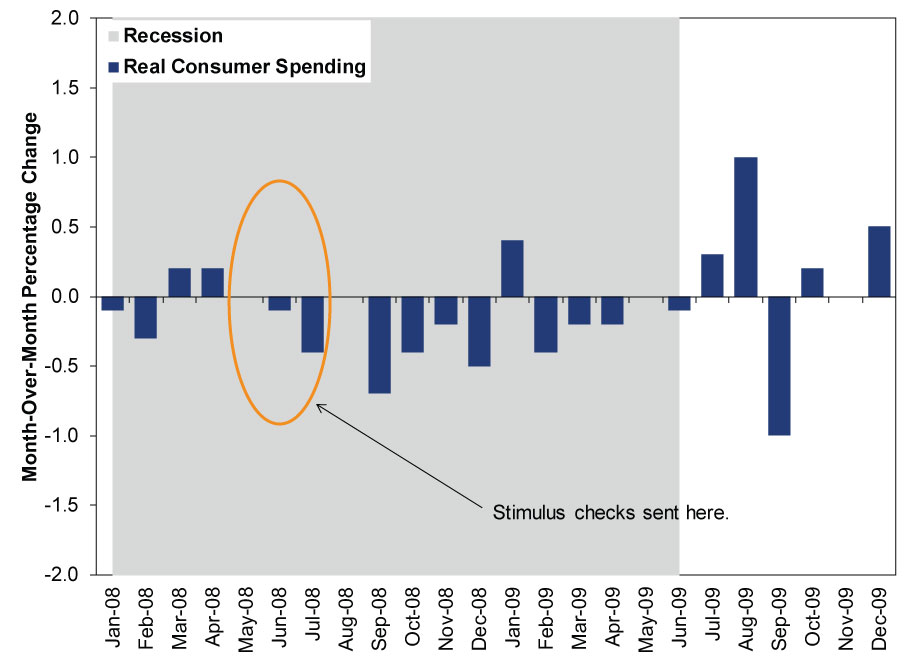

At best, they provided a short-lived boost. Exhibits 1 and 2 show monthly consumer spending growth before and after the checks went out. In 2001, spending jumped immediately afterward, then dropped again as the recession bottomed out. While there is no counterfactual, one could make a strong case that the stimulus checks merely pulled demand forward. In 2008, there is even less of a visible impact. Consumer spending stopped falling for all of one month after the checks were sent, then slid in seven of the next eight. Might it have fallen further without the checks? Sure-again, there is no counterfactual. But the stimulus didn't end the recession, which ran on for another year.

Exhibit 1: Stimulus Checks in 2001

Source: Bureau of Economic Analysis, as of 3/21/2016.

Exhibit 2: Stimulus Checks in 2008

Source: Bureau of Economic Analysis, as of 3/21/2016.

It is difficult to envision a eurozone equivalent of this having any more success. Consumers might spend their windfall, but they might also save it or pay down debt-just as they did with their gasoline savings over the last 18 months. If it juices demand a wee bit, great, but 11 quarters into recovery is generally not when demand needs a jump-start, and there isn't much evidence eurozone consumer demand is struggling. The bloc's economic issues are mostly structural, supply side issues, and helicopter money doesn't address that at all. So the whole thing is just headscratching. Not a huge negative, as a boost in the quantity of money is a boost in the quantity of money, but an ultimately feckless helicopter drop probably wouldn't do anything to shore up investors' crumbling confidence in central banks.

Thankfully, this entire discussion is likely academic. Helicopter talk seems to stem from the mistaken belief central bankers are out of ammunition. Pundits raise it as one bullet potentially left in the arsenal, and central bankers like the ECB's Peter Praet acknowledge it as such, in purely hypothetical terms. It all strikes us as jawboning. As oil stabilizes, boosting CPI, the calls for helicopter money should die down, allowing everyone to get on with life.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today