Personal Wealth Management /

The Curse of the New Fed Head?

With Janet Yellen’s official instatement on Saturday, should investors be worried about the stock market?

Should investors beware the “Curse of the New Fed Chair”? No, we didn’t make up the name—some argue heightened market volatility accompanies new Fed heads as investors grapple with the uncertainty of the new regime, making stocks extra vulnerable during new Chair Janet Yellen’s first few months. And markets were certainly volatile on her first day. In our view, however, the assumption misses a broader point about Fed chiefs—their actions are always uncertain, regardless of how long they’ve been in office. Folks can’t know what Yellen will do, any more than they could know what Ben Bernanke would do these last eight years, Alan Greenspan before him, Paul Volcker before him and, well, you get the drift. We can only weigh decisions once they’re made. That said, some good news: The curse isn’t real. There is little evidence suggesting new Fed heads materially impact the market one way or the other.

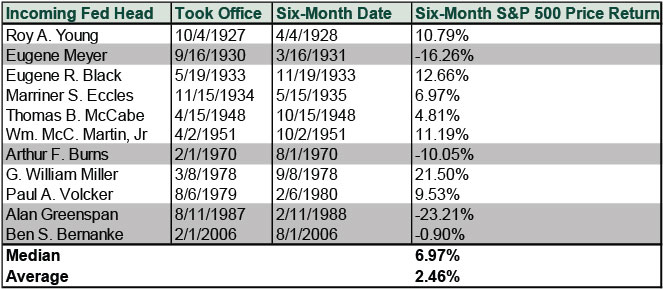

Consider market returns in the first six months of a new Fed head’s term. If you take all 11 Fed chairs since 1927, the median S&P price return six months after they took office is 6.97%, and the mean return is 2.46%—not great, but not terrible. (Exhibit 1) Only four saw negative returns, and there isn’t much (if anything) to suggest a new face at 20th and Constitution was why.

Exhibit 1: S&P 500 Price Index Returns Six Months after Fed Heads Took Office

Source: Fisher Investments Research, Global Financial Data, accessed 1/27/2014.

Take Eugene Meyer, who saw the second-worst six-month return. He took office shortly after the Great Depression began. The day he started, the S&P 500 Price Index was 33.4% below its 9/6/1929 peak.[1] The S&P plunged -43.4% during his first 12 months, but that was largely a function of how the Fed dealt with a huge liquidity crisis.[2] Then, the Fed was in its infancy—policymakers didn’t have the wealth of knowledge, experience and history they have today. So while Meyer favored increasing open market purchases to boost liquidity in the banking system, the new Open Market Policy Conference didn’t agree, and the majority voted against adding new reserves—even then, as now, the Fed head was just one vote of many. Thus the Fed tightened the money supply when it should have raised it, and it wasn’t able to serve effectively as lender of last resort—that would have roiled markets no matter who was in charge, old or new. A year of deflation and bank failures followed before policymakers finally came around in 1932.

Arthur Burns also entered during a bear market. The S&P 500 peaked on 11/29/1968. When Burns took over, the index had fallen 21.5%.[3] It fell another 18.5% before bottoming on 5/26/1970, and then a new bull market began.[4] Falling money supply did play a role in that bear market, but that was the handiwork of Burns’ predecessor, William McChesney Martin—he who first quipped about “pulling the punchbowl before the party gets going.” Greenspan, meanwhile, had the misfortune of starting two weeks before the S&P 500’s 8/25/1987 peak and about two months before Black Monday. It’s rather a stretch to say the wild euphoria surrounding stocks when he took over—and its disconnect from a worldwide liquidity shortage—had anything to do with a new Fed head. Coincidence isn’t causality.

Janet Yellen took office on February 1, nearly five years into a bull market. The S&P 500 was down -3.5% in January.[5] That volatility continued Monday and could very well last longer, with Yellen starting during a correction—it’s impossible to predict where markets go in the short term, and whether or not this is a correction will only be clear in hindsight. But whether returns during her first few months are terrible, amazing or ok will rest on many other variables beside monetary policy. Sentiment will play a role, too—markets swing on emotions in the short term—but sentiment will depend on more than investors’ feelings about a new Fed head. If stocks don’t do great, it won’t be because of a curse.

In the long run, markets will weigh the Yellen Fed’s actions. With the Fed’s next meeting scheduled for March 18-19, it’ll be weeks before stocks have anything to weigh. Yellen testifies in Congress between now and then, but testimony is just words—words aren’t actions. Any statements signaling future actions aren’t set in stone. Fed members have a strong track record of saying one thing and doing another—and defying popular expectations. So while some speculate stocks will do poorly because QE might end or do great because short-term interest rates will stay low, all based on their assessments of things Yellen has said or written, the simple truth is no one knows what she and the 11 other voting members will do.

[1] Source: FactSet as of 2/3/2014, S&P 500 Price Index Return, 9/6/1929 – 9/15/1930.

[2] Source: FactSet as of 2/3/2014, S&P 500 Price Index Return, 9/15/1930 – 9/15/1931.

[3] Source: FactSet as of 2/3/2014, S&P 500 Price Index Return, 11/29/1968 – 1/30/1970.

[4] Source: FactSet as of 2/3/2014, S&P 500 Price Index Return, 1/30/1970 – 5/26/1970.

[5] Source: FactSet as of 2/3/2014, S&P 500 Total Return, 12/31/2013 – 1/31/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today