Personal Wealth Management / Market Analysis

The ECB’s Punch Bowl Has No Punch

More quantitative easing would sedate the eurozone, not stimulate it.

A hackneyed cliché occasionally attributed to Albert Einstein says the definition of insanity is doing the same thing again and again and expecting a different result. Welp, the world's central bankers seem to have missed the message. On Tuesday, the ECB announced loan growth slowed fairly sharply in September, which one could take as evidence quantitative easing (QE) isn't so magical. But ECB Chief Mario Draghi and Chief Economist Peter Praet are jawboning about more "stimulus," leading many to believe more QE may be in the offing, perhaps in December. Headlines cheered, proclaiming more QE will be an elixir for the eurozone economy and stocks. However, a closer look reveals QE isn't responsible for this year's improvement in eurozone credit markets, and it's unlikely more of it would jumpstart eurozone growth. The good news for investors, though, is the eurozone doesn't need a jumpstart. Match that with sentiment that still doesn't fully appreciate the fact the eurozone isn't an economic black hole, and you've got a bullish recipe for reality beating expectations.

QE, for the uninitiated, aims to boost growth by injecting liquidity into banks, spurring lending-but it usually misses the target. Mechanically, it works like this: Central banks create new electronic reserve credits, which they swap with banks for long-term assets like government bonds and asset-backed securities. In theory, that frees up bank balance sheets, enabling them to use their new liquidity to back a big bump in lending, thus spurring the economy by boosting the quantity of money. As an added sweetener, the bond purchases reduce long-term interest rates, making borrowing costs cheaper for consumers, homebuyers and businesses. That's the theory.

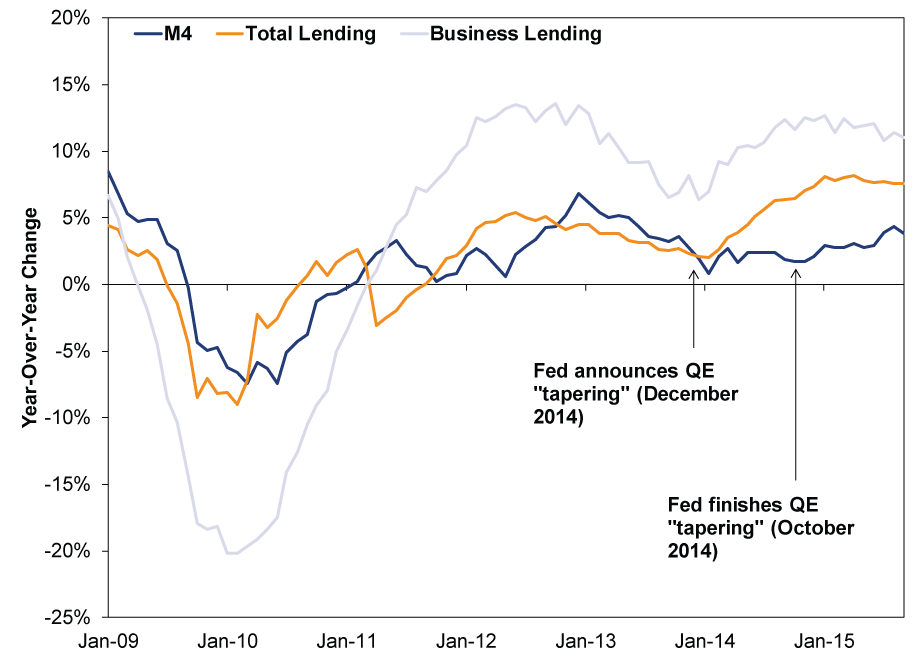

But reality often differs from theory, and it's no different for QE. Reducing long-term interest rates helps borrowers, but long-term rates are also banks' revenues, and short-term interest rates represent their costs. The spread between them, aka the yield spread, represents their profit margin. QE shrinks that spread, reducing banks' potential profits and thus discourages lending-the added risk simply isn't worth it. As a result, QE boosts bank balance sheets and the monetary base, but not the broadest measures of money like M3 or M4. In the US, M4 money supply and lending fell for a long stretch during QE but broadly accelerated after it ended (Exhibit 1)[i]. The UK had a similar experience, with choppy GDP growth during QE and a solid expansion after it ended in late 2012.

Exhibit 1: US Money Supply and Loan Growth, Before and After QE

Source: Center for Financial Stability and Federal Reserve Bank of St. Louis, as of 10/27/2015. Y/Y growth in M4 money supply, loans and leases in bank credit (all commercial banks) and commercial & industrial loans (all commercial banks), January 2009 - September 2015.

The eurozone's program began in March and is currently scheduled to run through next September, with about €60 billion in monthly asset purchases. Because monetary policy hits the economy at a pretty significant lag, we haven't seen much of QE's sedative effect yet-but the more QE the ECB undertakes, the higher the likelihood they sedate the economy instead of juicing it. Eurozone long-term interest rates fell in the run-up to QE, and yield curves flattened, as markets priced in QE's increasing likelihood amid incessant rumor and chatter. 10-year yields jumped shortly after the program launched but have drifted slowly lower since June. Yield spreads in France and Germany are smaller than America's, and spreads in Spain and Italy aren't much wider.

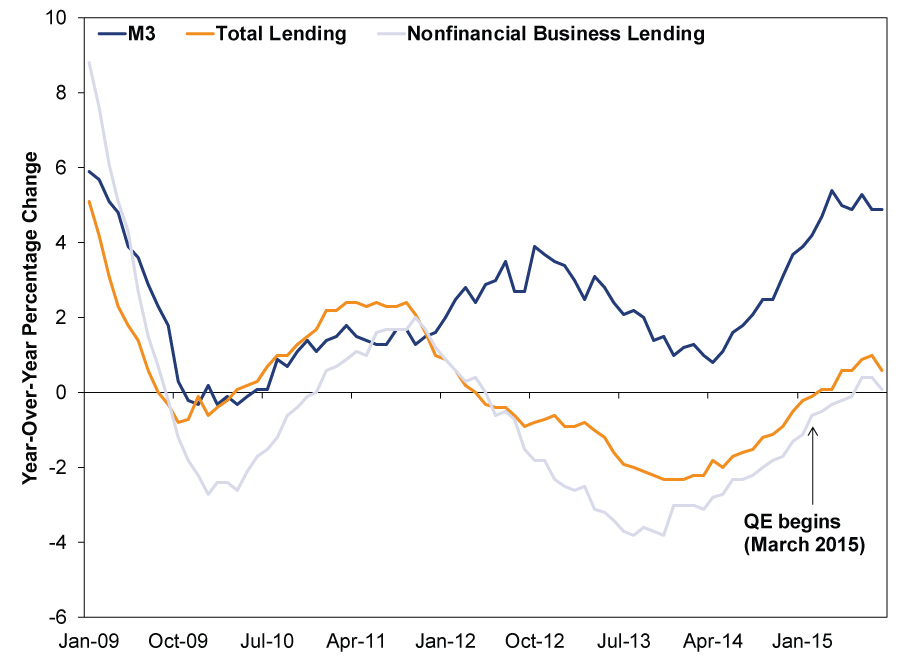

But there is a broad belief QE is working. Since it began, eurozone broad money supply growth (M3) has stayed swift and until September, loan growth was improving-with business lending finally turning positive in July-heightening enthusiasm for the program. But this viewpoint ignores developments before QE was even a speck in Draghi's eyeball. Eurozone money markets started improving in early 2014. We strongly suspect this summer's nice numbers result more from those pre-existing trends than QE itself, a theory September's lending downtick supports.

Exhibit 2: Eurozone Money Supply and Loan Growth, Before and During QE

Source: European Central Bank, as of 10/27/2015. Y/Y growth in M3 money supply, private-sector lending and lending to non-financial corporations, January 2009 - October 2015.

In our view, the eurozone would probably fare best without any more QE-the more bonds the ECB buys, the more pressure they exert on the yield curve. Adding to QE in December or any other time would likely amount to throwing cold water on the economy. Plus, despite the hand-wringing, the eurozone economy doesn't need extra stimulus. It has grown for nine straight quarters-well before QE started. The Conference Board's Leading Economic Index is in a solid uptrend, and Purchasing Mangers' Indexes for services and manufacturing remain in expansion, as do forward-looking new orders. All suggest growth continues. Yes, inflation remains very low, but this is largely due to cratering oil and other commodity prices-overall positive for the bloc. Removing artificial pressure from the yield curve would add another tailwind.

Some suspect officials might cut the deposit rate further into negative territory for an added boost, believing this will push banks to lend idle capital and make QE really work. But negative rates haven't done much for banks or depositors. Banks have largely passed costs on to customers, particularly big corporate depositors, or parked excess liquidity in bonds or at other central banks. Charging for deposits doesn't address why banks were holding huge reserves in the first place-it was because the regulatory environment and flat yield curves discouraged risk-taking. Not because banks earned a small interest payment on reserves. If interest on reserves were that big an incentive, banks wouldn't lend ever.

Good news is more QE shouldn't be a huge negative for euro land. The US and UK managed to grow while QE ran, and the eurozone should have enough fundamental strength to push through, too. We just think investors should keep their expectations in check, because it's highly unlikely the region sees some magical QE pop.

[i] You might notice M4 growth was a tad tepid the first several months after QE began. We suspect that has something to do with the slow growth in Treasury bond supply, a function of the falling deficit. Excluding Treasurys, M4's year-over-year growth rate was about one percentage point faster throughout 2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today