Personal Wealth Management / Market Analysis

The Elocution of Bond Yields

Bond markets have some interesting wisdom to share regarding current weak economy and credit ratings fears.

In the wake of Tuesday’s US debt ceiling deal, two primary stories have dominated headlines: Ratings agencies might still downgrade the US and recent economic data showing continued slow growth, sparking fears of a new recession. Which begs the question: Is this more than just a short-term spate of equity market negativity?

Some assume it does mean something bigger than short-term noise and attempt to mine answers by comparing the duration of selling to the past—finding parallels to events three decades ago (1978 to be specific). But what was so bad about 1978? Stocks rose double-digits amid an equity bull market, and the economy grew in all four quarters. That (among many other examples) should show short-term equity volatility on its own is never indicative of something terrible ahead. More timely and pertinent information to help put recent volatility in its proper context exists—it’s just outside equity markets. Look to bonds.

First, let’s talk about a potential downgrade of the US. Now, as we’ve said, we won’t attempt to forecast what the ratings agencies might opine. And at this time, there’s only one rater to discuss—Moody’s and Fitch announced late Tuesday they’ll maintain America’s top rating at present, though they’re watching. (Thanks. Shouldn’t they always be? Considering that’s their primary role?) That leaves S&P, which remains rather silent as of this writing.

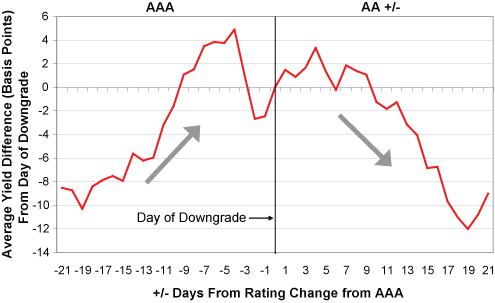

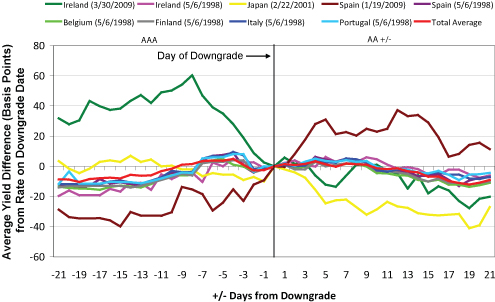

Let’s assume for a moment S&P does downgrade the US. Is this so problematic? If so, one should be able to find past episodes of AAA sovereign downgrades followed by persistently increased interest rates. Since 1998, AAA-rated sovereigns have received an S&P downgrade nine times. Exhibit 1 shows the average movement (equally weighted) of 10-year bond yields 21 days before and after a sovereign downgrade. Exhibit 2 shows the same for each sovereign issuer.

Exhibit 1: Average Sovereign Debt Reactions (10-Year Bond Yield) to S&P Downgrades From AAA

Sources: Bloomberg, Standard and Poor’s, Thomson Reuters, Nomura Securities, Fisher Investments Research.

Sources: Bloomberg, Standard and Poor’s, Thomson Reuters, Fisher Investments Research.

Eight of nine sovereigns had lower 10-year bond yields than on the day of the downgrade within roughly 12 trading days(Spain in 2009 is the not-so-surprising exception). In fact, stretching the timeframe out shows rates generally tend to rise slightly before a downgrade, typically falling after the downgrade occurs. So history doesn’t support the theory a downgrade automatically leads to lasting, far higher interest rates. And US debt in many ways exceeds the attractiveness of the countries referenced here—AAA ratings aren’t the only demand-driver for our debt.

The bond market can also aid in assessing recent economic data. First, let’s be clear—most folks are opining about slow growth. For example, US Q2 2011 real GDP accelerated from Q1 (though growth was tepid). But most media sources seem to gloss over that, instead lumping it together with downwardly revised Q1 growth to discuss +0.8% first-half GDP. True, that’s less than torrid, but bear in mind growth rate volatility is normal, and growth commonly slows only to reaccelerate later.

Meanwhile, US investment-grade corporate bond rates fell Wednesday to near all-time lows. Some in the press attribute that to recent equity market volatility—a possible contributor, but also a very backward-looking one. It seems reasonable the vast majority of bond buyers aren’t buying bonds today based on past equity volatility. Bond investors can be irrational too—just like stock investors. But overall, like stock traders, bond traders buy bonds based on forward-looking assessments of whether the investment likely returns an appropriate amount given the level of risk they perceive. And corporate bond rates at such low levels allude to a very low market assessment of corporate default risk.

From a macroeconomic perspective, if a new recession were actually probable in the immediate future, would corporate bondholders perceive default risk as so low—and down from the recent past? Reason implies they’d think the opposite, which has happened many times when the economy is entering a recession. This is another sign current market volatility and recession fears seem far more like one of the multiple rounds of emotion-driven negativity extant at points during the present bull market—very standard behavior seen regularly during historical bull markets.

In the recent debt ceiling debate, bond markets indicated all along US default risk was virtually non-existent. But the bond market has more wisdom to share: That ratings agencies’ opinions aren’t as impactful as many think (positively or negatively), and currently tepid US growth doesn’t indicate a recession is probable.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today