Personal Wealth Management / Market Analysis

The Elusive Passive Investor

That investors are flocking to passive investment products in droves doesn't make them passive investors.

Over the last decade, index funds-in the form of both mutual funds and ETFs-have risen greatly in prominence in the investment world. Passive products, folks often remind us, are taking share from active products-evidence to media types and pundits that passive investing is on the rise. But, as we've written before, owning passive products does not make you a passive investor.Virtually all managers and individual investors who use passive products do so in an active manner, making their strategy active. There is nothing wrong with that, but it effectively renders the passive vs. active debate moot.

Passive investing means owning the broad stock market, or some mix of stocks and bonds, via index funds-and never veering from this throughout your entire investment time horizon. The idea stems from the belief markets are so efficient it's virtually impossible to beat them.[i] Because passive investment vehicles mirror an index, they perform similarly over time, less their relatively low fees and tracking error-how much the fund deviates from the underlying index. Proponents argue this approach will generate better long-term returns than active managers that deviate further from the indexes. But in the non-theoretical world-real life-very few investors can successfully be passive and reap the long-term benefits.

The supposed evidence passive is winning out over active is the fact retail investors have largely moved away from actively managed funds and into index funds over the last decade or so. But this doesn't mean those buying index funds are employing a passive strategy. Investors must still decide whether to invest in all stocks or a mix of stocks and bonds-their asset allocation. This is an active decision, and arguably the one that most determines whether or not you achieve your long-term financial goals. So is the next layer down, picking which funds to own. If stocks, US or global? S&P 500 or Wilshire 5000? If bonds, government or corporate? More active decisions.

Individual investors aren't the only ones using passive funds actively. Many professional managers do it, mixing and matching narrow index funds in a way that is far removed from the broader market, and rebalancing periodically. Some own up to the inherent activeness. Others don't. But there is nothing passive about this. With or without tactical rebalancing, if portfolio structure doesn't resemble any discernible, identifiable index, it is not passive.

Some firms go so far as to design their own index and then create "index" funds to mirror it, claiming they are "unconventionally" passive. But if we all just make up indexes to link passive products to, then the distinction between active and passive and benchmarking in general has no value or meaning. That's especially true of some of these new, boutique indexes. Some have utterly bizarre selection criteria that can't rationally be anything other than active management dressed in passive's old clothes. Some would-be passive investors get the recipe right, mirroring a broad index and attempting to set it and forget it. But precious few are successful. Setting and forgetting is among the hardest things investors can do, as success requires either ignoring all financial news or resisting every last emotional impulse to trade.

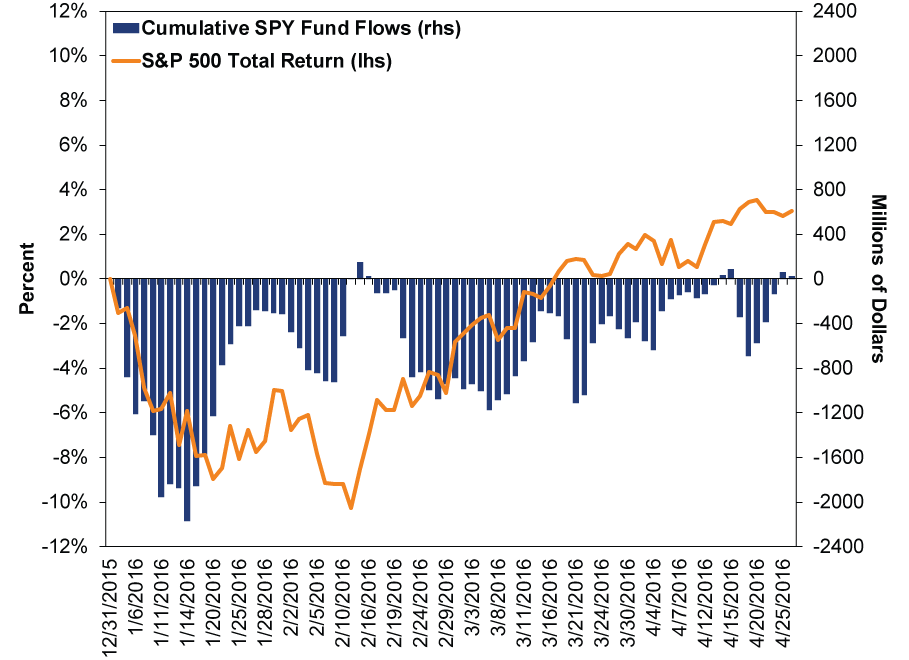

Fear is one such impulse, and a huge one. Corrections and pullbacks often feature steep drops, triggering loss aversion in even the most steely nerved folks. When stocks seem in freefall and headlines warn of doom and gloom, the desire to stop the bleeding can be overwhelming. Index fund investors are just as vulnerable to reacting to fear and volatility as active investors, and they frequently flee, locking in losses-and wait until after stocks have recovered somewhat to get back in, missing gains. Early 2016's sharp downdraft is a good example, as Exhibit 1 illustrates using one major S&P 500 ETF's (ticker: SPY) cumulative net flows. But it is far from the only one.

Exhibit 1: Investors Sell After Stocks Fall

Source: FactSet, as of 4/28/2016. S&P 500 total return and cumulative SPY net fund flows in millions of dollars, 12/31/2016 - 4/26/2016.

Conversely, when markets are booming, many investors find it difficult to resist the urge to lever up, over-concentrate in the hottest sectors or otherwise chase heat. Greed can be just as powerful a motivator as fear and often ends just as badly.

Some firms have figured this out and found a way to capitalize on it, packaging "passive" strategies with ongoing investment advice and counseling-often for an even higher total cost than many active managers charge. Some truly find value in this, and more power to them, but it is quite far removed from cheap index tracking. If the only way people can do passive is with extra service that increases their negative spread vs. the benchmark, that sort of defeats the purpose. Moreover, the proliferation of this service is another counterpoint to the notion that investors are chucking high-cost services for cheap DIY management.

Look, we aren't anti-passive or anti-index fund. If people can actually do passive, great! But the notion that investors en masse have evolved into perfectly disciplined passive investors is sheer myth. The preferred investment vehicle might have changed, but human instincts, emotions and foibles are the same as ever.

[i] This is a fallacy. While markets are quite efficient most of the time, they aren't always so. If they were, there would never be corrections-short-term market pullbacks driven by false fears, not fundamentals.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today