Personal Wealth Management / Market Analysis

The Eurozone’s Underappreciated Improvement

The eurozone economy has several little-noticed positives.

With Greece hogging headlines again, euro fears are back with a vengeance. While the eurozone isn't in perfect shape, there has been a fair amount of economic and political improvement in the region. Greek jitters and deflation concerns have overshadowed many recent small victories-reality is better than most perceive.

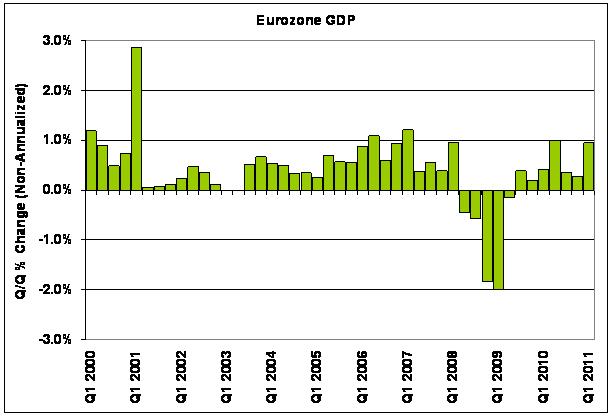

While the eurozone economy isn't growing as fast as the US, it has grown for six consecutive quarters (Exhibit 1). Retail sales are growing at the fastest pace since 2007 (Exhibit 2), and economic data have begun surpassing expectations more consistently as analysts have reduced their forecasts. With broad sentiment stuck between analysts' forecasts of stagnation and headlines' warnings of a deflationary "lost decade," positive (albeit uneven) growth should continue bringing relief.

Exhibit 1: Eurozone GDP Has Risen Six Straight Quarters

Source: FactSet, as of 1/6/2015. Q/Q percent change in real eurozone GDP, annualized, Q4 2010 - Q3 2014.

Exhibit 2: Retail Sales Are Rising at the Fastest Pace Since 2007

Source: FactSet, as of 1/6/2015. Eurozone retail trade ex. auto and motorcycles, February 2005 - December 2014.

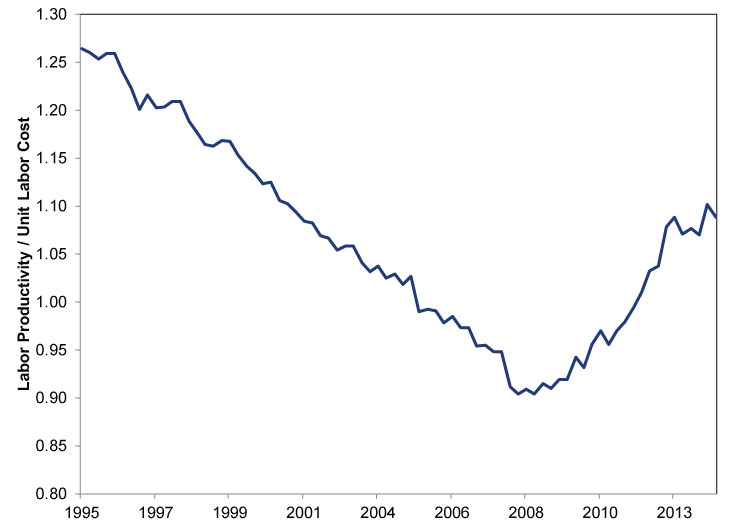

Spain, among the hardest-hit economies during the crisis, is now one of the fastest growing. Spanish Q4 GDP rose +2.8% q/q annualized, accelerating from Q3's +2.0%. One contributor is improvement in the country's labor market, often cited as a major obstacle during the crisis. A 2012 labor reform package made it easier to manage payrolls and negotiate contracts on a factory (versus regional) level. This, combined with larger labor supply, has helped labor costs improve significantly relative to productivity (Exhibit 3). It has also benefited workers: OECD reports suggest the reforms have resulted in about 25,000 new permanent worker contracts each month.

Exhibit 3: Spanish Labor Productivity Has Improved Significantly

Source: FactSet, as of 1/6/2015. Spanish labor productivity divided by unit labor costs, Q1 1995 - Q2 2014.

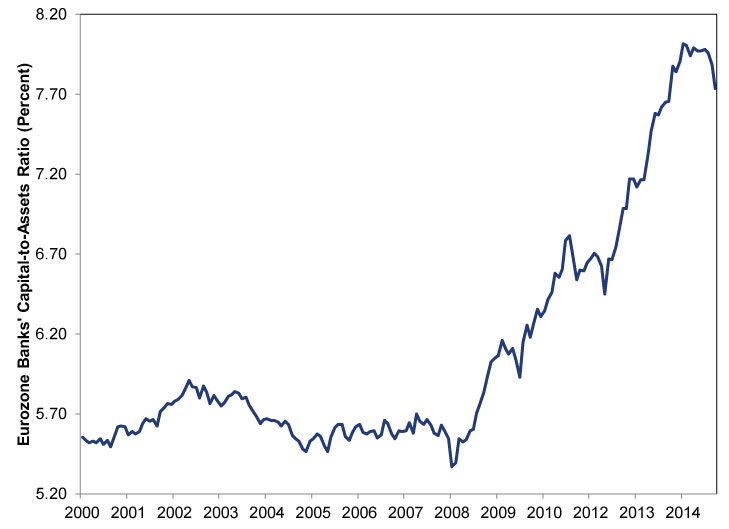

Credit markets have also improved. Banks have significantly cleaned up their balances sheets by retaining earnings, issuing equity and selling assets. Capital levels have increased by almost 50% since 2008 (Exhibit 4). The ECB cited improving conditions in its last two credit market reports, pointing to not only healthier banks, but improving demand. Healthier credit markets should benefit capital-starved small and mid-sized enterprises (SMEs), which compose a significant portion of the eurozone's economy. Loans to SMEs are typically floating rate, so the flatter yield curves (exacerbated by quantitative easing, as discussed here), shouldn't be that strong of a headwind.

Exhibit 4: Eurozone Banks Are Better Capitalized

Source: ECB, as of 1/6/2015. Capital as a percentage of total assets, all eurozone banks, February 2000 - December 2014.

The political front has seen progress, too. Most believe a tighter fiscal union is required for the eurozone's long-term survival. Eurozone leaders approved a permanent sovereign bailout mechanism in 2012, which provides greater financial firepower and a more clearly defined process than temporary programs used in the crisis's early stages. Member-states also established a banking union, which made the ECB the primary bank regulator and established common bank resolution procedures. Though the blueprint will inflict losses on large depositors in failing institutions (similar to Cyprus in 2013), its existence reduces uncertainty about who takes losses when a bank fails and how much national governments must contribute.

The eurozone still has issues, but most are well-known after five years of crisis chatter and likely discounted in eurozone stocks. Even modest economic growth and slow progress towards a tighter fiscal union should exceed overly dour expectations. As this bull market has repeatedly shown, galloping economic growth isn't a prerequisite for solid stock returns.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today