Personal Wealth Management / Economics

The Fed’s Deflated Logic

Fed bond buying isn’t a solution for disinflation—it’s the cause.

While many US economic indicators have picked up lately, one hasn’t: inflation. At first, that probably seems nice—goods and services are staying affordable! But there is such a thing as too-low inflation, and most measures indicate that’s what we have today. Some speculate this means the Fed’s quantitative easing (QE) bond buying must continue—we need the Fed to create money until inflation hits its 2% y/y target. Yet in our view, this is backward—QE can’t fix slowing inflation (aka disinflation). It’s the cause! Inflation likely won’t hit that 2% threshold until the Fed stops QE—a big reason we’d welcome its end (and so, over time, would markets).

Rising prices get a bad rap, but modest inflation isn’t inherently bad—it’s a healthy side effect of growth! It means money supply is rising and capital is moving, giving the economy fuel for growth. It puts the capital in capitalism.

Most observers seem to agree slowing inflation isn’t great—headlines weren’t thrilled with last week’s PPI (producer prices, aka wholesale inflation) or Tuesday’s CPI (consumer prices) numbers. But folks are mixed on the causes. Some cite falling fuel costs, a byproduct of the shale oil boom. And energy was indeed the biggest drag on CPI and PPI. But stripping out volatile energy and food prices, core CPI was still muted—up 0.2% m/m (1.7% y/y) in November. The Fed’s preferred measure, the Personal Consumption Expenditures price index, was even lower at 0.7% y/y in October. Which, naturally, led others to suggest tepid growth, lackluster wages and weak global demand are to blame—and, thus, the Fed should keep juicing demand through QE.

But this perception misses a key point: Inflation is always and everywhere a monetary phenomenon. Thus, so are disinflation and deflation! If you don’t have enough money chasing a given amount of goods and services, prices will fall—and growth will slow. The economy doesn’t have enough fuel! That lack of fuel, in our view, is what’s weighing on growth—and QE is the weight. Its goal is to raise the monetary base, reduce long-term interest rates to encourage consumers and businesses to borrow, and thus raise the broad money supply. It accomplished two of three. By buying $85 billion of long-term assets from banks each month in exchange for newly created reserves—essentially electronic cash in banks’ Fed accounts—the Fed drove down borrowing costs and boosted the amount of money in the banking system. But banks aren’t lending off these excess reserves at nearly the rate needed to jumpstart growth—the monetary base is up over 200%, but broader measures M2 and M4 are up only 37% and about 3%, respectively, since QE began.

Low long-term rates are the reason why. Banks’ core business is borrowing at short-term rates and lending at longer-term rates, and the spread represents their potential profit. Banks aren’t charities—they won’t take the risk of a new loan without sufficient reward. A small rate spread means smaller profits and, thus, tighter credit—fewer loans, less money chasing goods and services, falling prices.

Once QE ends, this should change. Rate spreads have widened amid taper talk—markets are pricing in the end. As bond purchases wind down, they should widen further, encouraging banks to lend more and increasing broad money supply. Many more businesses will get the capital they need to invest in new equipment, technology and people. The more businesses invest, the more money changes hands, and the more it fuels growth—with modestly rising prices as a side effect.

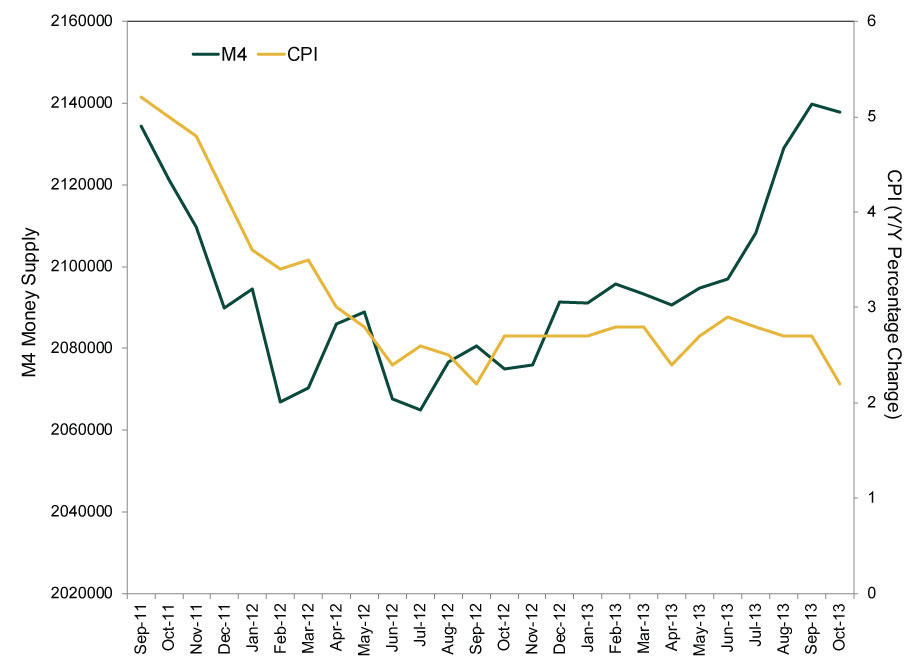

This notion inevitably prompts some folks to worry that with a huge buildup of reserves for banks to lend off of, banks could lend too aggressively, driving inflation too high once QE ends. Right now, this doesn’t seem like a huge risk. For one, the UK hasn’t seen any kind of inflationary backlash after ending its QE program last November. M4 money supply accelerated, but inflation is at its lowest level in four years. (Exhibit 1) Long-term gilt yields—the market’s expectation of future inflation—are benign.

Exhibit 1: UK M4 vs. CPI (Annual Rate)

Source: Bank of England and Office for National Statistics, as of 12/17/2013.

Plus, banks aren’t terribly likely to open the floodgates—don’t expect them all to try to make up for lost time. If they did, they’d likely create a credit supply glut, outstripping demand, and have to lower rates to attract borrowers. That would make lending less profitable again. Banks thus have heavy incentive to tread lightly—especially with capital requirements soon to rise under Basel III. Most likely, loan growth reverts to historical norms.

Not that we dismiss the risk—or the need for the Fed to eventually tighten. But these issues are further down the line, and we’ll have plenty of signals, like long-term Treasury rates. For now, what matters is that when QE ends and businesses shake off its deflationary sedative, the economy should get more fuel, helping growth surprise stocks to the upside.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today