Personal Wealth Management / Market Analysis

The Fed’s Sequestered Logic

The Fed seems to think slow growth justifies continuing QE—we think that’s exactly why they should stop.

Fedspeak. It’s a language filled with nebulous constructs and sentences about 20 words too long. Take this sentence from Wednesday’s no-taper press release: “Household spending and business fixed investment advanced, and the housing sector has been strengthening, but mortgage rates have risen further and fiscal policy is restraining economic growth.” Eeeeh? Don’t worry, we’ll translate: “The economy looks fine overall, but that darned sequester still stings.” And that, folks, is why they didn’t taper. Which is ... a touch confusing. QE isn’t helping—it’s actually doing the opposite of what the Fed wants. Economic activity follows increased private lending and business creation—not more excess bank reserves. Ending QE would likely free up credit, giving the private sector more fuel for expansion and boosting stocks.

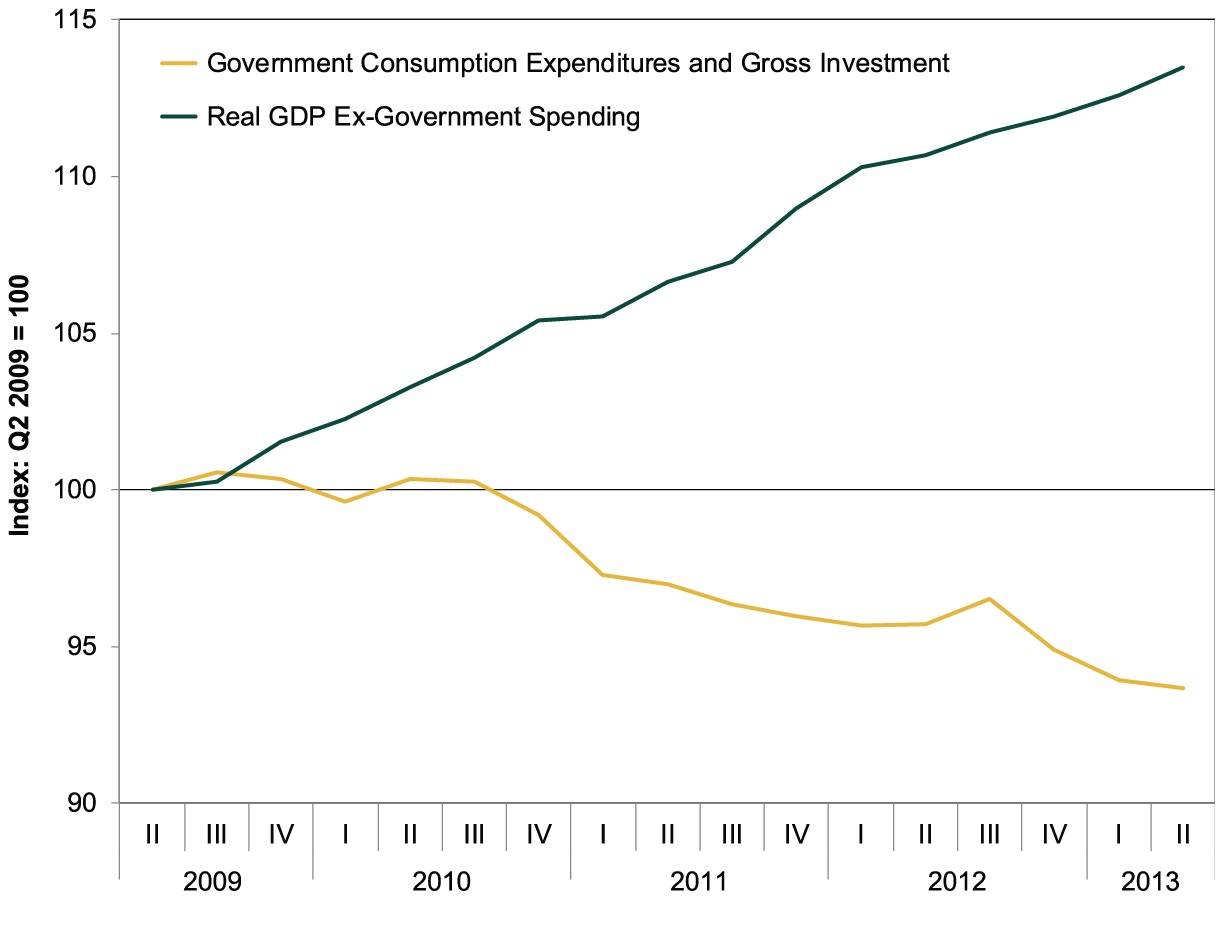

Don’t get us wrong, weak government spending is an incremental negative for the US economy. Demand is demand, and a drop, regardless of where it comes from, is a headwind. But public spending cuts also aren’t exactly as big a minus as the Fed seems to think. We’re still growing—nine straight quarters, likely going on ten. The public sector is merely a part of the economy—and the vast majority of the US economy, the private sector, has more than offset its weakness (Exhibit 1). Put another way, we don’t need stimulus.

Exhibit 1: Government Spending & GDP ex-Government Spending

Source: US Bureau of Economic Analysis, as of 8/29/2013.

Recent employment data tell a similar story. From July 2013 to August 2013, private payrolls increased by 152,000 employees. The most recent Job Openings, Layoffs and Turnover report showed over 3.3 million private sector jobs were open—about 170,000 more openings than a year earlier. Public sector hires and job openings paled in comparison. Long-term employment data agree, too! Since the bottom of the last bear, March 9, 2009, private payrolls have added 4.7 million employees, but government payrolls fell by over 700,000. Here, too, public-sector cuts are a drag but don’t indicate broad labor market weakness.i

So yes, government cuts are a big reason GDP and jobs growth have been slower. And yes, with the sequester seemingly here to stay, faster growth must come from the private sector. The Fed is right! (If overstated.) But the prescription is wrong. Continuing QE likely won’t do much for US economic or employment growth. It isn’t stimulus. The reserves created through QE aren’t multiplying throughout the economy—the Fed’s asset purchases flattened the yield spread, creating a disincentive to lend. So businesses haven’t much used the Fed’s “funny money” to invest in new technology, R&D, equipment, facilities, production and, yes, hire more employees.

We just don’t see how this changes with more QE. As long as the yield spread stays slim, money won’t circulate faster, no matter how many more reserves the Fed adds to the banking system. We don’t need more money—we just need what money there is to move faster. If the Fed stops purchasing assets, long rates should rise, banks should lend more, and businesses should finally get the money to do all the things the Fed wants them to do.

Investors, too, should look to the private sector to tame their taper terrors—stocks have risen despite four-plus years of contractionary monetary policy, not because of it. Think about what corporate America has accomplished even with the Fed hitting the brakes. Q2 S&P 500 earnings growth is estimated at +2.1%, and current expectations are for +3.5% in Q3—the 15th and 16th straight quarters of growth.ii Corporate profits are at all-time highs! Further, other fundamental factors (like a high and rising LEI and growing-but-lean inventories suggesting businesses are struggling to keep up with strong demand) indicate corporate America likely continues expanding.

Now, think just how much stronger the US economy would be if QE ended and net interest margins widened, incentivizing banks to loan more freely. More profitable lending perhaps widens the pool of borrowers banks are willing to extend loans—moving beyond the very strongest corporate and industrial borrowers, where much of this cycle’s borrowing has been centered. Stocks would likely see a boost, too. More private sector expansion likely translates to more earnings growth and better sentiment, giving investors more confidence in stocks’ future profitability. As sentiment begins aligning with healthy fundamentals, folks bid more and more for future earnings, and stocks should feel a swift tailwind. Sequester or no!

i US Bureau of Labor Statistics, March 2009 to August 2013, data accessed 9/20/2013.

ii FactSet, as of 9/13/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Market Analysis Stablecoins Didn’t Eat the Treasury Bill Market2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today