Personal Wealth Management / Market Analysis

The Ghost of a Banking Crisis Past Visits Italy

Recent Italian financial turmoil echoes euro crisis banking troubles-but this expansion should charge ahead anyway.

Editor's Note: MarketMinder does NOT recommend individual securities; companies referenced herein are merely cited as examples of a broader theme we wish to highlight.

The world's oldest bank is at the center of what media presents as the world's newest financial scare-Monte dei Paschi di Siena, a venerable Italian institution known for its rich history and faring poorly on stress tests. Last Wednesday, the bank failed to raise private funds to plug a €5 billion (~$5.2 billion) shortfall (since grown to €8.8 billion) and Italy increased its public borrowing limit to €20 billion to prepare potential rescues for Monte dei Paschi and, potentially, others. This perpetuates a long-running meme that shaky (maybe contagious!) Italian banks could sink the eurozone economy. The issue may finally be coming to a head-and as uncertainty falls and false fears fade, sentiment (and stocks) should get a lift.

Despite new headlines, these issues are old-ancient history, from a market perspective. From 2009 - 2012, most eurozone members faced and dealt with bank weakness, but Italy didn't. Ireland initially capitalized its banks directly, sending deficits skyward and leading to a 2010 EU/IMF/ECB bailout. (Today, Ireland is growing nicely.) In 2009, Spain created the Fund for Orderly Bank Restructuring (FROB)-a bailout fund-and used it to resolve failing institutions and oversee bank mergers (mostly among troubled cajas).[i] In 2012, Spain tapped the European Stability Mechanism (ESM)-the eurozone's permanent bailout fund-in a very special non-bailout bailout,[ii] using €100 billion to recapitalize its banks. Like Ireland, it has recovered well.

During all this, Italy demurred, as nonperforming loans piled up and crimped lending. But in late 2015, Italy bailed in four small banks. Investors holding junior bonds-including some retail investors who had been promised a safe place to stash cash-took it on the chin, with occasionally tragic consequences, including suicides. Bailing in retail creditors under the ECB's bank resolution rules is politically unpalatable-hence Italy's foot-dragging. As a result, the country's banks are ailing, and media types fret capital shortfalls, government bailouts and bondholder haircuts could rekindle the euro crisis. The ECB estimated last month that just 14 Italian banks hold €286 billion of nonperforming debt-nearly a third of the eurozone total. So it suffices to say things aren't great, but that doesn't mean a systemic threat to Italian or eurozone finances is brewing-a fact that may be dawning on investors.

The perspective is rather new: At 2012's outset, conditions looked dire. Italy's debt was nearly €2 trillion, rates on 10-year sovereign debt topped 7%, and adding another €20 billion in debt would have been a challenge, especially since the government already planned to roll over €450 billion of it that year. Coupled with Spain's woes and bailed-out Portugal, Ireland and Greece,[iii] investors feared the euro's days were numbered, as member states would be forced to default and/or revert to national currencies in order to print their way out of debt. With every banking tremor in the peripheral eurozone, headlines screamed the Union was splintering.

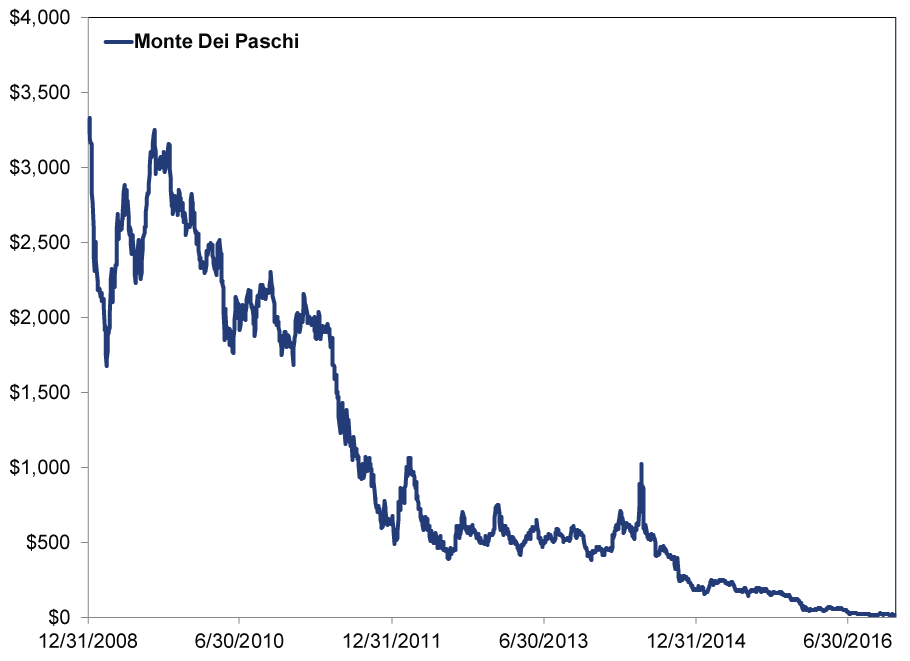

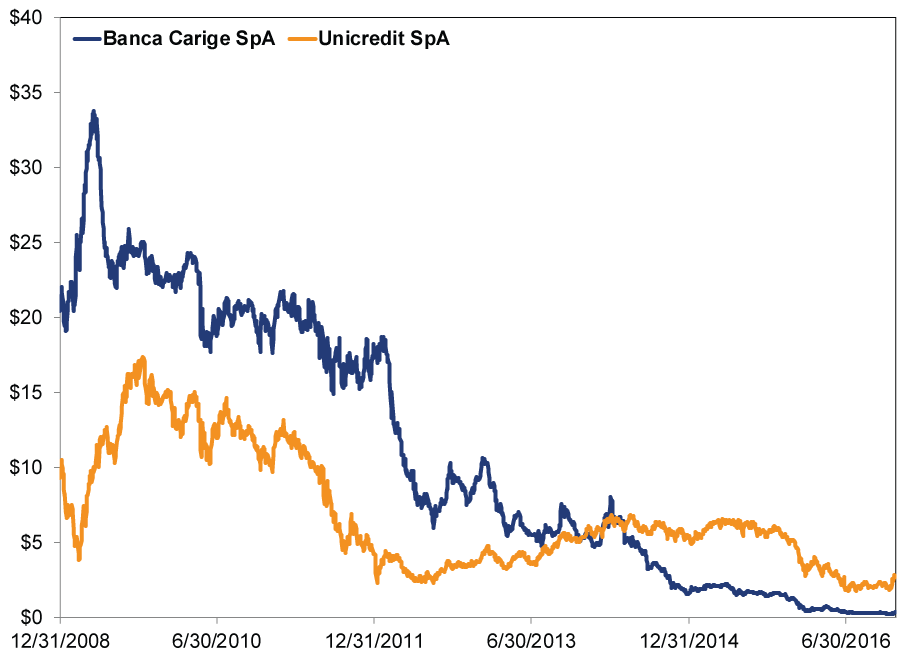

Today, few investors think shaky Italian banks have such power. More seem aware that issues exist, but they aren't big enough to derail the global expansion. Equity markets reflect this: Monte Dei Paschi's stock price has fallen 85% YTD and 99% since 2008, indicating its woes are priced in. Same for Banca Carige SpA and Unicredit SpA (other Italian banks). It takes big negative surprises to move markets significantly. Yet the following exhibits show markets aren't shocked to hear Monte dei Paschi and others are in hot water.

Exhibit 1: Monte Dei Paschi Plummets 99%

Source: FactSet, Banca Monte dei Paschi di Siena (BMPS) shares. 12/31/2008 - 12/20/2016.

Exhibit 2: Not Much Better Over Here

Source: FactSet, Unicredit SpA (UCG) & Banca Carige SpA (CRG) shares. 12/31/2008 - 12/20/2016.

Now, some might worry Italy's €20 billion of direct financial support entangles bank finances with sovereign, risking a "doom loop"-when a government threatens its own finances by buying banks' nonperforming loans, which in turn threatens other banks' viability based on their holdings of sovereign debt. There is precedent for this fear: Ireland's domestically administered bank bailout was a big reason its finances eventually faltered, requiring a €77 billion IMF/EU/ECB bailout in 2010. This is why the eurozone allowed Spain its non-bailout bailout-cleaner, less risk of problems spreading. And it is why the EU implemented bail-in rules for bondholders of failing banks. Both maneuvers are designed to sever the link between banks' health and sovereign finances. Yet Italy's response suggests this link isn't fully broken: While some investors will take losses under bail-ins, Italy is still recapitalizing its banks directly to avoid dinging Ma and Pa.

But before presuming Italy is about to enter a vicious cycle of snowballing bank and sovereign debt, let's scale a bit. The €20 billion thus far in guarantees (not outright transfers) is just 1.1% of Italy's 2015 GDP. In contrast, Ireland's 2010 bailouts sent deficits surging to €45 billion-32% of GDP. Over the subsequent two years, further bailouts drove the sum to €67 billion. But Italy's economy is vastly larger than Ireland's, and its bailout is much smaller. And even if Italy's banking troubles metastasized, the global economy wouldn't automatically falter. Italy is also just 2% of world GDP and less than 1% of global stocks. Italy-related fears aren't quite as intense today as they were in the past-but markets haven't fully moved on, either. The false fear of Italian banks knocking the wider eurozone economy is still kicking-and as always, false fears are bullish.

[i] Spain's non-profit banks, which were whacked in the crisis. Banking that isn't guided by profit and loss doesn't have a strong history of success behind it.

[ii]So called because it didn't aid the government repaying debt, but was instead used to aid banks directly. That, and because officials insisted it wasn't a bailout.

[iii] Who could forget Greece?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A May Global Economic Check-In2026-05-26

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 18 - May 222026-05-26

-

In The News How to think about the Iran war — and what it means for oil and stocks2026-05-25

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, US Q1 GDP, Graduation Season

2026-05-25

2026-05-25

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today