Personal Wealth Management / Market Analysis

The Good, The Basel and The Eurozone

Manufacturing, the Fed and a couple of PIIGS provided a mix of news for investors early this week—some good, some not-so-good and some simply political.

Global Manufacturing Update

The US, UK and eurozone reported manufacturing data this week, and surprising to many, almost all regions showed improvement.

The US ISM Index rose to 50.9 from 49 after a dip in May, beating expectations of 50.6. (Is it possible May’s dip was a blip?) A reading above 50 indicates expansion, while below 50 indicates contraction.

UK Manufacturing PMI rose to 52.2, a two-year high, from 51.5 in May—beating forecasts of 51.4. The survey shows all constituent categories improved across the board.

But perhaps the biggest surprise was eurozone manufacturing PMI. Contracting less than expected in June, the gauge of the 17 member nations increased to 48.8 (a 16 month high) from 48.3, beating estimates of 48.7. Notably, Italy’s, Spain’s and France’s indexes all rose. We’d posit the eurozone is not only improving, but improving in unexpected places, like its beleaguered periphery.

The US Moves One Step Closer to Basel III

The Fed voted unanimously to hike banks’ regulatory capital requirements Tuesday, moving the US closer to Basel III international capital standards—a move with plusses and minuses for Financials and broader markets. The rules aren’t yet set in stone—the FDIC and OCC will vote on them by July 9—but considering all three agencies co-wrote them, those votes are likely formalities.

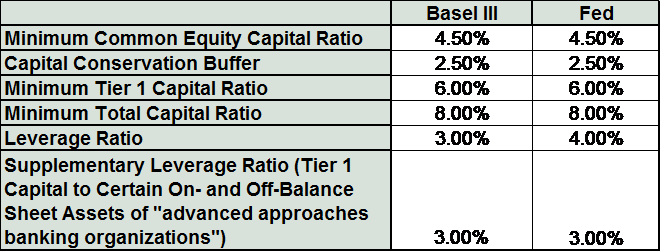

Among the plusses, the headline capital ratios largely match Basel III, as shown in Exhibit 1, and some of the differences include more flexible accounting rules for off-balance-sheet unrealized gains and losses. The higher leverage ratio is a negative, as it could weigh on bank lending—though according to the Fed, the 100 largest US banks have only a $4.5 billion capital shortfall, and they have until 2019 to raise it, which should help mitigate the impact. And, consistent with the Basel committee’s recent guidance on the Liquidity Coverage ratio, banks will be allowed to tap capital buffers during periods of financial stress without being treated as insolvent.

However, there may still be tougher rules to come. In his opening remarks, Fed Governor Daniel Tarullo said “a number of capital-related initiatives remain” for the US’s eight largest banks, including a higher leverage ratio and tougher capital requirements for banks relying heavily on wholesale funding. So regulatory uncertainty remains, as does the risk of large banks hoarding capital to meet higher requirements, which could hamstring lending—a headwind to economic growth.

The Fed claims these changes help limit systemic risk, though we’re skeptical. Making banks stronger is a perfectly benign goal, but there is no evidence stricter capital requirements for the biggest banks would have prevented 2008’s financial panic—regulators’ purported goal. “Too big to fail” wasn’t the problem in 2008. In fact, making huge banks even huger was regulators’ preferred solution to the crisis. That the solution is now considered a problem is puzzling—and the potential unintended consequences this introduces bear watching.

Exhibit 1: US and Basel III Capital Standards at a Glance

Source: Federal Reserve Board of Governors. “Advanced approaches banking organizations” includes institutions with consolidated total assets of $250 billion more or consolidated on-balance sheet foreign exposure of $10 billion or more.

Portu-Greece

In a surprise move on Monday, Portugal’s Finance Minister, Vitor Gaspar, resigned. Gaspar was the architect of Portugal’s recent bailout and is being blamed for ongoing economic weakness, which critics blame on “too much austerity.” And a day later, Portugal’s Foreign Affairs Minister (and a coalition leader), Paulo Portas, resigned, protesting the budget and Gaspar’s replacement, Maria Luis Albuquerque.

Prime Minister Pedro Passos Coehlo ensured he’d stay in office, yet fears persist these resignations could destabilize the Portuguese government—making it more difficult for the country to meet deficit reduction targets to receive much needed aid. But we largely doubt this happens. Portugal has come a long way since its 2011 bailout—its deficit has decreased by almost half since 2010. Challenges still remain, but Portuguese politicians have overall shown dedication to meeting targets. Further, the EU/IMF/ECB troika has repeatedly shown leniency toward bailout recipients.

Where it appears to be taking a (somewhat) harder line is Greece. Only ~2,600 state employees have been laid-off—far from the 4,000 required by yearend for Greece to receive its next €8.1bn aid tranche. Further, the country’s National Organisation for Healthcare Provision has already overspent by €1.2bn from January through May. Not exactly a campaign on cutting public spending. So Greece is being held accountable for its inaction, and if it can’t prove its ability to meet bailout terms, the IMF has threatened to stop contributing aid.

Timing isn’t great—Greece needs a tranche of aid to rollover €2.2bn of bonds maturing in August. Still, we don’t think this is eurozone-dissolution worthy. It could be the troika is talking tough with the eurozone’s perennial foot-dragger in the hopes Greece shapes up. Ultimately, we anticipate a last-minute compromise or can-kick or rule-bending to ensure Greece has the funding it needs.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today