Personal Wealth Management / Economics

The Great Unemployment Debate

Despite accelerating hiring, the unemployment rate incrementally rose in the last report before the US elections. But should we draw any material conclusions from the data?

Friday, the US Bureau of Labor Statistics (BLS) released October’s employment situation report—the last look at unemployment before Tuesday’s presidential election. As voters head to the polls, the unemployment rate will be 7.9%, 0.1 percentage point higher than a month ago, though down by around 1 percentage point in the last year. In the month, private employers added 184,000 jobs while government cut 12,000, for a net total of 172,000 jobs added (according to the Establishment survey). That’s a faster pace of hiring than logged last month.

Now, we realize writing that last sentence may raise the political ire of some. It seems this fall, no matter how dry the text or how much it’s simply a recitation of what a report showed, this statistic is clearly as politicized as they come outside of pure polling data and approval ratings. With each release, as much of the coverage surrounds the implications for candidates’ chances as what it might illustrate about the job market. Friday, for example, headlines suggested, “Job Growth Quickens, Giving Obama Some Relief.” Another discussed “Unemployment and Obama’s Election Prospects.”

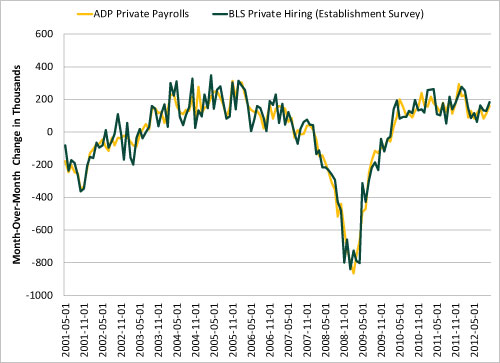

While the unemployment rate is undoubtedly a bit wonky, underlying government reports more or less echo what private sector-originated reports have shown—relatively consistent, though perhaps slow, improvements in the labor market for some time now. For example, earlier this week, ADP’s Employment report showed private employers added 158,000 jobs in October—a bit fewer than the BLS’s report showed, but not wildly so. Exhibit 1 shows these two indexes of private-sector hiring have moved in the same general direction and at similar magnitudes for some time.

Exhibit 1: ADP Private Payrolls and BLS Establishment Survey Private Payrolls

Sources: ADP, US Bureau of Labor Statistics, Federal Reserve Bank of St. Louis. May 2001 – October 2012.

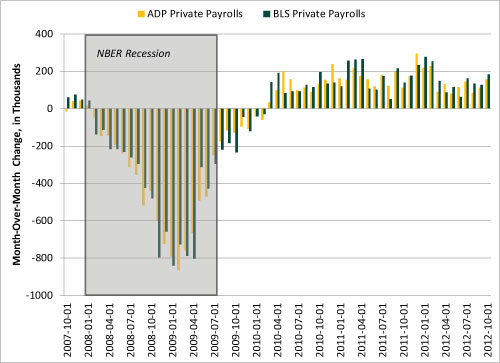

While the state of the job market tends to get a huge amount of ink, what seemingly gets less press is the fact the job market reflects economic conditions long since behind us. For example, the current bull market began in March 2009—a quarter or so before the current economic expansion began in June 2009 (according to the National Bureau of Economic Research, the official arbiter of US business-cycle dating). Yet according to both ADP and the BLS, the private sector didn’t add jobs until March 2010—well after both the recession ended and the bull market began. As Exhibit 2 shows, unemployment simply lags—as true today as it’s historically been.

Exhibit 2: ADP and BLS Data Show Hiring Lags

Sources: ADP, US Bureau of Labor Statistics, Federal Reserve Bank of St. Louis. October 2007 – October 2012.

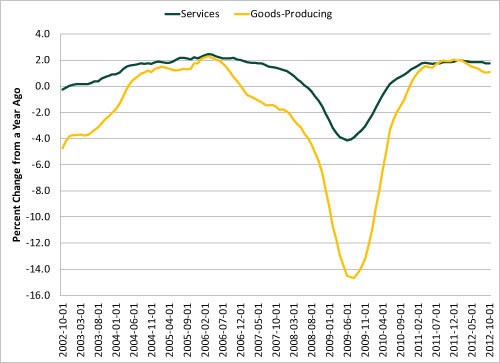

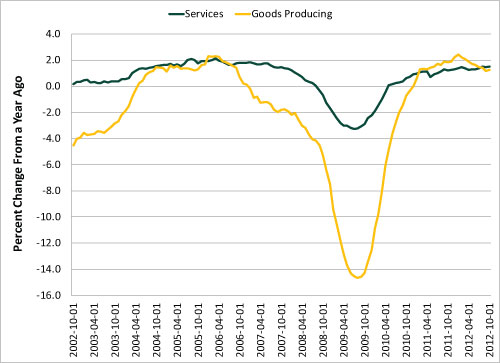

To figure out where hiring is going, then, we’d suggest not looking at the White House or even necessarily where hiring has been. Look instead to economic activity in the private sector—retail sales, factory output and, perhaps most importantly for jobs, services sector output. Services businesses account for a dominant share of US economic activity—which is mirrored by employment figures. Exhibits 3 and 4 show hiring data split between services and manufacturing firms. And in recent months, one can see a rotation where services have taken the lead in hiring.

Exhibit 3: ADP Payrolls, Services Vs. Goods Producing

Sources: ADP, Federal Reserve Bank of St. Louis. October 2002 – October 2012.

Exhibit 4: BLS Payrolls, Services Vs. Goods Producing.

Sources: BLS, Federal Reserve Bank of St. Louis. October 2002 – October 2012.

Economic activity in the private sector and, particularly, the services sector—and not who wins Tuesday’s election—is what will determine the pace of hiring moving forward. In that way, we’d suggest perhaps the focus on unemployment—and its political implications—is overstated.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today