Personal Wealth Management / Market Analysis

The Greek Gambit, Redux

Does Greek political turmoil mean the euro crisis has returned?

Those were two common sentiments in the press Tuesday in the wake of a broad selloff across the continent, with Greek political drama seemingly at the nexus. The Athex Composite (a capitalization-weighted gauge of 60 stocks listed on the Athens Exchange) closed the day down nearly -13%-that is not a typo; there is no missing decimal point. Many headlines shouted over what amounts to the index's biggest single down day since 1987, which is really saying something for Greece, considering the harrowing -91% (also not a typo) bear market in the Athex from October 31, 2007 through June 5, 2012. The big volatility seems to have stoked fears of a renewed eurozone crisis, with potential global implications. In our view, though, there is little evidence substantiating the fear.

For those who haven't paid close attention, here is the ultra-quick, bullet-pointed version of the euro crisis, which will admittedly gloss over a lot of details:

- In late 2009, then-Greek Prime Minister George Papandreou admitted the nation (errr ... the previous administration) had fudged its debt and deficit figures.

- 10-year sovereign Greek yields rose.

- By early May 2010, it was clear Greece was struggling to finance itself, with 10-year yields spiking to over 12%, up from 5-ish% when the year began.

- Greek yields rose.

- Greece got a €110 billion bailout from the EU, IMF and ECB (the troika)! Austerity.

- Greek yields fell.

- About a week later, the European Financial Stability Facility, a temporary, €750 billion bailout fund for troubled eurozone sovereigns was launched by the troika.

- Greek yields rose.

- The Greek fears became eurozone peripheral debt fears.

- Irish, Portuguese, Greek, Spanish and Italian yields rose.

- Ireland requested a bailout in late 2010.

- Yields rose.

- Portugal requested a bailout in April 2011.

- Yields rose.

- In early 2012, the EU created the European Stability Mechanism, a permanent bailout fund like the EFSF.

- Greece got a second bailout and defaulted.

- Yields fell.

- Greece defaulted.

- Yields fell.

- Yields kept falling for most of the last two years (brief bout with Cyprus' bailout aside).

- Economic growth returned to the eurozone in Q2 2013.

- Growth returned to Greece in Q2 2014.

Here are two other things you should know about this period: The global economy grew and despite some intense volatility at points, stocks overall rose.

That brings you (more or less) up to the present. The proximate cause for today's big fat Greek selloff[i] seems to be more Greek political theatrics, with PM Antonis Samaras moving up the Presidential election and naming Stavros Dimas his candidate for the figurehead post. Current Greek President Karolos Papoulias' term ends in March, and Parliament must name his successor by then at the latest. The election isn't a popular vote-it's held in Parliament, and Dimas will have three chances to win sufficient support.

According to Greece's constitution, in the first two votes, Dimas must win support from 200 of the 300 members of Parliament. In the third, 180. The first vote is slated for December 17, with further votes on December 22 and 29, if necessary. If all three votes fail to elect a president, Samaras would have to dissolve Parliament and call a snap election.

You might think this would be a rubber stamp, considering the Greek Presidency has little official power-that resides with the Prime Minister and Parliament, which has been controlled by Samaras and his New Democracy party since late June 2012. Samaras won a confidence vote as recently as October. But the vote is widely viewed in Greece as a confidence vote on Samaras' handling of bailout exit talks with the troika, which have been contentious lately. The leftist Syriza party has made their case clear-they believe Samaras bungled the bailout exit and want to reverse some austerity measures and subject bondholders to a third default. Needless to say, they oppose the current government, a coalition of New Democracy and the Panhellenic Socialist Party (Pasok).

Here is where the murkiness begins: The coalition holds only 155 votes, insufficient to elect Dimas President. The opposition, a disorganized group of Syriza, the Communist Party and the borderline neo-Nazi Golden Dawn, hold 99. The remaining 46 MPs are the key to the election, and it is unclear how much support the coalition count on. But however you do that math, the election seems extremely close. That raises the possibility of national elections, and Syriza leads recent national polls, which some fret would complicate negotiations with the troika, only two months before the bailout is set to expire.

Possible! But in our view, there are some major mitigating factors suggesting this isn't likely to send us back to bullet point #3. First, none of the financial matters involving Greece and the eurozone are new at this point. All are long known. While Tuesday's political wrangling in Greece was a surprise to Greek markets, it isn't unprecedented. Virtually no bailout review or negotiation has gone terribly smoothly between the parties, and the fear of Greece leaving the euro is so widely known (and, likely, overdone) it has its own portmanteau, the "Grexit."

But also, consider: Syriza isn't anti-euro, they're anti-austerity-a fairly common position in the eurozone these days. France's FranÇois Hollande, for one, was elected on an anti-austerity ticket, but he has since done a 180. We're not suggesting Syriza would do the same-just that we wouldn't presume the political platform of a party in Greece is any more ironclad than any other European party's. But it is possible this is merely politicians' promises, mostly lies in any language. Finally, they could mean what they say and simply seek better bailout terms from the troika. And, ultimately, if turmoil returns to Greece and Greece alone, that would be very unlikely to affect the global economy. Greece is small.

Now then, matters in Greece are not necessarily like those in Vegas[ii], but we'd caution against presuming they're contagious. After all, while fear of a pan-peripheral collapse was common from 2010 - 2013, the only nation to default was Greece. (Twice.) The only nation whose GDP fell by a third was Greece. The only nation to see its markets fall 90%? Greece. While it's true extremist parties have risen in the European Parliament, most voters in the EU pay less attention to this than national elections-it isn't a useful benchmark.

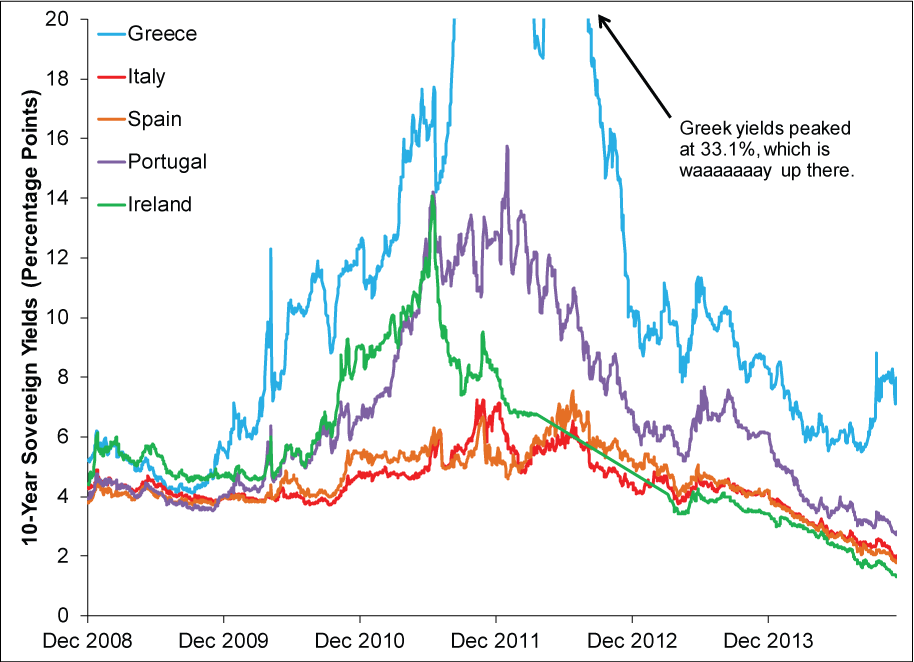

To date, as Exhibit 1 shows, the only nation who's seen a recent increase in rates? Greece, to 7.98% as of Tuesday's close.[iii] The rest of the periphery has yields below 2.81%, which is a far cry from the crisis.

Exhibit 1: Eurozone Peripheral Sovereign 10-Year Yields

Source: FactSet, 12/31/2008 - 12/09/2014.

In our view, this is a matter worth keeping an eyeball on, but we wouldn't suggest you lose much sleep over it. Greece has been sliding down a slippery slope for nearly all of this bull market, and we would suggest this is more in keeping with that norm than out of it.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Come on, you knew that was coming.

[ii] We're told what happens there, stays there.

[iii] Source: FactSet, as of 12/09/2014. 10-year sovereign bond yields for Greece, Italy, Spain, Portugal and Ireland.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today