Personal Wealth Management / Market Analysis

The High-Frequency Debate

Is the blame often heaped on high-frequency trading for stoking volatility proven beyond a reasonable doubt?

Machines skimming off pennies or less from millions and billions of transactions—turning slivers of bucks into mountains of money over time. That’s at the heart of Hollywood’s Superman 3and Office Space, but it’s also seemingly what many thinkof high-frequency trading (HFT)—computerized equity trading systems designed to execute in milliseconds. But is it so?

In attempting to prove their point, many HFT detractors cite volatility experienced in 2008, 2010’s “Flash Crash” and Wall Street’s recent spate of swings as evidence. Additionally, they often rely on estimates—like HFT accounts for 60%of all trading volume in stocks (how they accumulate that data is in question). But there are holes in this argument.

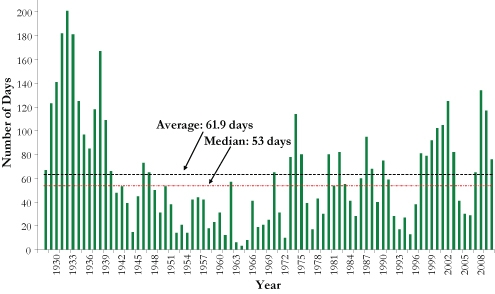

In attempting to prove HFT is solely driving heightened volatility, data showing HFT’s share of trading volume isn’t sufficient proof—in fact, it’s not even on target. Why? For one, selectively choosing points in the past three years yields an insufficient data set. After all, HFT wasn’t invented in 2008—it’s existed since the early 2000s. Also needed is a historical counterfactual—preferably, one predating HFT. And one including both up and down moves—after all, volatility isn’t unidirectional (though most blaming HFT for increasing volatility are really talking about negativity). Below is a chart depicting daily market movements exceeding 1% (up or down) since 1928.

Daily S&P Closing Change Exceeding +1% or -1%, 1928 – 2010

Source: Global Financial Data, Inc.

As shown, the average number of days of market volatility annually is about 62. The median is 53 days. Thus, the past few years have been higher. Case closed, right? Not so fast. Look at the preceding years: 2007 had 65, or roughly average. 2006? 29. 2005? 30. 2004? 41. HFT existed during all these far-less-volatile-than-average periods. Next look back at prior decades. What’s rather clear is there are periods—plenty of them—of above-average or median volatility in decades when traders executed via paper and shouting.

Next consider the theory these machines provide an unfair advantage, and thus, are skimming profits fractions of pennies at a time. Here again, the percentage of total volume executed via HFT is irrelevant. What would be relevant is the percentage of profitable HFT trades. And you’d need to know how many high-frequency trades have a high-frequency trader on the other side.

HFT machines are unlikely to be universally on the same side of a trade. After all, the users are in competition with one another. And ultimately, any position taken in stocks—even one lasting seconds—carries a risk of loss. That means a machine using mathematical calculations cannot be assured of making money—even a ha’penny.

HFT proponentsprincipally argue increased trading beneficially adds liquidity. And there is some sense to this. Think of appraisals, like those on Antiques Roadshow: Experts on the program commonly say something akin to, “These items frequently come up at auction and have sold in the range of X and Y.” (Excited or disappointed look from knick-knack owner follows.) Pure price discovery! That an item has come up for bidding many times before provides more reference points for assessing value. Similarly, more liquidity in markets aids price discovery since more bids provide a range to gauge changes in a stock’s perceived value—even if those bids come from computers. By no means are we arguing HFT is necessary for markets to efficiently operate. But we are arguing HFT’s detractors need to at least acknowledge proponents have a valid point.

Either way, it’s hard to prove HFT is a scourge or benefit beyond all reasonable doubt. But HFT critics’ blanket rage against the machines is far from a proven fact. HFT is mostly a new variation on what traders have always wanted—speedy, timely information to act on. Just consider why the stock ticker was invented—and why 19th century telegraph companies received special NYSE access to obtain quotes. Fear of machines and new technology isn’t a new societal feature and it seems to us the HFT debate is at the crossroads of this and investors’ dislike of sharply negative markets. Daily volatility has clearly been high lately, but the case HFT is to blame lacks evidentiary support in our view.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today