Personal Wealth Management / Market Analysis

The Joy of All-Time Highs

How we learned to stop worrying and love the acrophobia.

Acrophobia abounds. Rejoice in it.

The S&P 500 hit its 112th and 113th new all-time closing high of this bull market Wednesday and Thursday.[i]Cue the acrophobia[ii] and claims you'd be certifiable to buy stocks at these supposedly lofty levels. But there is nothing about an all-time high that says stocks can't get much, much loftier before a bear market begins. And perversely, that new all-time highs are greeted mostly by concerns-not celebration-is a sign these highs aren't the bull market's peak.

In a development that strikes us as pretty much the norm for the preceding 111, there was no shortage of fearful warnings that this all-time high-THIS!-signals the end is nigh. They point to Ukraine. Gaza.Iraq. The Fed and a supposedly more hawkish tone in meeting minutes released Wednesday-the Fed could hike rates sooner than the unknowable date pundits speculated was likely! Or certain investor sentiment surveys that allude to bullishness bubbling up, a contrarian warning sign, in their view. It's that eurozone's troubles are supposedly back, in the form of a deflationary depression. The US is still not growing at a lightning fast pace. Or it's Japan's falling GDP. Oddly, one of the most-read articles on a major financial news website rehashed fears from basically 2009, that the withdrawal of stimulus (monetary and/or fiscal) would yank the one supporting pillar from underneath the bull. Others presume the trouble is a distorted measure of valuations (the cyclically adjusted price-to-earnings ratio, or CAPE) has reached a level it last saw in July 2004, smack in the middle of the last bull market.

How, some pundits ask, can stocks rise amid so many fears?

But this actually gets markets somewhat backwards. Stocks rise, in part, because those fears exist. They act as fog, impairing investors' ability to see the world clearly. Gradually, as the fog lifts, investors see reality for what it is. Their confidence gradually grows with increasing clarity; they become more willing to bid more for each dollar of earnings. But you want to be invested before that happens to benefit. Today, the fog remains.

Consider: Thursday, while stocks were disregarding negatives, few noticed the news The Conference Board's US Leading Economic Index (LEI) rose 0.9% m/m in July, a fairly sizable monthly jump. In the postwar era, no US recession has begun when the LEI are rising, and no recession implies stocks won't face a stiff headwind from a faltering US economy. (Or global economy! UK, China and eurozone LEI are all positive as well.) Regional manufacturing gauges and the housing market show growth. Eurozone purchasing managers' indexes, while missing estimates, show growth in August. A strong Q2 earnings season has been largely downplayed as well, with some pundits suggesting earnings rose only due to buybacks[iii]-a faulty assertion when you consider aggregate S&P 500 profits rose, too.[iv]

The thing about bull markets is that throughout the course, one perceived negative is very often replaced by another-fears morph. Fed fears flip-flop between short-term rate hike and taper; inflation and deflation. Geopolitical concerns evolved from Arab Spring to Libya; Libya to Syria; Syria to Ukraine and Iraq. The CAPE has been above its average for all but four of this cycle's 66 months.[v] The fact folks haven't moved on from these fears today is telling.

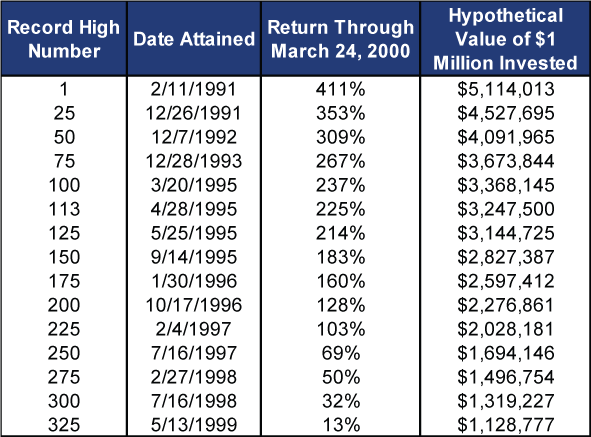

But still, is it worth the risk to invest with stocks having risen so strongly for five-plus years? In our view, the answer is yes. In the 1990s, the 113th record occurred April 28, 1995. Stocks rose 225% between that high and the ultimate one on March 24, 2000. This is not to say we are forecasting a 1990s repeat. But it does argue that discounting the ability of a maturing bull market to rise substantially as it ages may just be acrophobia.

Exhibit 1: Forward Return After Selected All-Time Highs, 1990s Bull Market

Source: FactSet, S&P 500 Total Return Index, 10/11/1990 - 03/24/2000.

[i] Source: Factset, as of 08/21/2014. S&P 500 Total Return daily closing index level, 03/09/2009 - 08/21/2014.

[ii] This is Greek for fear of heights. It is not agoraphobia, which is the fear of going outdoors, a far less common and far more extreme issue that we would struggle to apply to markets.

[iii] It is also an amazingly odd claim that buybacks are window dressing for profits. As a shareholder, the entire reason you buy a stock is you think you want a slice of that companies' future earnings. If a company buys shares back your stake in those future earnings increases, which is fundamentally bullish. From a market-wide point of view, it also reduces equity supply. So there.

[iv] Source: Factset. Data include the 478 S&P 500 firms reporting as of August 20, 2014.

[v] Source: Multpl.com, monthly S&P 500 CAPE. Average is 16.55.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today