Personal Wealth Management / Politics

The Latest in Catalonia’s Separatist Saga

What should investors make of Catalonia’s parliamentary election?

Last Thursday, Catalonia held the parliamentary election scheduled after Catalan separatists’ October independence referendum. With about 80% turnout, separatist parties have declared victory, and media are touting results as a massive victory for the pro-independence camp. But in reality, this is as status quo as it gets: The pro-independence parties actually lost two seats, and the outcome reinforces the divisions among Catalans over independence. While some political uncertainty still lingers and could act as a modest headwind, not much has fundamentally changed after the vote. In my view, this remains a localized issue, not one that should spell trouble for broader eurozone markets.

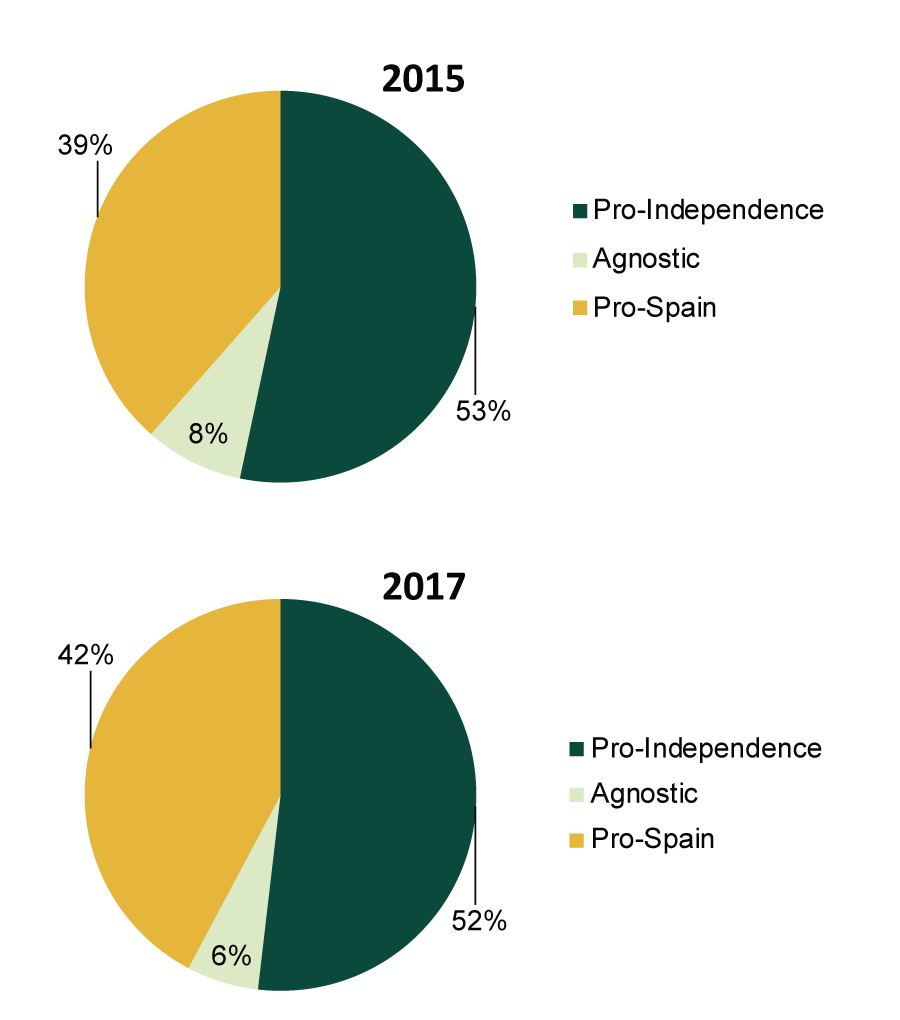

Here is a high-level view of Catalonia’s new parliament:

Exhibit 1: Meet Catalonia’s New Parliament, Same as the Old Parliament?

Source: Fisher Investments Research.

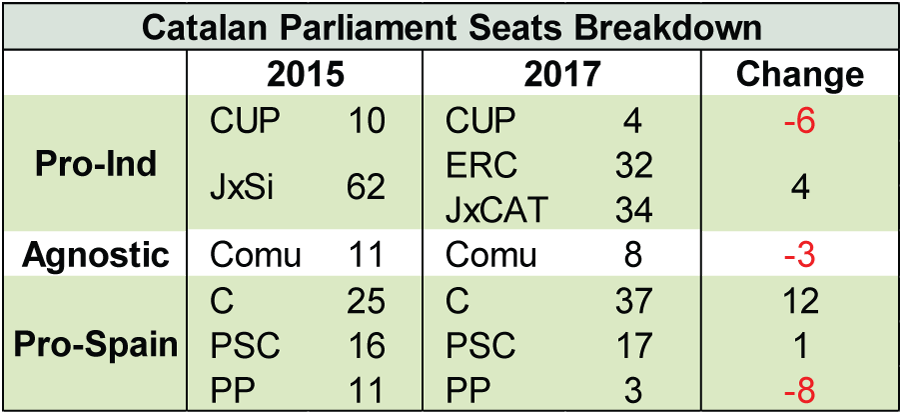

Exhibit 2: Detailed Results by Party

Source: El País, Fisher Investments Research. CUP is Popular Unity Candidacy-Constituent Call; JxSi is Junts pel Sí (Together for Yes); Comu is Catalunya en Comú-Podem (Catalonia in Common—We Can); C is Ciudadanos; PSC is Socialists’ Party of Catalonia; PP is People’s Party of Catalonia; ERC is Republican Left of Catalonia—Catalonia Yes; JxCAT is Junts per Catalunya (Together for Catalonia).

While the pro-independence side maintained its majority, parties within the camp disagree over important details. The Republican Left, formerly the primary independence party in Catalonia, won about the same amount of votes as JuntsXCat—a new party led by former Catalan leader Carles Puigdemont (currently in exile in Brussels). These two parties aren’t as extreme as Popular Unity, which desires to nationalize all major industry in Catalonia. The pro-Spain side isn’t any more unified, either: business-friendly Ciudadanos, the center-right People’s Party and the center-left Socialist Party span the political spectrum and are largely ideologically incompatible, making any coalition-building difficult.

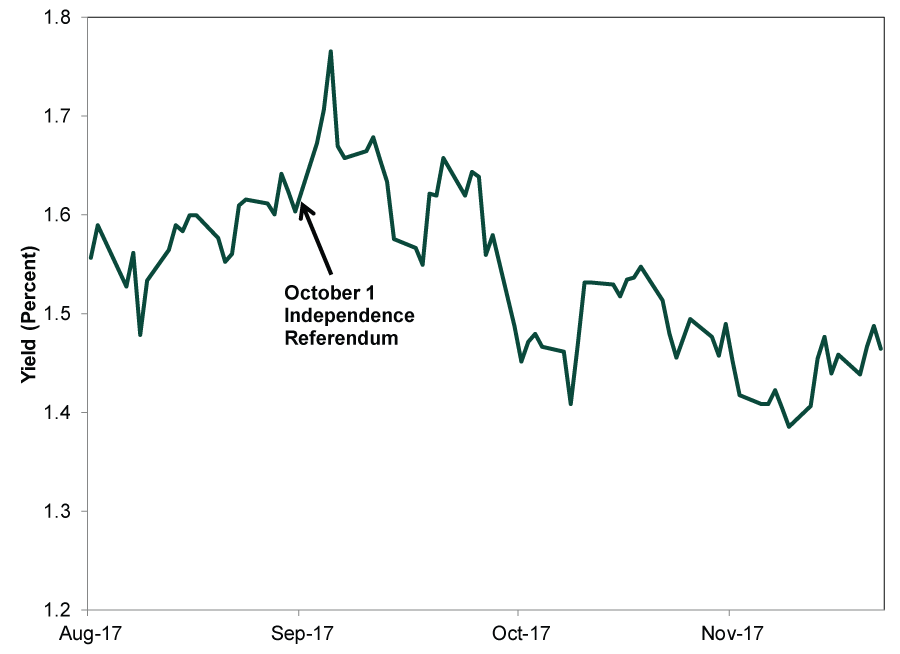

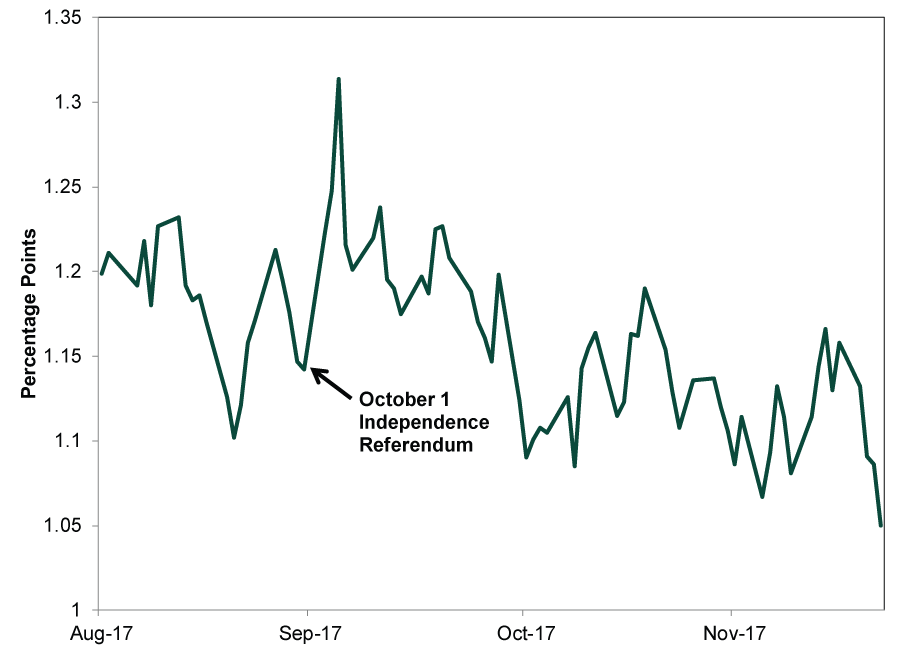

Despite investors’ fears, Spanish markets have remained fairly calm throughout the political standoff that followed the October 1 referendum. Spanish 10-year bond yields are down since that vote (Exhibit 3), as is the spread over German bunds (Exhibit 4), a measure of relative risk.

Exhibit 3: Spanish 10-Year Yield

Source: FactSet, as of 12/22/2017. From 8/31/2017 – 12/22/2017.

Exhibit 4: Spanish-German 10-Year Bond Yield Spread

Source: FactSet, as of 12/22/2017. From 8/31/2017 – 12/22/2017.

Spanish stocks, though choppy, have largely moved sideways—no steep pullbacks. Though they have lagged broader eurozone markets, evidence of uncertainty generating headwinds, investors have largely taken the developments in stride. Always remember: Markets are very good at weighing the likely future and pricing in risks. If the Catalonian situation posed grave risks to Spain’s economy, the market would tell us.

While it seems unlikely this situation gets resolved soon, fears about the potential broader fallout seem overwrought, in my view. The Catalan saga remains a localized legal issue. While continued uncertainty could be a minor headwind in the short term, it also doesn’t fundamentally alter the positive drivers underlying the Spanish economy—let alone the eurozone.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today