Personal Wealth Management /

The Many Faces of Risk, Retirement Edition

Contrary to what many believe, risk has a much broader meaning than merely risk of loss.

Risk. To some, the four-letter word of investing. And to many investors, it means effectively one thing: potential loss of principal. But in reality, risk has a far broader definition-and realistically, you cannot avoid it. You can only exchange one form for another. Commonly, folks shun potential loss of principal or short-term volatility by reducing equity holdings or other higher returning assets in favor of less volatile, lower returning ones. And yes, in doing so, you are likely subjecting yourself to less volatility. But at the same time, risk hasn't been averted. You may have greatly increased a hard-to-see, yet insidious risk: Longevity risk, or the risk you last longer than your money.

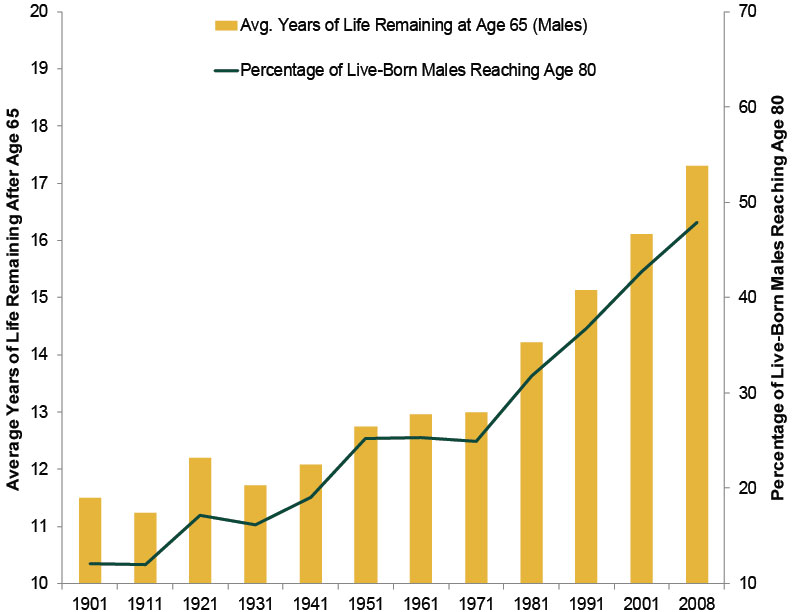

It's no secret Americans are living longer and longer lives. On average, a baby boy born in America today will live to be over 78 years old-an increase of more than 27 years in the last century. As medicine, hygiene and overall living standards have increased in the US, so has life expectancy-and the share of Americans reaching what many consider to be advanced age. In Exhibit 1, the yellow columns plot the life expectancy of a 65-year old male American. The green line shows the percentage of live-born American men who live to age 80. As of the most recent data (2008), nearly 50% of men lived to 80. In 1971, only one in four did so.

Exhibit 1: Expanding Male Life Expectancy and Frequency of Reaching Age 80

Source: Centers for Disease Control.

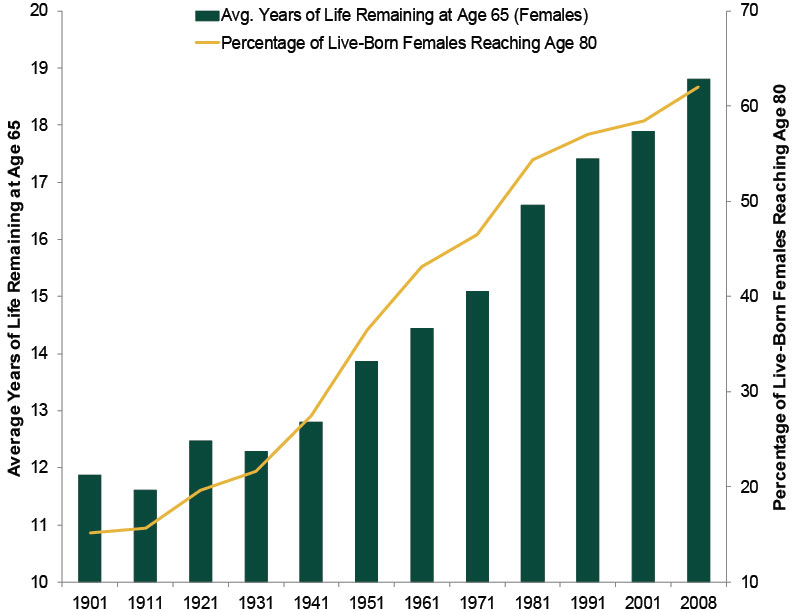

Women tend to live even longer than men. The average American woman can expect to live almost 19 years after reaching age 65. Six in ten reach age 80. Barring extenuating circumstances like an illness, an American woman is more likely than not to reach 80. (Exhibit 2)

Exhibit 2: Expanding Female Life Expectancy and Frequency of Reaching Age 80

Source: Centers for Disease Control.

To take it a step further, consider the rising number of nonagenarians. As of 2008, 16% of men and 27% of women lived to age 90-up from 7.7% and 14.1% in 1971, respectively. Astoundingly, the number of men reaching 90 almost doubled between 1991 and 2008. The typical American retiree must plan for a far longer period than his or her parents.[i]

These longer spans require thinking even more about your changing cost of living today. Assuming you live at least partially off of your retirement savings, it's prudent to consider you'll need the money to last longer and outpace inflation. But even considering average inflation may not be telling. Inflation generally doesn't tell a very useful story as it pertains to your finances-there are many components in the Consumer Price Index basket (CPI, a common inflation measure). Unless your expenditures align perfectly with the exact goods specified in the exact weights used, CPI inflation will not directly reflect changes in your cost of living. No statistic can capture that perfectly, because your spending patterns are unique to you and likely shift throughout life. Consider: One 50-year old single man living alone will have totally different cost inputs than a 50-year old man with a college-age child he's paying tuition for. But when his child graduates college, the second man's expenses will likely be radically altered.

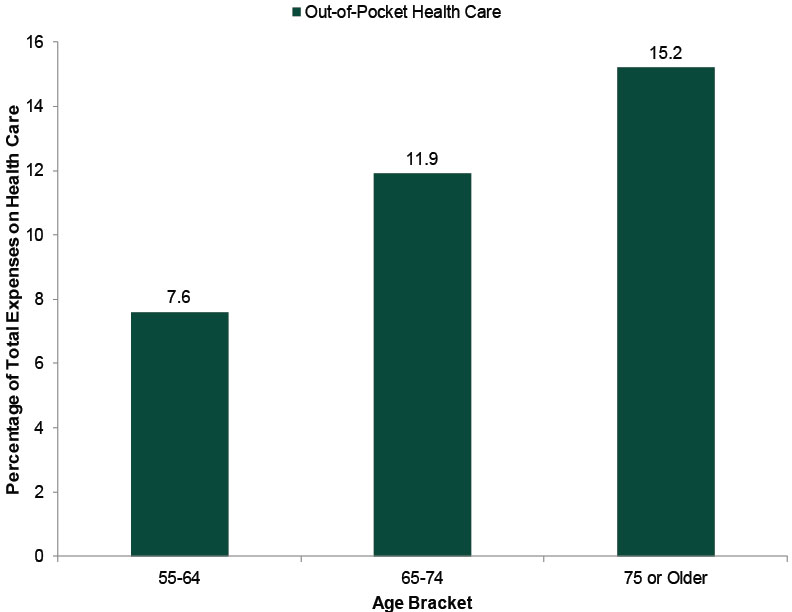

It's no secret a major influence on retiree budgets is health care. As we age, we tend to consume more and more health care services, devices and drugs. This doesn't stop at retirement-it accelerates. Exhibit 3 plots the change in the share of expenditures by Americans across three age brackets typical of retirees and those approaching retirement. It isn't just that health care costs are fast rising relative to prices generally-health care consumption also increases dramatically in retirement.

Exhibit 3: Out-of-Pocket Health Care Expenses' Share of Total Expenses Doubles With Age

Source: Social Security Administration, Expenditures of the Aged Chartbook, 2010.

To put a number to it, according to the Bureau of Labor Statistics (BLS), medical care expenses have increased at a nearly 5% average annual clip since 1984. At that rate, $10,000 spent on medical care roughly doubles in 15 years-easily within the average 65-year old's life expectancy.

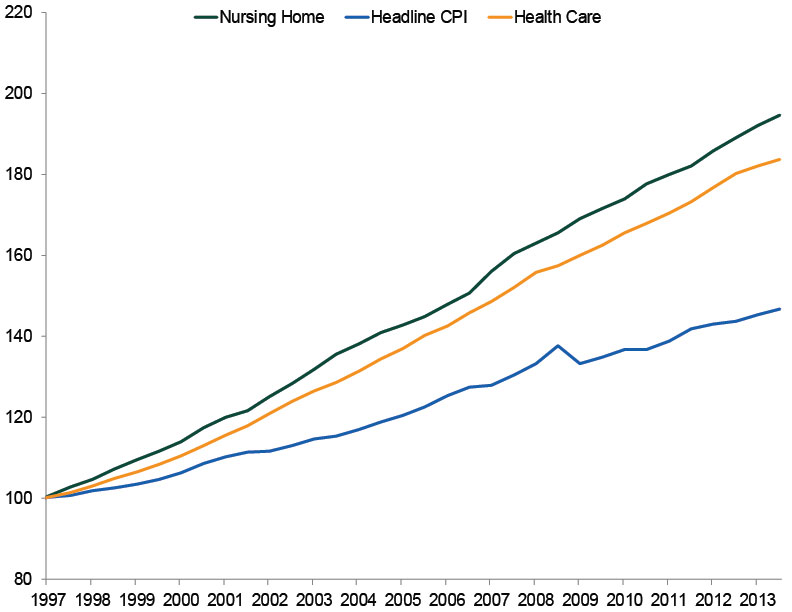

With more and more Americans living longer, nursing and retirement homes are becoming increasingly common expenses-sort of a hybrid expense between health care and housing. Since the BLS began tracking nursing homes separately in 1997, prices have risen at an even faster clip than health care. (Exhibit 4)

Exhibit 4: Nursing Home Costs Rising Faster Than Health Care and Much Faster Than CPI

Source: Bureau of Labor Statistics, December 1996 - November 2013. All costs indexed to 100 at December 1996.

These factors are not insurmountable but they do call into question "conventional wisdom" like age-based asset allocation. Subtracting your age from 100 or 120 to determine the percentage of stocks to include in your mix of stocks, bonds and cash is of little value when more folks are living longer than ever. (And life expectancies likely continue advancing in the future.) You may need stocks' long-term returns to support your lifestyle! The notion of risk you consider must be more broad than simply volatility or the risk of loss. Ask yourself: Is it more risky to invest in stocks, an asset class that has historically risen in roughly 70% of years since 1926, or bet that neither you nor your spouse will live to a ripe old age?ii Which is more fear-inducing: short-term volatility or a long-term future with questionable financial backing?

It is important to understand the trade-off involved with reducing a portfolio's short-term volatility. Often, such moves increase other, less obvious or immediately visible risks. The painful part of it is by the time longevity risk becomes more clear, it may be too late to repair.

4 Ways to Avoid Running Out of Money During Retirement

To investors who want to retire comfortably. Download the guide by Forbes columnist and money manager Ken Fisher's firm. It's called "The 15-Minute Retirement Plan." Even if you have something else in place right now, it still makes sense to request your guide! Click Here to Download!

[i]Centers for Disease Control, National Vital Statistics Reports, Vol. 161, No. 3, September 24, 2012; page 48, table 20.

[ii] Global Financial Data, Inc., as of 07/26/2013. Figure references S&P 500 Total Returns for calendar years 1926 - 2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today