Personal Wealth Management / Behavioral Finance

The Missing Lesson: Unfriend the Trend

Beware forecasts that simply extrapolate the year's start forward.

Thursday's personal finance pages were awash with pundits sharing investing lessons learned (with varying degrees of value). The Wall Street Journal's Morgan Housel offered up four mostly sensible points. The Motley Fool's Sean Williams offered 21 occasionally overlapping points that have some real pearls of wisdom. Best of all, US News and World Report's Catherine Alford offered "12 Money Lessons Your Child Should Know Before Age 12." (This latter article included the most basic-yet-overlooked lesson of all-the power of compound interest. Many folks older than age 12 could benefit from learning to love compounding.) However, might we suggest a timely 38th lesson? Recent trends do not predict the future. That is a lesson it seems to us many investors-including some professional prognosticators-should probably consider.

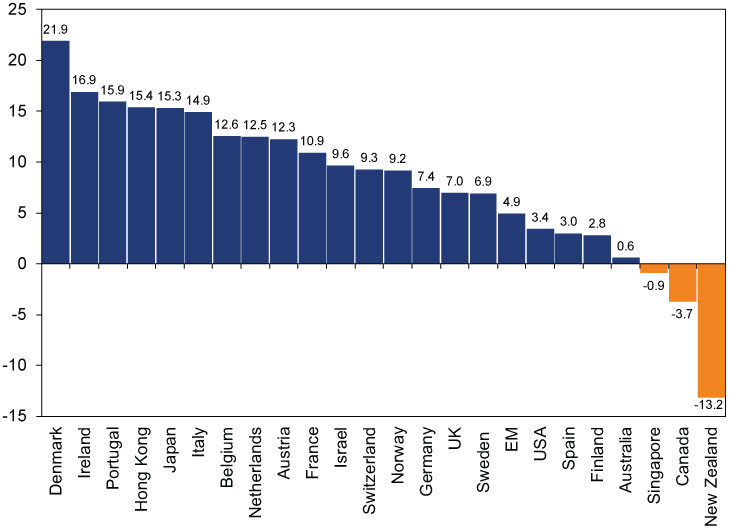

Next week, 2015 will reach the halfway mark and, as is customary, Wall Street forecasters are already unveiling their second-half outlooks. Thus far in 2015, US stocks (the S&P 500) have returned a paltry 3.4% including dividends (2.4% without). Global stocks have fared better, rising 5.6% (with net dividends), led by Europe and Japan.

Exhibit 1: Year-to-Date Global Stock Market Returns by Country/Region, in Percentage Points

Source: FactSet, as of 6/25/2015. MSCI World constituent country returns (in USD) and MSCI Emerging Markets returns including net dividends. USA is represented by the S&P 500 and includes gross dividends.

On the rates side, benchmark US 10-year Treasury yields started the year by falling from 2.17% to a low of 1.64%, but later U-turned to close Thursday at 2.37%. Those are the trends, friends, as Q2 comes to a close. And it is against this backdrop that Wall Street's strategists are recalibrating their outlooks for the remainder of the year.

As a refresher, many pundits entered 2015 expecting some pretty darn tepid returns from stocks-US and foreign, for that matter. In January, the 10 forecasters included in Barron's semi-annual Roundtable forecast an average 5% gain for US stocks.[i] They expected little more from foreign. The most bullish forecaster in January projected the S&P 500 would rise 8 - 10% this year.

And he is sticking to his guns! As are most of the analysts polled. Two Goldman Sachs strategists (Abby Joseph Cohen and David Kostin) now project the S&P 500 will finish the year at 2200 and 2150 respectively, or gains of 4.6% and 2.2% from Thursday's 2103.2 close. Another firm out with its second half outlook is projecting US stocks will "oscillate around the 2100 level" and finish the year flattish, which is basically a recap as much as it is an outlook. CNN surveyed 20 investing professionals and the results showed they anticipate the S&P 500 finishing 2015 at 2183. That's a 3% gain from present levels, or a repeat.

Many of these same surveys and outlooks argue better returns await in Japanese and European stocks, which, if you refer back to Exhibit 1, looks a lot like what just happened. Still others are extrapolating the 20 basis point (0.2 percentage point) gain in 10-year yields to suggest yields continue rising from here-some even going so far as to predict a bond bear based on the quick rise starting in April continuing.

However, there isn't anything about the first half of a year that predicts the second. In any market. Let's examine some S&P 500 history for an example. In 2009, the first half was incredibly volatile and tallied only a 3.2% gain.[ii] That had analysts projecting a rocky second half at best. Yet after June, US stocks had a relatively smooth ride to 21.3% gains.[iii] 2010's first half closed amid a correction that drove the gauge to a -7.6% decline.[iv] A decline ending days into Q3, with stocks rising 22.0% in the second half.[v] 2011's first-half gain didn't foretell the second half's decline, and 2012's 8.3% first half was followed by a 4.7% second.[vi] 2013 and 2014 did largely continue trends from the first half into the second. But this is far from a consistent trend.

Further back in time, 1929's returns through June were a nicely positive 13.4%.[vii] Anyone need us to point out the second half didn't follow suit? In 1932, the first half was awful, with the S&P 500 falling -45.4%, but the second half was great! Stocks rose 55.5%.[viii] 1933 reversed that pattern, with stocks rising huge (+58.4% in the first half) but faltering slightly (-7.4%) in the second.[ix]

More recently, in the 2000s bull, 2003's solid first half was followed by a similarly strong second. But 2004, 2005, and 2006 all saw much stronger second halves than first. 2007 reversed that, with the first half's gain giving way to second-half losses. During the 1980s, stocks' first-half direction (up or down) matched the second half's only five times. In the 1990s, direction matched more frequently (seven of ten years), but the average difference in return between the first and second half was big! Nearly six percentage points. This isn't a basis for setting expectations.

In our view, your outlook for the remainder of 2015 shouldn't be influenced by returns thus far. As we often write here, past returns don't predict the future. Or, in Facebook English, unfriend the trend.

[i] While we are big fans of Barron's Roundtable, we feel compelled to point out that in virtually every edition in this bull market, the introduction claims "stock picking is the best path to profit" given the current backdrop. Which is a fallacy of the highest order, considering stock picking is typically the least important part of portfolio strategy.

[ii] Source: Factset, as of 6/25/2015. S&P 500 price returns.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] Ibid.

[viii] Whew. Ibid.

[ix] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today