Personal Wealth Management / Market Analysis

The Myth of Small Cap’s Superiority

Small cap’s historical long-term returns don’t tell the full story.

It’s perhaps stocks’ worst-kept secret: Small cap has outperformed large cap since 1926. Over the years, all sorts of theories have emerged to explain the category’s apparent perma-superiority, rationalizing a blind buy-and-hold approach or bias against large cap. Some say small caps are just plain riskier, justifying higher upside. Others say smaller firms have more growth potential—it’s a lot easier for prices and earnings to grow exponentially off a low base than a Google-sized one. Neither is correct. Small cap isn’t any better! It leads at times and lags at others, and its outperformance is concentrated in bull markets’ initial bounces off bear market lows.

From 1926 through 2013, small cap has returned about 11.5% annualized. Large cap, represented by the S&P 500, has annualized about 10%. However, take out the first two years of the four biggest small cap post-bear booms (of the completed bull markets during that span)—beginning in 1932, 1942, 1974 and 2002—and average annualized returns dwindle to 7.6% for small cap and 7.9% for large.

Small cap’s returns are largely a function of the market cycle. Small firms usually get hammered in bear markets and cut costs to the bone in order to survive. This gives them an easy base for earnings growth when the bull begins—even modest revenue recovery brings big earnings pop. That plus a reversal of the extremely dour pessimism surrounding small caps in the bear market’s final throes—when folks fear small firms’ very survival—gives the category a big tailwind during the bull’s early goings.

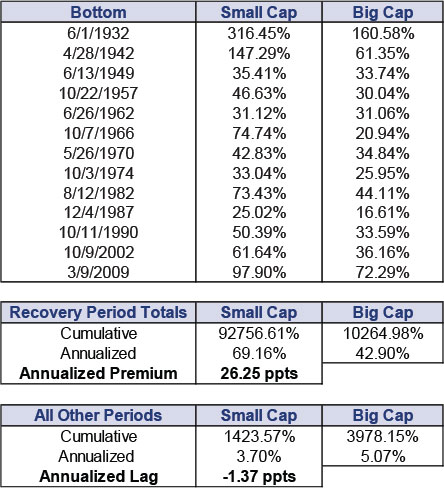

This phenomenon is short-lived, however. Exhibit 1 shows small cap’s and large cap’s returns during the first year of every new bull market since 1926. During those 13 years, small cap’s annualized return is 26.25 percentage points ahead of large cap. The rest of the time, small cap’s annualized return is nearly 1.4 percentage points behind large cap.

Exhibit 1: Small and Large Cap During a Bull’s First Year ... and the Rest of the Time

Sources: Morningstar, FactSet and Global Financial Data, Inc., as of 6/2/2014. Small cap returns are based on the Ibbotson Associates Small Stock Total Return Index from 1/1/1926-12/31/1978 (Morningstar) and the Russell 2000 from 1/1/1979-12/31/2013 (FactSet). Big cap returns are based on Global Financial Data’s S&P 500 Total Return Index from 1/1/1926-12/31/2013. Monthly data are used through 12/31/1987; daily data are used thereafter. For periods beginning prior to 12/31/1987, first-year returns are computed from the end of the month.

Sometimes small cap’s outperformance stretches well beyond the first year, sometimes it fizzles early—this isn’t a timing tool. It’s more to illustrate a critical point: To get small cap’s great long-term returns, you must be buying at the depths of some big, nasty bear markets—right when fear is highest, exactly when instinct and emotion tell you to sell. And when many investors cave.

Instead of pinning all their hopes on small cap solely because of its higher long-term return, investors are likely better off over time staying open to the opportunities (and risks) arising in all major categories—small, big, growth, value, foreign, domestic, dividend payers and non-payers and all the different countries and sectors. Leadership rotates often and irregularly, and the shifts happen for gameable, fundamental reasons. That includes shifts to large cap, which usually outperform in maturing bulls—with the biggest of the big stocks (“mega caps,” or those with a market cap above the MSCI World’s weighted-average market cap) doing best as the bull wears on.

In our view, that’s about where we are today. With the deep pessimism of the bull’s early stages waning and optimism becoming more prevalent, retail investors who sold out during the bear’s depths are trickling back into stocks. These investors, naturally more skittish, are more inclined to bid up the biggest, most stable companies—those with bigger gross margins, multiple product lines, strong brand names and geographically diverse revenue sources, all drivers of continued earnings growth and stability. This phenomenon should put mega cap stocks in the driver’s seat through the end of this bull market, disappointing those who cling blindly to small cap solely because of one long-term number.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today