Personal Wealth Management /

The Myth of the Monetary Airbag

Is loose monetary policy protecting stocks from reality?

Janet Yellen is a powerful lady, but she isn't the reason stocks are rising while people are fighting in Iraq and Ukraine. Photo by Chip Somodevilla/Getty Images.

Are central banks protecting markets from reality? Some argue yes, with loose monetary policy an airbag against a geopolitical-tension driven crash. Yet market history argues otherwise: Regional conflicts regularly have fleeting market impact, whatever the monetary policy may be at the time.

The concern is understandable, considering 2014's events thus far. Ukraine has descended into war, with "pro-Russian" separatists going so far as to shoot down Malaysia Airlines Flight MH 17. The terrorist group Islamic State of Iraq and al-Sham ignited war in Iraq, tearing through the country's northwest in June. Violence between Israel and Hamas has escalated. In the past several months, Russia annexed the Crimea, the Thai military staged a coup d'état, and a Chinese vessel sank a Vietnamese fisherman's boat in the South China Sea leading to a water gun fight on a naval scale. Not to mention continuing past stories, like the Syrian War and hot rhetoric in East Asia from China, Japan and North Korea blowing some more fish to smithereens with a missile test. Yet for the year, global markets are up 6.3%.[i]

Many folks may wonder, "Why are markets so blasé toward these events? Are they-gasp-unaware? Do markets not correctly see the severity of war?" Of course they do! But they also know regional tensions and violence don't grind the global economy to a screeching halt. In most of the world, normal life goes on. Maybe folks are more concerned and monitor the news closer. But the economy doesn't stop. In this five-year old bull market alone, tensions have flared from Egypt and Syria to Tunisia and Sudan, along with plenty of threats for more-yet stocks continue running higher.

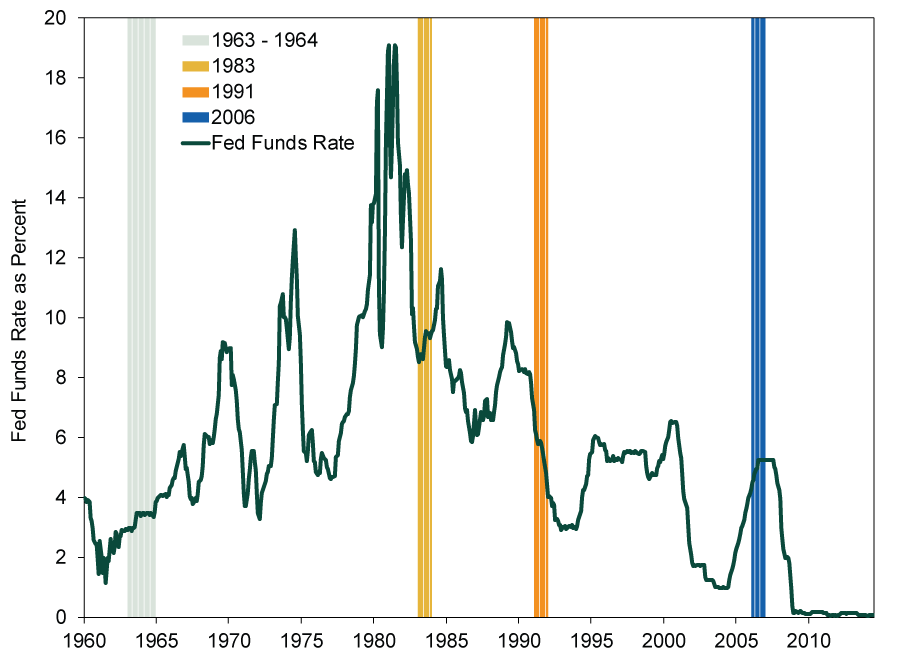

This isn't a recent phenomenon. Here is an uncommon perspective you will not read from many market pundits: History doesn't support the notion conflict is automatically bad for stocks. In fact, there are myriad examples of bull markets rising while tensions and conflict do, too. Consider 1963 - 1964: JFK was assassinated, South Vietnam and Brazil saw their governments overthrown and Soviet dictator Nikita Khrushchev was deposed. Yet global markets rose 15.4% and 11.3%, respectively.[ii] In 1983, the USSR shot down KAL Flight 007, Lebanese militants bombed a US marines' barracks and the US invaded Grenada-yet markets still rose nearly 22%.[iii] They rose 18.3% in 1991, despite Operation Desert Storm and an Irish terrorist attack on 10 Downing Street in the UK.[iv]In 2006, North Korea tested nuclear weapons, Israel and Hezbollah battled over the summer and Thailand experienced another coup, yet markets surged 20.1%.[v] It takes a global conflict with a reach like World War II-one big enough to wipe trillions off of global output-to cause a bear market.

Now, maybe you're wondering if monetary policy was loose at those points, preventing a crash like pundits argue it is today. Here is your answer: No. Historically, most folks equate loose and tight descriptors with US overnight rates. Low and getting lower is loose, higher and rising is tighter. Exhibit 1 highlights our four examples: Rates were rising during three. The Fed Funds rate today is at 0.1%-suffice it to say it was higher in our examples. Higher and rising rates didn't make stocks more prone to regional conflict. This guts the idea stocks need a monetary airbag during conflict. This same argument also goes against those who argue quantitative easing (QE) is propping up stocks today-the US didn't use QE until 2008, yet markets weathered regional war just fine without it.

Exhibit 1: Effective Federal Funds Rate (Monthly) Since 1960

Source: St. Louis Federal Reserve, as of 07/30/2014.

Now, to be clear: We aren't arguing war is bullish. It isn't. It's just that skirmishes, armed conflict and outright regional war are unlikely to carry the power to negate what private companies are doing-and the profits they're making-in the US, UK and other countries around the world. As scary and troubling as wars are from a humanitarian point of view, regional strife tends to be a false fear for global markets.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Source: FactSet, MSCI World Total Return from 12/31/2013 - 7/29/2013.

[ii] Source: Global Financial Data, FactSet as of 12/31/2013.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

In The News Expert says investors are ignoring a massive global rally2026-06-22

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today