Personal Wealth Management / Market Analysis

The Next Debt Fear?

A few Fed officials fretted Corporate America's debt at September's meeting, which has some media types wondering if we all should be worried.

Photo by DNY59/iStockPhoto.

Debt. It is a four-letter word to many investors, both literally and figuratively.[i] Consider that in the eight years since the financial panic struck, we've seen a rotation of fears over various flavors of debt: Alt-A mortgages and commercial mortgages were each widely feared to be the "second shoe to drop" in 2009 (though the first shoe was actually not debt as much as an accounting policy change). Later it was Dubai World. Then Greek debt, which was followed, briefly, by municipal debt. Then debt fear spanned the eurozone. In recent years, it has been mostly high-yield and Energy-sector debt. But now, judging from recent Fed meeting minutes, we figure the next debt fear may just be corporate debt. Folks, let us pre-emptively gut this for you: Corporate America isn't overindebted presently.

The Fed's September meeting minutes include the claim that: "A few participants expressed concern that the protracted period of very low interest rates might be encouraging excessive borrowing and increased leverage in the nonfinancial corporate sector." Which is a sentence the media didn't miss, with some arguing the fact more investors haven't caught on to this next big debt fear shows complacency abounds.

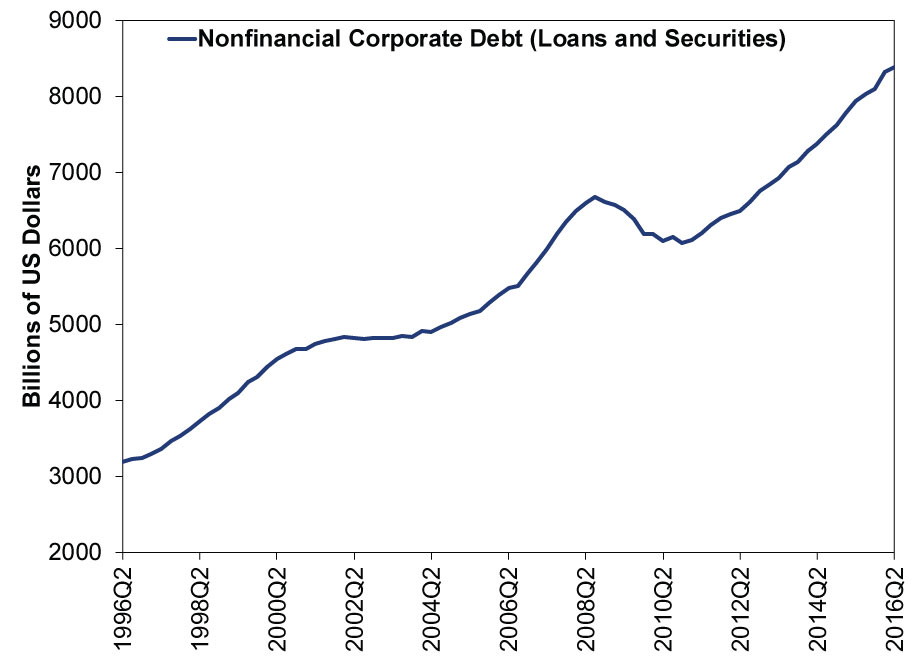

It's true nonfinancial corporate debt has risen in recent years. (Exhibit 1)

Exhibit 1: US Corporate Debt Keeps Growing

Source: US Federal Reserve, as of 10/31/2016. Nonfinancial corporate debt, quarterly, in trillions of dollars, Q2 1996 - Q2 2016.

And there is undoubtedly some truth to the assertion exceedingly low borrowing rates partly fueled this rise. After all, interest rates are just the cost of money, and when it's low, it wouldn't be surprising for folks to take advantage. Mostly it's good financial sense: If you can borrow for X and earn Y over the long-term, Y-X is your profit margin. This math has fueled stock buybacks, but also corporate investment. In recent decades, there has never been a better time to borrow funds for a new plant, product line or equipment. It doesn't take much return on that investment for borrowing to be profitable. But absolute debt levels won't tell you anything by themselves-as always, scaling is necessary.

By scaling, we mean proper scaling. Some seized upon the Fed's words, and argued corporate debt is very high as a percent of US GDP. But this mixes apples and oranges. The relationship between the level of private businesses' debt and the flow of economic activity across the entire US-households, businesses and government-is tenuous at best. It seems like an extension of the common practice of comparing federal government debt to GDP. That makes much more sense, though, as government tax revenues (which support interest payments) are generally based on overall economic activity in the country, which GDP is a loose way to tabulate.[ii]

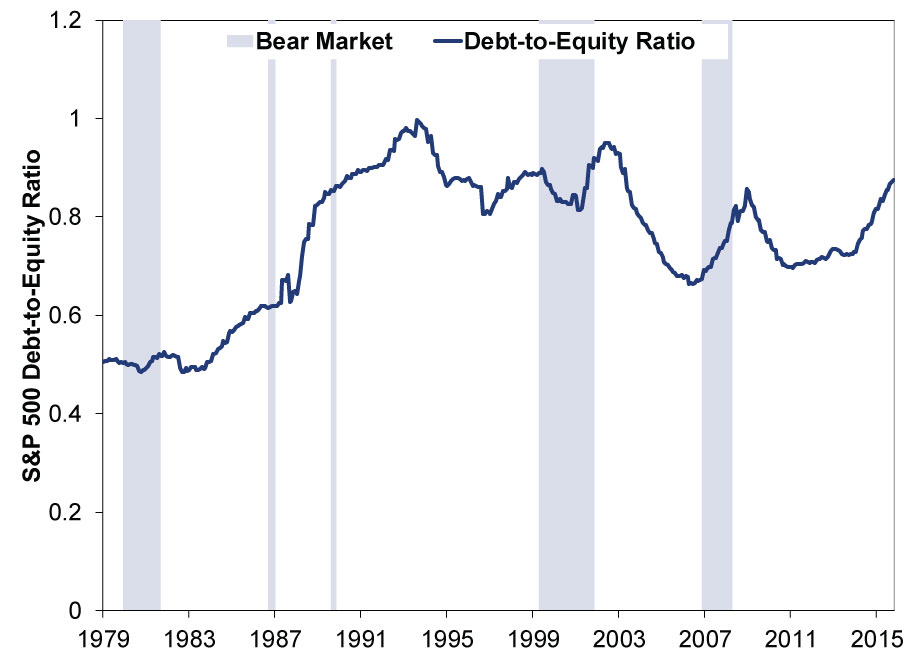

But that doesn't hold for business revenues or profits. GDP's calculation quirks destroy this comparison. For one, Corporate America books costs and revenue from all over the world. US GDP makes no effort to tabulate that, and actually has calculations that make this even less comparable. After all, there is a little store chain whose name rhymes with Mall Start that sells many, many imported goods. Those imports buoy Mall Start's revenue and profits-increasing its ability to service debt. But they lower GDP. For nonfinancial corporations, it's better to compare total debt to total equity to assess balance sheet strength. Presently, this metric suggests Corporate America isn't so hugely over-indebted. (Exhibit 2)

Exhibit 2: Debt-to-Equity Ratios Aren't Alarming

Source: Thomson QAI, as of 9/30/2016. S&P 500 ex. Financials total debt/total equity, December 1979 - September 2016.

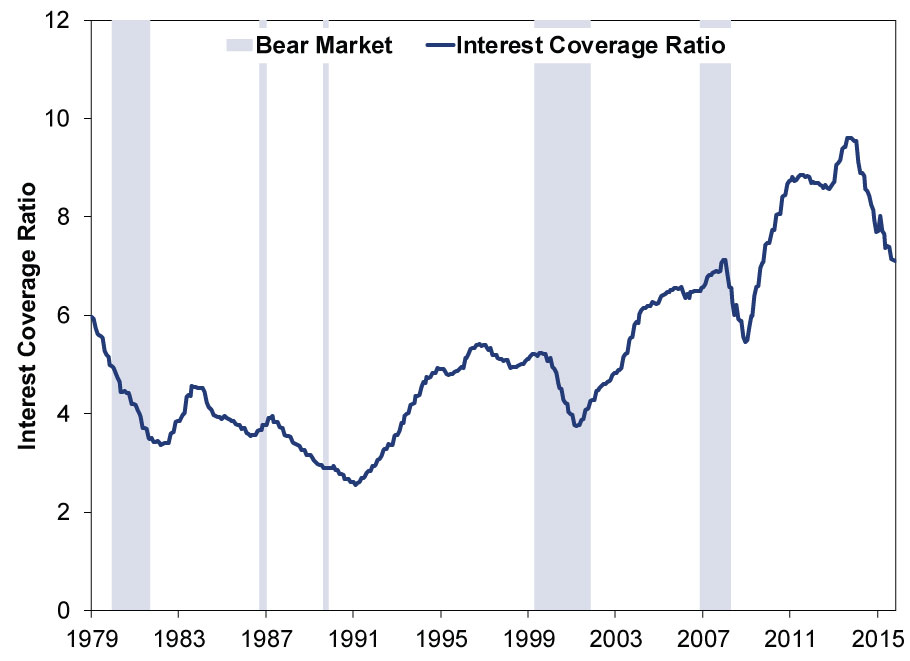

But even this is incomplete, because the amount of debt alone-whether absolute or relative-isn't telling about Corporate America's health. The ability to repay debt is what matters.

A useful way to evaluate this is the interest-coverage ratio, which compares a firm's interest expense to earnings before interest and taxes. The higher the ratio, the easier a firm can service its debt. While recent quarters have shown falling interest coverage, it is still at historically high levels. And, the recent decline seems in large part tied due to falling Energy earnings-a factor that seems poised to wane looking forward. (Exhibit 3)

Exhibit 3: S&P 500 (ex. Financials) Interest Coverage Ratio

Source: Thomson QAI, as of 9/30/2016. S&P 500 EBIT / Interest Expense, December 1979 - September 2016.

So, yes, debt has risen, but so have profits, and companies have refinanced a bunch of debt at lower rates. So there is more debt, but it is vastly cheaper debt and more affordable than any time in the last 30 years-including everyone's favorite bull market, the 1990s.

Some say, sure, companies can service their debt now, when borrowing rates are ultra-low. But when rates eventually rise, higher debt costs will imperil corporate America. But rising rates don't change debt-servicing costs overnight-it takes time for existing debt to mature and roll over to higher-yielding debt. Besides, while 10-year Treasury rates have drifted up recently, they are still very low and many factors (low inflation, foreign monetary policy and more) suggest they won't skyrocket soon. In the meantime, firms are refinancing maturing debt at lower rates. Plus, balance sheets are healthier than most presume: US nonfinancial firms are sitting on record amounts of cash-$1.9 trillion according to the Federal Reserve as of Q2 2016. Some of the borrowing is merely tax planning.

None of this is to say companies won't get over their heads in debt going forward. But so far, there is little evidence low rates are fueling a corporate debt binge.

HT: Youngro Yoon.

[i] We mean this in the correct, old-fashioned sense of the word "literally," not the newfangled one that actually means figuratively.

[ii] Very loose.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

In The News Expert says investors are ignoring a massive global rally2026-06-22

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22 -

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today