Personal Wealth Management / Market Analysis

The Only Article You Need to Read Before December’s Big Fed Meeting

Why a Fed rate hike should be fine for stocks.

Few things in financial markets are foregone conclusions, but here's something pretty close: Barring something extraordinary, the Fed probably raises rates on Wednesday. They might not! But considering how much they've hinted, and how much everyone presumes strengthening economic data and rising inflation warrant a rate hike, standing pat would be bizarre. Cutting rates would be really weird, too. Unlike this time last year, when your neighbor and dog[i] were probably sure a rate hike would end the expansion, this time, investors are pretty calm. While the myth of the Fed-fueled bull market persists, few think a quarter-point hike in overnight rates will kill it. We're inclined to agree (with everything but the "Fed-fueled bull market" part). Stocks and the economy should be just fine.

Short-term interest rates, on their own, aren't a market driver or hugely meaningful for the economy. No level or direction is inherently good or bad. What really matters is the yield curve spread-the gap between short-term and long-term rates. Short rates represent banks' funding costs. Long-term bond yields are the reference rate for banks' lending rates, a proxy for their revenues. The gap between them-long rates minus short rates-represents banks' profit on the next loan made. Wider spreads encourage more lending, adding fuel to the economy, while negative spreads usually choke lending and precede recessions. Hence, determining whether a rate hike will harm the economy requires looking at its potential impact on the yield curve.

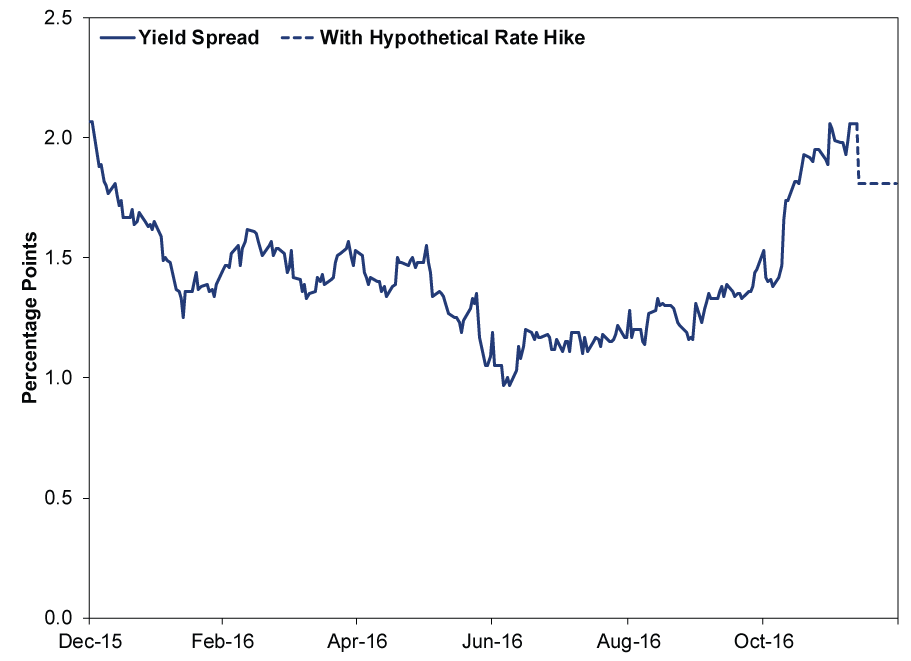

During 2016's first half, the US yield curve spread shrank as long rates fell globally, hitting just 97 basis points (or 0.97 percentage point) on July 8. But then it began widening gradually, and after a November surge, it is over 200 bps wide, near where it began the year. If the Fed hiked now and long rates didn't budge, the spread would shrink to 181 bps, still higher than where it was most of the year-and 2016's narrower spreads didn't derail growth.

Exhibit 1: US Yield Curve Spread Year to Date

Source: FactSet, as of 12/12/2016. 10-year US Treasury yield minus effective fed-funds rate, 12/31/2015 - 12/12/2016. Dotted line presumes a 25-basis point Fed rate cut and no movement in 10-year yields and is for illustrative purposes only.

Of course, long rates aren't guaranteed to hold still. They are a market function, not controlled by the Fed. They could be stable, or rise a bit, or fall, depending on how global bond market forces evolve. But whether they drift a bit higher or lower, the yield spread should remain sufficiently wide to encourage lending.

Rate hikes typically don't become problematic until the Fed overshoots, hiking short-term rates above long rates. With the two more than 200 bps apart, as things stand now, the US economy can likely withstand several rate hikes before they become problematic. As investors realize this and continue getting over rate hike fears, improving sentiment should be a modest tailwind for stocks.

[i] Unless you have a dachshund. Those pups don't have a clue about monetary policy.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today