Personal Wealth Management / Market Analysis

The Other Fightin’ Irish

Ireland is getting ever-closer to returning to debt markets—setting it up for a potentially satisfying 2013-2014 season.

While one Irish team saw their hopes swept out with the tide Monday night, another is seemingly poised for a better spring: Ireland is nearing a full return to debt markets and continues planning to launch a new benchmark 10-year bond. In fact, progress was made along those lines Tuesday when Ireland launched its first syndicated bond deal since its bailout in late 2010. This follows its first medium-term debt offering, which was made last summer.

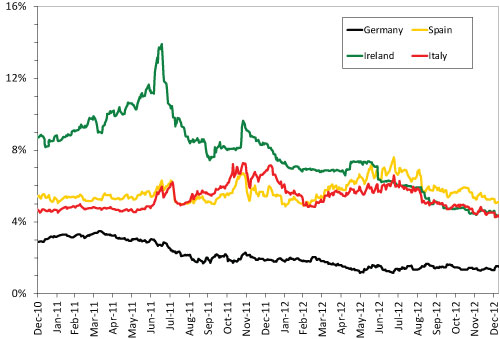

Combined with Irish yields, the news paints a picture of a country which has made significant progress since a property market crash tied to 2008’s global financial crisis caused Irish lenders Anglo Irish Bank Corp. and Irish Nationwide Building Society to effectively fail. As shown in Exhibit 1, Irish yields have fallen meaningfully—and the spread between Irish bonds and German bunds has narrowed significantly, falling from a high of over 11 percentage points to under 3 (2.85, to be precise). In fact, Irish yields are now below Spain’s and are effectively equal to Italy’s.

Exhibit 1: Peripheral European 10-Year Yields

Source: Thomson Reuters, as of 1/8/2013.

The news also highlights starkly the difference between Ireland and some others in Europe’s periphery—a point we’ve made before in this space, but one that bears repeating. The source of Ireland’s woes is very different from the source of Italy’s or Spain’s or Greece’s or Portugal’s. By and large, those countries are suffering from competitiveness issues in many ways resulting from a socialism-to-capitalism ratio that’s been far too out of whack for far too many years. In some, that’s resulted in bloated public sectors that borrowed at artificially low rates and are now paying the piper (we’re looking in your general direction, Greece). In others, it’s resulted in a non-profit banking sector that (predictably) doesn’t turn a profit and therefore, when faced with too-high default rates tied to a real estate bubble’s bursting, doesn’t have sufficient capital to continue functioning without a bailout (your turn, Spain).

We won’t belabor the point—suffice it to say, Ireland’s problems were arguably much less structural than they were a result of a global banking panic. Going on five years later, though, it’s hard to argue significant progress hasn’t been made—which isn’t to say Ireland won’t continue facing challenges for potentially the next couple years.

For example, consider the dilemma presented by this mix: Government spending necessarily increased when it decided to bail out then-failing banks (likely the right move at the time), spiking the debt-to-GDP ratio and likely helping drive yields higher. As yields increased, Ireland was increasingly unable to finance its debt, leading ultimately to the request for the bailout. But a condition of the bailout was cutting government spending. Thanks to (in our view, quirky) accounting, GDP counts government spending as a positive contributor, so cutting government spending hurts GDP, worsening the debt-to-GDP ratio without conditions’ otherwise changing (that’s just pure math). Meanwhile, slowing GDP for other reasons (like relative overall eurozone weakness slowing Ireland’s economy some) hurts tax revenues, further contributing to the debt-to-GDP issue.

Sounds like a rather unsolvable, vicious cycle, doesn’t it? But here’s the good news: Relatively reasonable (and likely still-falling) yields mean it’s much more affordable for Ireland to finance that debt than it was just a few short years ago. And while it still has work to do to fully regain international investors’ trust, lower yields are a tremendous help toward that goal—in turn making it more probable Ireland successfully hits its target of fully returning to debt markets in early 2014.

Then, too, consider that while GDP technically counts government spending as a net positive, in our view, it’s infinitely preferable to rely more on the private sector for the bulk of production. Meaning in the long run, the fact Ireland’s scaling back its government spending (through much-maligned austerity measures) is likely an overall good thing ultimately resulting in an overall leaner, fiercer international competitor. Something the rest of the eurozone seemingly implicitly recognizes.

So don’t count the Irish out just yet—they still have more than a fighting chance. In fact, we wouldn’t be surprised if the 2013-2014 season proves more satisfying for the Celtic Tiger than 2012 was for their cousins stateside.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today