Personal Wealth Management / Financial Planning

The Reality Behind Social Security’s 2033 ‘Depletion’

COVID’s impact isn’t quite what headlines imply.

Tuesday afternoon, the Social Security and Medicare Boards of Trustees released their delayed annual report on the state of their respective trust funds. The Social Security report in particular always generates a ton of headlines for its grim projections about when the trust will run out, allegedly chopping retirement benefits overnight. True to form, this year’s report spurred headlines coast to coast, all focused on COVID’s impact, which amounted to moving the depletion date up one year from 2034 to 2033. As always, we think investors mapping out their far-future retirement cash flow needs should take the projections and the handwringing with many grains of salt, as nothing here is etched in stone.

Practically, it matters little whether the trust fund is scheduled to run out in 2033 or 2034, as this is mostly a political deadline—Congress can always act as needed to ensure the trust fund’s ongoing viability. Options include raising the retirement age, tweaking the way benefits are calculated, adjusting the cap on earnings subject to payroll taxes and more. Congress has used all of these tricks before. They just haven’t done so since the early 1980s, which happens to be the last time the fund appeared to be stumbling toward insolvency. Necessity is the mother of legislation, and if we know politicians at all, we know they will delay action as long as possible before finally tweaking the system for fear of being seen as hurting people who paid into the system. But eventually they will act, and they will likely try sparing current and soon-to-be beneficiaries from being hit, as that would be bad politics. Yes, that is a somewhat cynical view, but we also think it is pretty realistic. So, a few years from now, if (more likely, when) they raise the retirement age for people born from around 1980 onward and bump the cap on earnings subject to the payroll tax at around $200,000 annually, remember you heard it here first.[i]

With that said, it is far from guaranteed that 2033 is the actual deadline, as these projections are chock full of guesswork and uncertainty—especially the pandemic-related parts. Taking their cues from the trustees’ commentary, pundits largely pinned the accelerated shortfall on COVID. As one outlet put it: “The Covid-19 pandemic and economic recession are to blame for moving up the depletion rate by a year, driven by the big drop in employment and resulting decline in revenue from payroll taxes.”[ii] In their accompanying letter, the trustees wrote, “The finances of [Social Security and Medicare] have been significantly affected by the pandemic and the recession of 2020.”

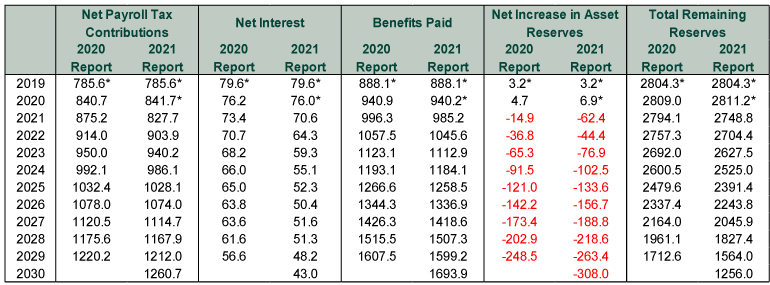

Have been. Past tense. So, logically, you might assume this means last year’s lockdowns knocked payroll tax revenue significantly, leading to a big shortfall that accelerated depletion. However, you would be wrong. Net payroll tax contributions actually rose by about $56 billion last year. They also beat the projections in last year’s report, which as the trustees noted, did not include the estimated effects of the pandemic. As a result, the trust fund ran a surplus of $6.9 billion, smashing the $4.7 billion surplus projected a year ago. For those keeping score, the level of reserves at year-end, $2.81 trillion, was the highest since 2017 and second-highest on record. So all in all, for all the pain we, our readers and society as a whole suffered on a personal level, last year was a pretty good year for Social Security’s coffers—better than expected, to say the least.

What the trustees are actually referring to is their decision to reduce their forecasts for the next nine years. They have reduced projected payroll tax revenue for every year through 2029, and they see it outright falling in 2021. They have also penciled in less interest income, thanks to low US Treasury yields. The slower projected spending on benefits (resulting from COVID-19’s tragic impact on the mortality rate) only partly offsets the lower projected revenues, leading to larger deficits predicted in every year.

Exhibit 1: Comparing 2020’s and 2021’s Social Security Projections

Source: Social Security Administration, as of 9/1/2021. Data are from Table VI.C4 in the 2020 Trustees Report and Table VI.C5 in the 2021 Trustees Report. All figures are in billions of current dollars and cover the Old Age and Survivors Insurance Trust Fund. * denotes actual data; the other years are SSA forecasts.

That raises the ever-important question: Are they riiiiiiiiiiiiiiiiiiiiiight? Employment is already up significantly from 2020. Nonfarm payrolls are still down from February 2020’s peak by 5.7 million, but is that enough to lead to a $14 billion drop in payroll tax revenue next year?[iii] Put it this way: Total nonfarm payrolls bottomed out at 130.2 million in April 2020, then rose to finish the year at 142.5 million.[iv] Since then, they have increased gradually to 146.8 million.[v] Plus, which this is perhaps a bit indelicate, most of the remaining employment shortfall is in lower-wage endeavors. Total compensation of employees is already $694.4 billion above its pre-pandemic level.[vi] Yes, some of this increase no doubt went to people whose income is above the payroll tax cap, but plenty of it likely also went to people who had been out of work and hard-working folks at the lower end of the income spectrum. So overall, we have a hard time seeing what the trustees’ precise logic is here.

Beyond near-term quibbles about the pandemic’s impact, we would apply all the usual caveats about long-term mathematical modeling and the underlying presumptions about interest rates, economic growth, birthrates, immigration and all the rest. Those are unknowable even 2 and 5 years out, never mind 75 years (the projections run through 2095). They are academic, actuarial exercises with generally little grounding in the real world.

Regardless, let us pretend these forecasts turn out 100% accurate. Let us also pretend that Congresspeople collectively decide they don’t want to be re-elected and don’t adjust anything to prevent the trust’s depletion. What happens then? Well, in short, people still get retirement benefits. Social Security has always paid current beneficiaries with current revenues. With apologies to Al Gore, it is not and has never been a lockbox. (Find the Saturday Night Live bit on this. It is gold.) The vaunted trust does not fund benefits every year—it is the accumulation of decades of surpluses. If it depletes in order to ensure benefits are fully funded over the next decade, then—by the trustees’ own estimates—annual revenues will still fund about 76% of annual benefits.

Again though, this is all political. The trustees have incentive to publicize depletion dates in an effort to goad Congress into acting. They are the intended audience here—not retirement savers. If you want to save more and plan your investments so that you rely more on your portfolio and less on Uncle Sam in retirement, by all means do so! But in our view, the notion that anything in today’s report necessitates huge changes from a financial planning standpoint—or represents a looming fiscal cliff for current retirees—is quite far fetched.

[i] These are totally unscientific guesses.

[ii] “Social Security Won’t Be Able to Pay Full Benefits by 2034, a Year Earlier Than Expected Due to the Pandemic,” Katie Lobosco, CNN, 9/1/2021.

[iii] Source: St. Louis Federal Reserve, as of 9/1/2021.

[iv] Ibid.

[v] Ibid.

[vi] Source: BEA, as of 9/1/2021. Compensation of employees, seasonally adjusted annual rate, Q4 2019 – Q2 2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today