Personal Wealth Management / Market Analysis

The Return of the Retail Investor

It seems the average investor’s appreciation of stocks might be picking up these days—in response, the media’s claiming both doom and boom for markets ahead.

Are stocks in a bubble? Or is a lack of retail investor optimism weighing down equities? These seemingly contradictory questions stem from recent media takes on fund flows—the amount of money going in and out of mutual funds. In our view, though, fund flows are merely an imperfect sentiment marker—and right now, they neither point to inflated markets nor an absence of investors. Rather they suggest signs of budding optimism—newfound cheeriness, but not at levels indicating euphoria, implying recent inflows likely aren’t a warning sign of a market about to roll over.

Recent data show investors have flocked into stock-oriented mutual funds and ETFs this year. One school of thought fears it’s a stampede—a warning sign. According to them, investors, seeing recent strong gains in stocks, have started piling into markets because they’re afraid of missing the rally. As a result, stocks are frothing. Looking at recent history, this viewpoint has some credence: Markets have at times moved against fund flows. But the evidence is inconsistent at best—you can’t assume the stocks will move opposite the casual investor. Fund flows aren’t a contrarian indicator—divining their meaning requires looking much deeper to see if economic reality is in line with the direction funds are flowing. Make sure the fundamentals check out.

Said differently, some optimism is just plain rational. A bubble is far different. Bubbles happen when returns are far disconnected from fundamentals; when folks overlook growing negative fundamentals out of greed. To have a bubble, it’s virtually requisite that few folks see the scenario as a bubble. It’s a new economy; companies’ profits don’t matter; it’s different this time. The fact bubble fear is widely discussed suggests stocks haven’t reached their boiling point. Moreover, vast positive economic data do support stocks’ growth, and leading economic indicators suggest there’s more to come—stocks are just one of those indicators, making a disconnect between stock returns and bubbles seem more likely than between stock returns and the economy.

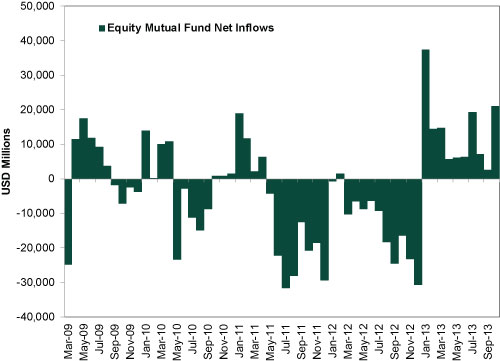

The other school of thought takes the opposite view—they want more inflows! Their theory: Investors, still shaking from the last financial crisis, aren’t entering markets quickly enough, and that lack of participation—despite strong stock growth so far—will sap this bull’s life force. Which is a strange concern in our view. For one, four years of heavy net outflows didn’t buck the bull from 2009 through 2012 (Exhibit 1). Two, stocks don’t need new buyers to keep on rising. They just need investors willing to bid shares higher—it’s an auction marketplace. You can have a hot bidding war with just two people. And they needn’t be new investors—folks can always sell one stock at the going rate and use the proceeds to bid up another. Multiply that by a few million transactions, and that’s how markets move—if buyers are overall more willing to bid up shares, stocks rise.

Exhibit 1: Monthly Net Equity Mutual Fund Inflows

Source: Investment Company Institute, as of 12/20/2013.

In our view, recent fund flow data are one more sign this bull market has climbed a wall of worry since it began—and should have plenty more left to climb. As we’re likely near the halfway point of this bull market, it isn’t surprising many retail investors who have been skittish on stocks thus far are just now slowly re-entering equity markets. It takes a while for the emotional scar tissue of the last bear market to fade. Investors are now starting to realize stocks are resilient and still have opportunities. They’re warming up to the idea things aren’t as bad as they assumed for the last four-and-a-half years.

This doesn’t have to put a ceiling on the market. In this case, it should be a tailwind! According to investing legend Sir John Templeton, “Bull markets are born in pessimism, grow on skepticism, mature on optimism and die on euphoria.” Strong fundamentals have supported growth thus far, but sentiment has largely been skeptical, with optimists starting the occasional tug of war. That some investors are now returning to stock markets suggests they’re starting to recognize those healthy fundamentals, boosting their confidence in markets’ sustainability. As this confidence drives them to bid stocks up—and as the economy continues chugging along—others who are still holding back likely begin to feel more confident, too, and they’ll bid prices higher. This ascending confidence is a powerful force for stocks, and it can last quite a while before sentiment reaches the euphoria of bull market peaks.

Fund flows suggest this confidence climb is in the very early going. As do more qualitative assessments of sentiment. Heck, the contradictory, dour interpretations of fund flows suggests investors are far from uniformly optimistic. And sentiment could retreat again—it did once this year, regardless of how unwarranted it was. What investors should mind instead is the longer it takes for folks to toe into optimism, the longer the bull likely lasts—and the longer they have to capitalize on future gains.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today