Personal Wealth Management / Economics

The UK Might Do Some Things to Taxes and Spending

The UK's latest tax and spending plans are about as "austere" as the last five years-and likely have little net economic impact.

UK Chancellor George Osborne leaves 11 Downing Street to deliver the Autumn Statement. Source: Getty Images.

UK Chancellor George Osborne delivered the annual budgetary theatrics known as the Autumn Statement on Wednesday, and depending on your point of view, this package of pledges and fiscal tweaks that may or may not make next year's actual Budget [i] was a) an austerity nightmare or b) a supply-side economic reform miracle with an unfortunate side of bank bashing. Ah, ideology. In reality, though, it's about what you'd expect for a government's last fiscal hurrah before general election: 108 pages of charts, bullet points, tax tweaks and spending plans that create a few winners and losers, strike a populist note and overall do a whole lot of nothing. Whether you think these plans are a blessing or curse, the likely economic and market impact here is small.

First to the "austerity" in the form of "spending cuts," which snatched most eyeballs. The current government has sought to balance the budget since it took over in 2010, initially targeting a small surplus in fiscal 2015-2016 (0.3% of GDP, compared with the -7.6% of GDP deficit in 2009-2010). However, reality has forced them to push this out two years and continually fine-tune spending plans with a series of "austerity" budgets that weren't actually austere in terms of spending reductions-projected spending increases were trimmed a tad, but not actual spending.

The spending projections in 2014's Autumn Statement are what we've seen since 2010-a period where the public sector did not radically shrink for good or ill. Yes, plans to bring total managed expenditure (TME) to 35.2% of GDP by 2020 sounds radical-lowest spending since the 1930s! Some expect a fiscal bloodbath, with one think tank warning a million public sector jobs could vanish. Thing is, spending would not be all that low. It would actually be an all-time high. Just a smaller all-time high than they might otherwise have speculated. No way to know-this is the first 2020 projection. And, for that matter, if Labour or a Labour-led coalition takes the reins from this Conservative/Liberal Democratic coalition at next year's election, these long-term spending plans could all go out the window.

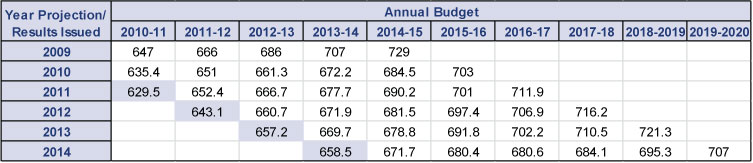

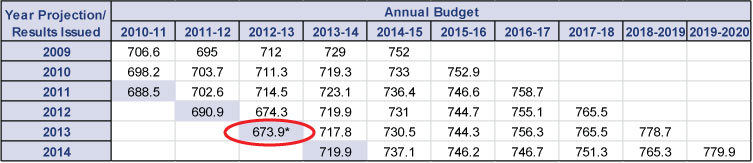

Anyway, we don't see much economic impact here. As Exhibit 1 shows, total public spending wouldn't fall ever, just as it never fell once during this government's administration. TME, which includes net investment (gross investment minus depreciation) would keep rising, too (Exhibit 2). And if it didn't? There is no evidence this would be a huge negative. The private sector could very well pick up the slack. Heck, the only time TME fell during this administration-fiscal 2012-2013-GDP held up fine and accelerated at the end. And that austerity comes with an asterisk, as TME was artificially reduced by the Royal Mail privatization. Without that accounting adjustment, TME would have risen then, too, to £701.9 billion. Actually, the UK economy has done overall fine through these faux-austere years. GDP was choppy through 2012, but that had more to do with quantitative easing squeezing the interest rate spread and, along with regulatory confusion, whacking loan and broad money supply growth. We find it telling growth accelerated in a year that had no QE and the vestiges of an austerity TME cut.

Exhibit 1: Projected and Actual UK Public Spending (Excluding Investment)

Source: 2009 Pre-Budget Report; 2010 Economic and Fiscal Outlook; 2011, 2012, 2013 and 2014 Autumn Statements. All figures are in billions of pounds sterling. Shaded boxes are actual results, unshaded are projections.

Exhibit 2: Projected and Actual UK Total Managed Expenditure

Source: 2009 Pre-Budget Report; 2010 Economic and Fiscal Outlook; 2011, 2012, 2013 and 2014 Autumn Statements. All figures are in billions of pounds sterling. Shaded boxes are actual results, unshaded are projections. Austerity is in the little red oval. *Is there because only the Royal Mail privatization made this drop, knocking £28 billion off the actual TME of £701.9 billion with accounting gimmickry.

So that's all a thing. Or not. Actually, we found the tax tweaks to be where the real action is. Read between the lines a little, and they could very well be the Conservative Party's 2015 campaign tack in a nutshell-a dash of "fiscal responsibility," a pinch of tax-cut happiness and supply-side reform and a sprinkle of populism, all aimed at currying favor with voters who might lean Labour. Only time will tell how the gambit works, though, particularly with a good five months of campaigning and politicking ahead. This one is wide open.

While the political impact is impossible to game, the economic impact is fairly easy to assess. Extending Individual Savings Accounts' (ISA) tax-free status to deceased account holders' surviving spouses is a small plus. As is increasing ISAs' annual contribution limit a wee bit from £15,000 to £15,240 next April. Consumers will no doubt enjoy gas taxes holding steady and the abolition of taxes on international airline tickets for kids under 12 next May and under-16s the following March. A pledge to "review" business taxes, which hit brick-and-mortar shops hard, sounds nice, but is hollow. They did announce specifics on income taxes, though. The personal allowance for all rises from £10,000 to £10,600 next April, and the income threshold for the highest band rises 1.2% from this year's £41,865. It all amounts to a very incremental cut for everyone. Well, except those poor non-domiciled residents, some of whose annual charge will rise. Winners and losers.

The flagship tax measure, real estate stamp duty overhaul, also creates winners and losers. For 98% of homebuyers, it's a tax cut (read the finer points here if you want-we prefer not to bore you with math, because we are nice people). For those buying homes over £925,000, however, it is a tax hike. It's particularly crippling for those buying homes over £2 million, whose tax bill will jump by £50,000. Yeouch. Now, that's a very, very small subset of the UK housing market-basically, high-end London. Some speculate this could crush that market, but we don't see it. Communism-fleeing Chinese tycoons and Russian oligarchs who splurge on Kensington mansions will probably keep at it. Taxes matter, but those folks have other incentives, too. Like sheltering their money from kleptocracies.[ii]

Finally, on to the corporate tax front, where we saved the worst for last.[iii] Banks get punched-odd, considering the government considers itself business-friendly and often lobbies to protect its banks from EU tax and regulatory madness, but also consistent with this government's MO since Day One. Banks aren't popular with people, so hitting them with small annoying taxes curries favor with voters. In past years, it was the tax on bank balance sheets. This time, it's adjusting the tax treatment of prior losses used to offset taxable profits. Historically, banks have been able to book all prior losses against current/future profits, lowering the burden. But from April 2015, the allowable amount falls to 50%. A headwind, but also a very small one. The government expects the change to increase banks' tax bills by just £3.5 billion over the next five years. Big!! But 0.05% of the banking system's total assets over that entire period. Small. A few big banks will take small earnings hits, but this shouldn't much crimp future lending.

The other potential change, which the UK media dubbed the "Google Tax ," is even smaller, but snazzy and so in vogue these days. The 25% tax on profits multinational firms divert to avoid UK corporate taxes is supposedly a means of nudging firms into restructuring, but details are scarce. There is also no guarantee this can take effect, much less pile on taxes or restructuring costs for multinationals. Tax experts and attorneys are already contesting the international legality of this measure, and international law makes defining UK-attributable profits difficult. In short, we highly doubt this tips the tax's namesake and other similar firms take a tax beating over this any time soon.

So, to recap: Politics, imaginary austerity, winners, losers, meh. The winners are no doubt happy, and the losers probably feel the pain about two and a half times harder, but both ends are so incremental that there probably just isn't much impact. As far as markets are concerned, we'd chalk this Autumn Statement up as a political marketing ploy without much substance.

[i] It is a proper noun there, which we enjoy to no end.

[ii] We thought about including tax-fleeing French people here, but we aren't so sure. This probably reduces the incentives for them to jump the channel a teensy bit.

[iii] You're welcome? Sorry? We aren't sure?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today