Personal Wealth Management / Economics

The US Can Afford Its Debt

US deficits and debt are not problematic for the economy.

The full faith and credit backing bonds issued at this building is still good. Photo by Raymond Boyd/Getty Images.

Uncle Sam's fiscal year ended Wednesday, and if the Treasury's most recent data are any indication, the deficit is set to fall again. Per the latest Monthly Treasury Statement, as of August, the fiscal year 2015 deficit is $530 billion, $59 billion below August 2014's year-to-date tally and on track for the fourth straight reduction. Folks, if you've wondered why the deficit isn't getting the headlines it did five years ago, this is why: It's hard to create an alarming narrative from such benign numbers, and bad news is what sells. But we think the latest numbers are worth exploring as yet more evidence US deficits and debt are not problematic for the economy or markets.

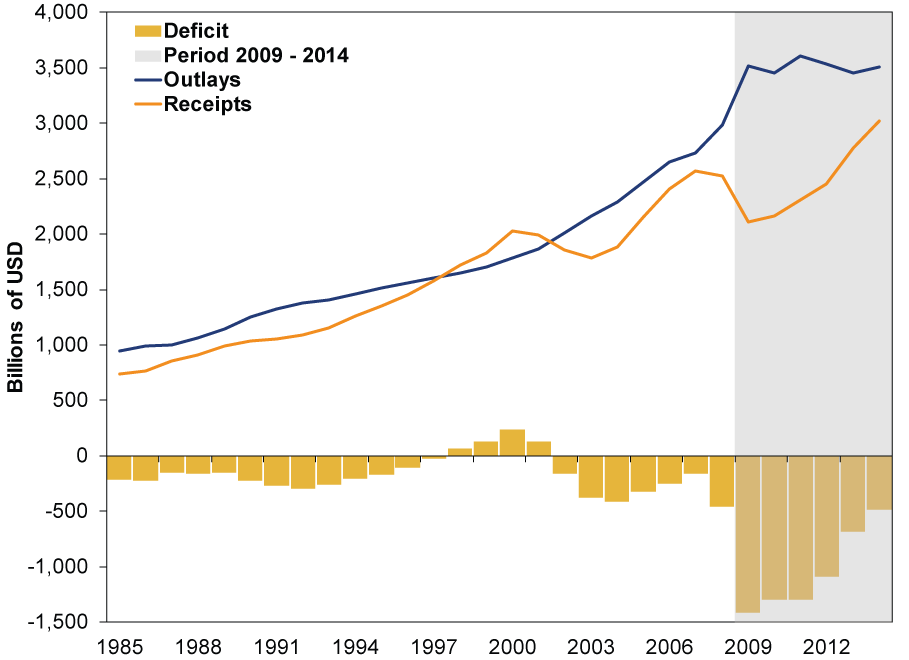

$530 billion is a big number. It's bigger than any deficit before 2009, and if our deficit were a country, it would be the world's 26th-largest economy, between Belgium and Taiwan. But scaling, as ever, is key. At 2.4% of GDP, it is below America's average deficit/GDP ratio over the last 50 years. $530 billion is also just over one-third the size of 2009's whopping $1.4 trillion deficit, a byproduct of the financial crisis, stimulus and recession. Back then, folks feared spiraling deficits would sap growth, but they didn't. The spike was only temporary, and a growing economy and 2012's tax measures boosted revenue. This, along with flattish overall spending, chopped the deficit tremendously.

Exhibit 1: US Federal Deficits, Outlays and Revenues 1985-2014

Source: Office of Management and Budget, as of 9/29/2015.

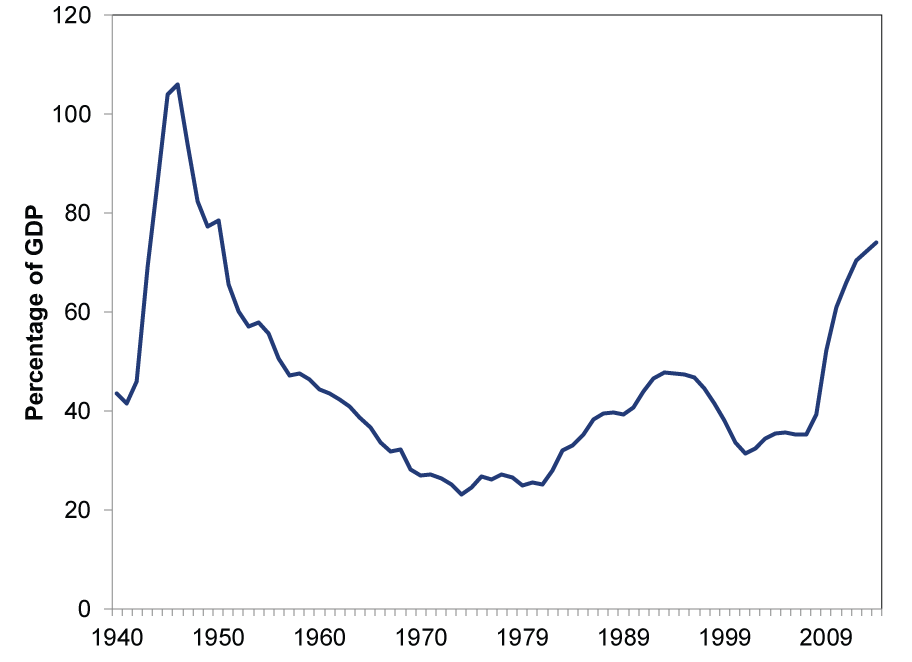

Here some might say, yeah, but even smaller deficits add to debt, and debt is still rising. That's certainly true, but modestly higher debt isn't a problem for markets or the economy. Total net public debt, which excludes inter-governmental holdings, is $13 trillion, or 73% of GDP, as of Q2 2015. High relative to the last 50 years, but it reached 109% during the 1940s as the government borrowed massively to finance WWII, and that didn't prevent a big post-war boom.

Exhibit 2: Net Public Debt as a Percentage of GDP 1940-2014

Source: Office of Management and Budget, as of 9/29/2015. [i]

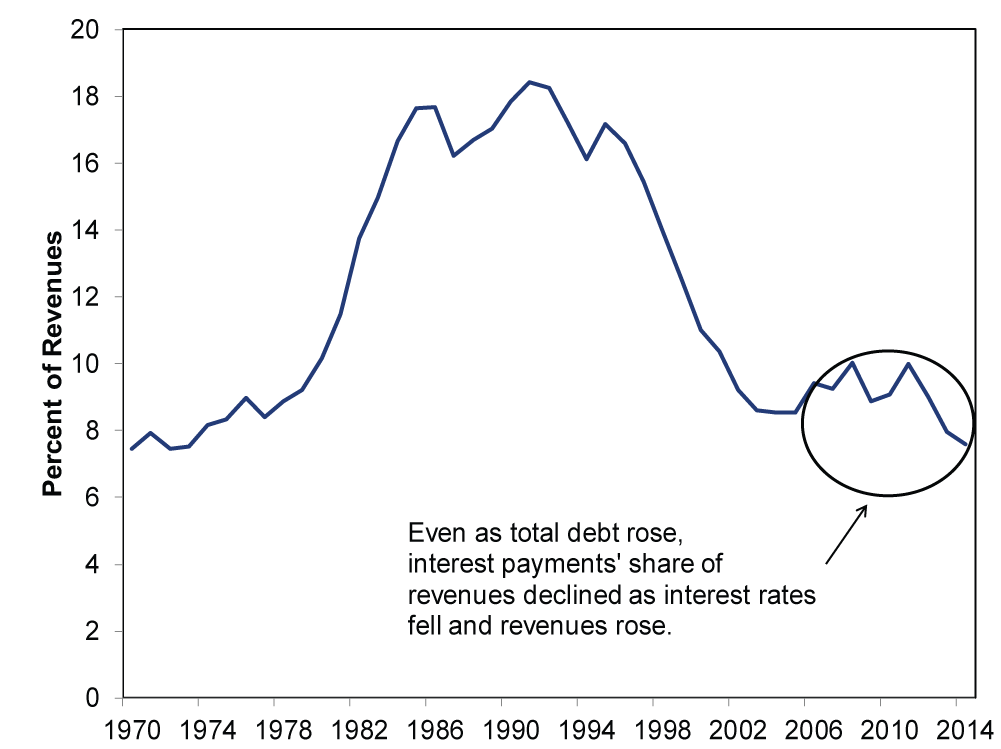

Moreover, even as debt has grown, it has become more affordable-and affordability is the kicker. Fiscal crises happen when countries can't service existing debt or borrow at tolerable rates. Our debt load is cheap and getting even cheaper, even as debt grows. Interest payments relative to tax revenues (Exhibit 3) are below 8%, their lowest level since the early 1970s. They're far, far lower than much of the 1980s and 1990s, great times for the economy and markets. Not only are absolute revenues up, but total interest payments have fallen the last couple years as we've issued and refinanced maturing debt at cheaper rates, making our existing debt stock radically cheaper.

Exhibit 3: Federal Interest Payments' Share of Revenues

Source: Federal Reserve Bank of St. Louis, as of 9/29/2015.

Even if interest rates rise, US debt service probably won't break the bank. Higher interest rates impact newly issued bonds only. Considering the weighted average maturity of marketable debt outstanding is 69.6 months, it would take years for all (or even most) US debt to roll over at higher rates. Moreover, the weighted average yield is just 2.02%, and bonds maturing today are still refinanced at lower rates than when they were first issued. 10 years ago, we paid 4.4% on 10-year bonds. As of Wednesday's close, we pay just 2.04%. Most bonds are similarly cheaper up and down the yield curve. For debt to become unaffordable, rates would have to skyrocket and stay there for some time-far longer than that blip of double-digit rates 35-ish years ago.

Anything is possible in the long run, of course, but markets move on probabilities within the foreseeable future. In that window, rates seem exceedingly unlikely to soar. For one, sky-high interest rates usually entail soaring inflation expectations, a la the late 1970s/early 1980s. Today is nothing like then, when the legacy of price controls and misguided monetary policy (compounded by the oil shock) wreaked havoc. The global commodity slump remains a big deflationary pressure, and the supply glut should keep prices down a while longer, at least. Low foreign yields also keep interest rates low here as eurozone and Japanese QE programs restrict high-quality sovereign debt supply globally, boosting demand for US Treasurys.

Perhaps most importantly, the US remains the world's lowest credit risk. Yield, after all, is compensation for risk, and low US long-term bond yields are a sign investors have utmost confidence in the full faith and credit of the US Treasury. Since default risk is as low as can be, bond buyers don't demand high returns. Yes, the Fed has monkeyed with the market, but quantitative easing is far from the sole source of demand. Pension funds, insurance companies, banks, other institutions and individual investors worldwide buy Treasurys in droves, seeking stability over return. For that to change, it would likely require an enormous financial shock. 2011's US credit downgrade, Congress's perpetual brinkmanship, the biggest financial crisis since the 1930s and back-to-back worse-than-average bear markets didn't wreck the US's standing. It is highly, highly unlikely something far worse than these events materializes in the foreseeable future.

We probably haven't heard the last of debt fears. They're one of the oldest, most timeless bricks in the wall of worry. But unless something changes radically, the risk America's IOUs pose to the economy and stocks is next to nil.

[i] In case you are wondering, the postwar debt/GDP plunge was mostly due to stable government spending and debt levels and rising revenue as the economy grew in the postwar era, as this chart shows. Debt didn't fall much, but the ratio did.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility Anatomy of a (Near-)Correction2026-04-16

-

Macro Insights Q1 2026 Executive Summary2026-04-14

-

Expert Commentary Q1 Earnings, China GDP, Global Economy | 3 Things You Need to Know This Week

2026-04-13

2026-04-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—April 6 - April 102026-04-13

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today