Personal Wealth Management / Market Analysis

The Yuan’s Symbolic Ascent

The IMF adding the yuan to the SDR will not dethrone the dollar as the world's preferred reserve currency.

Welp, it's all but official: IMF Managing Director Christine Lagarde blessed the yuan's inclusion in the IMF's Special Drawing Rights (SDR) reserve currency basket, making it exceedingly likely the IMF's board votes later this month to add the yuan. Talking heads are already trying to quantify the impact on global currency reserves, with some estimating $1 trillion in reserve assets or more could flip from dollars to yuan. This may rekindle one of investors' long-running fears: the US dollar losing its top reserve currency status. For years, folks have feared foreign central banks will replace dollar-denominated assets with other currencies, selling US Treasurys by the boatload. This will supposedly drive US interest rates higher, choke off growth and make our debt unaffordable, leading to catastrophe. Folks, this has always been a false fear, and it remains so, regardless of chatter to the contrary.

First, a little background. Central banks stockpile reserves of foreign assets (typically, bank notes and sovereign bonds) to minimize big, disruptive swings in their own currencies that might threaten trade, foreign investment or the country's ability to implement monetary policy. If a currency plunges, the central bank can sell foreign reserves and buy domestic assets, defending its currency (as Russia has done on and off the past 18 months). If officials think the currency is too strong, central banks can counter by selling domestic assets and buying foreign (as Switzerland did before dropping the franc's ceiling in January). The dollar is top banana in the reserve currency world, followed by the euro. About $4.2 trillion of global reserves are in dollar-denominated assets, primarily Treasury bonds. It is here those debt concerns crop up, because if those are sold, folks fear fallout.

The SDR, created in 1969 to shore up the post-war Bretton Woods currency system, is one asset nations can use in reserves. After Bretton Woods fell in 1971 and most major currencies floated, the world had less need for a standardized reserve accounting unit, but the SDR lives on in IMF bailouts to distressed countries. SDRs can't be held by individuals or institutions, only countries. SDRs aren't a currency, in the sense they cannot be spent. Technically, the SDR is an accounting unit-a claim on multiple currencies. Presently, it includes the world's four most convertible currencies: US dollars, British pounds, euros and Japanese yen.

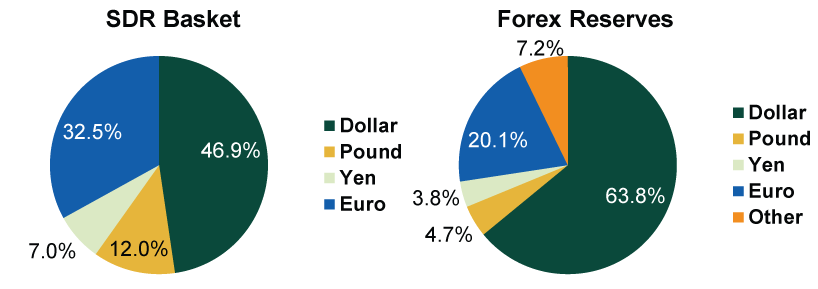

Some claim SDRs will replace the dollar as the world's primary reserve currency, but this ignores the fact nations receiving SDRs must convert them to actual currencies before they can deploy the funds. SDRs account for just ~$200 billion of the current ~$11 trillion of outstanding forex reserves globally. A central bank can elect to hold any currency (mostly in the form of sovereign debt, to reap some return) even if it isn't in the SDR. Central banks today hold plenty of Canadian dollars, Australian dollars and Swiss francs, even though none are in the SDR. And just because a currency is included in the SDR doesn't necessarily mean central banks flock to acquire them. As Exhibit 1 shows, the yen, pound and euro have far bigger weightings in the SDR than they do in actual foreign reserves.

Exhibit 1: The SDR Isn't a Forex Blueprint

Source: IMF, as of 11/17/2015.

The yuan being part of the SDR-should this happen-simply means member countries carrying SDRs in their reserves would get some yuan if they cashed them in, should they wish to. Ultimately it is a symbolic move.

And it is a symbolic move that would have little to no impact on the dollar. Dollars account for the lion's share of foreign reserves because the US sovereign debt market is the deepest and most liquid in the world. There are over $13 trillion of outstanding, tradeable US Treasurys. That is over $10 trillion more than the UK, with $2.1 trillion in tradeable outstanding government bonds. There are more euro-denominated bonds, but they're divided across several countries: Germany has about $1.2 trillion, France has $1.7 trillion, Italy has $2 trillion and Spain has roughly $827 billion-and the ECB and eurozone banks have gobbled up much of the outstanding supply. Japan has just over $8.5 trillion of total outstanding federal debt, but much of this is held by the government and Japan Post. [i]

The yuan can dethrone the dollar as the world's reserve currency only if central banks replace their dollar-denominated assets with yuan-denominated assets, and there simply isn't enough of the latter for this to happen. Total Chinese central government debt totals just $1.4 trillion (not a perfect gauge, as this includes intergovernmental holdings). Since China heavily restricts foreign ownership of government debt, much of this simply isn't available for foreign central banks to hold, casting doubt on those predictions $1 trillion in reserve assets will soon convert to yuan. At last count, foreign investors owned just $15 billion in Chinese central government bonds. Maybe in the very, very, extremely long term the yuan does have a bigger slice of global reserves than the dollar. But either way, the US doesn't rely on official sector demand to finance its debt. Demand from banks, individual investors, private institutions and pension funds is more than sufficient.

The SDR also doesn't have much bearing on the other aspect of the dollar's reserve currency status: its use in international trade. Because China's yuan is directly convertible with very few currencies[ii], most Chinese trade happens in dollars, not yuan. If a Chinese toy manufacturer sells to a South African importer, the buyer must convert its rand to dollars to purchase the toys, and the Chinese firm then converts the dollars to yuan. Adding the yuan to the SDR won't change this-it depends on China establishing more direct currency conversion agreements. If they do, and the yuan were used more, it would likely be an incremental positive! It would mean fewer hassles for global trade, which likely means more global trade. And the dollar would be fine. The US government doesn't get a brokerage fee from being in the middle of these transactions. There is literally no benefit to the US from this.

Should the IMF decide to add the yuan to the SDR, some would see it as symbolizing China's reform progress and emergence in the global monetary system. Fair enough. But it doesn't mean the yuan will catapult to dollar-like prominence in the world stage overnight. For this to happen, China would need to further liberalize capital flow and the yuan's convertibility, make the yuan float freely, and increase the supply of its sovereign debt by leaps and bounds (which, if it happened in short order, would scare the heck out of the world). This will likely take a long time, and even if this scenario plays out, it still doesn't spell doom for the dollar. The more likely result is a deeper and more liquid global monetary system, a positive for the world.

[i] Source: The Saint Louis Federal Reserve as of Q2 2015, UK Debt Management Office as of September 2015, Federal Republic of Germany Finance Agency as of 11/11/2015, Agence France Tresor as of September 2015, Banco de Espana as of September 2015, Dipartmento del Tesoro as of September 2015 and Ministry of Finance Japan as of September 2015. US dollar figures based on the following exchange rates: 1 British pound = 1.52 dollars, 1 yen = .0081 dollars and 1 euro = 1.07 dollars.

[ii] Currently, the yuan is directly convertible with US dollars, Japanese yen, Australian dollars, British pounds, euros and Russian rubles.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today