Personal Wealth Management / Economics

Theories Miss the Mark on March’s Jobs Miss

Whether caused by the dollar or not, March's weak job gains hold little insight into the US economy and stocks' future.

Job growth slowed in March, and here is what people are saying about that: "Financial markets got the news Friday that March job creation was subpar, and that complicates the investment outlook." "It wasn't just that the economy added 126,000 jobs in March when we'd been expecting 245,000. It was also that we lost 69,000 jobs in revisions to previous months. These tend to mark turning points in the economy." "The March jobs report showed tell-tale signs that the factory sector is struggling and the broader economy is feeling the impact. ... manufacturing employment fell into contraction ... this is the broader impact from a stronger dollar hurting the export sector as well as domestic industry." The thing is, all this talk is a wee bit wide of the mark, in our view. Whatever happens with jobs today is always a function of what happened in the economy months ago-jobs aren't a leading indicator. Nor is March's manufacturing employment decline evidence the stronger dollar is about to take its toll on US stocks.

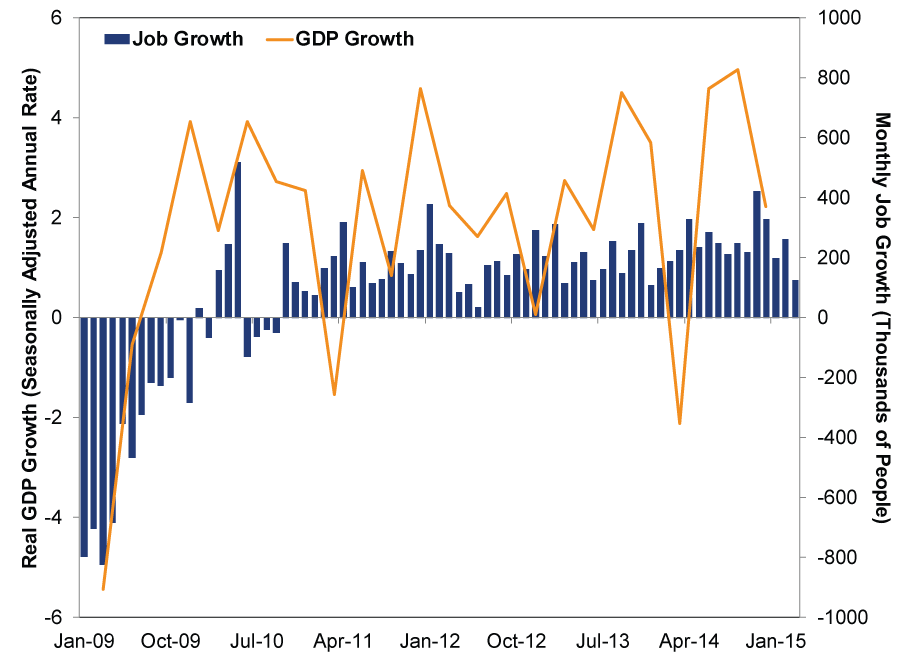

Economies move first. Then jobs. During the last recession, US GDP bottomed in June 2009. Employment kept falling and bottomed in February 2010. GDP growth accelerated in Q4 2011, then slowed a bit. Job growth accelerated in Q1 2012, then slowed a bit. GDP accelerated in Q2 and Q3, then slowed in Q4. Job growth accelerated in Q4 and early Q1, and now it is slowing. Here are all of those words in picture form.

Exhibit 1: Late-Lagging Job Growth

Source: FactSet, as of 4/6/2015. Monthly change in nonfarm payrolls, January 2009 - March 2015, and quarterly real GDP growth (seasonally adjusted annual rate), Q1 2009 - Q4 2014.

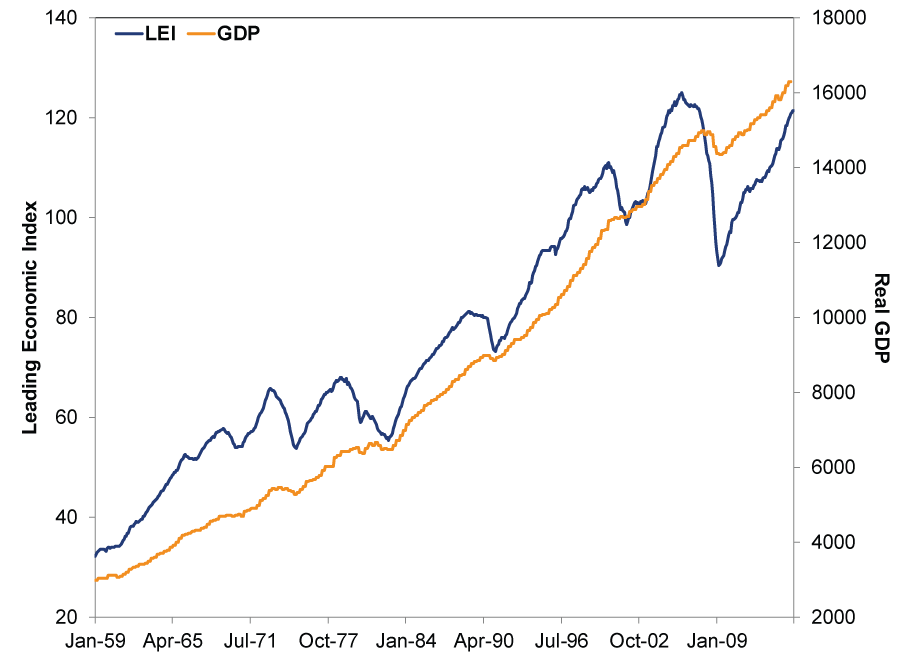

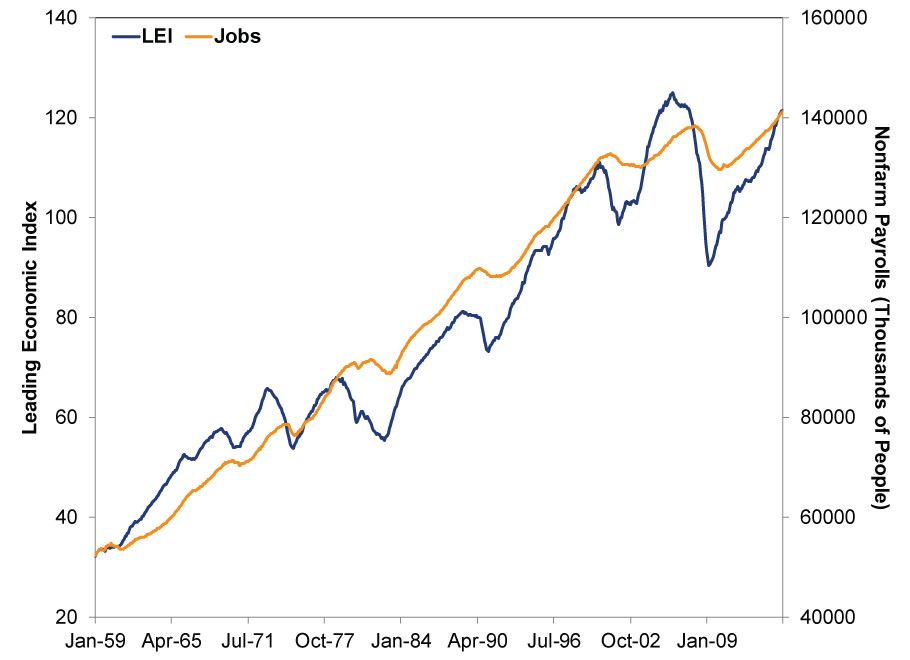

Job growth doesn't mark economic turning points. Nor do revisions to job growth-those lag reality even more. Job markets just confirm what coincident economic data already told us. None of it complicates stocks' outlook because stocks are forward-looking and pretty efficiently discount widely known information. Stocks typically fall for some time before recessions begin and resume rising well before they end. This is why stock prices are one of the 10 variables in The Conference Board's Leading Economic Index (LEI), a darned reliable indicator of future economic trends (Exhibit 2). Job growth is not in the LEI, because it doesn't lead (Exhibits 3 and 4).

Exhibit 2: LEI and GDP

Source: FactSet, as of 4/6/2015. The Conference Board's Leading Economic Index, January 1959 - March 2015, and real GDP, Q1 1959 - Q4 2014.

Exhibit 3: LEI and Jobs

Source: FactSet, as of 4/6/2015. The Conference Board's Leading Economic Index and total nonfarm payrolls, January 1959 - March 2015.

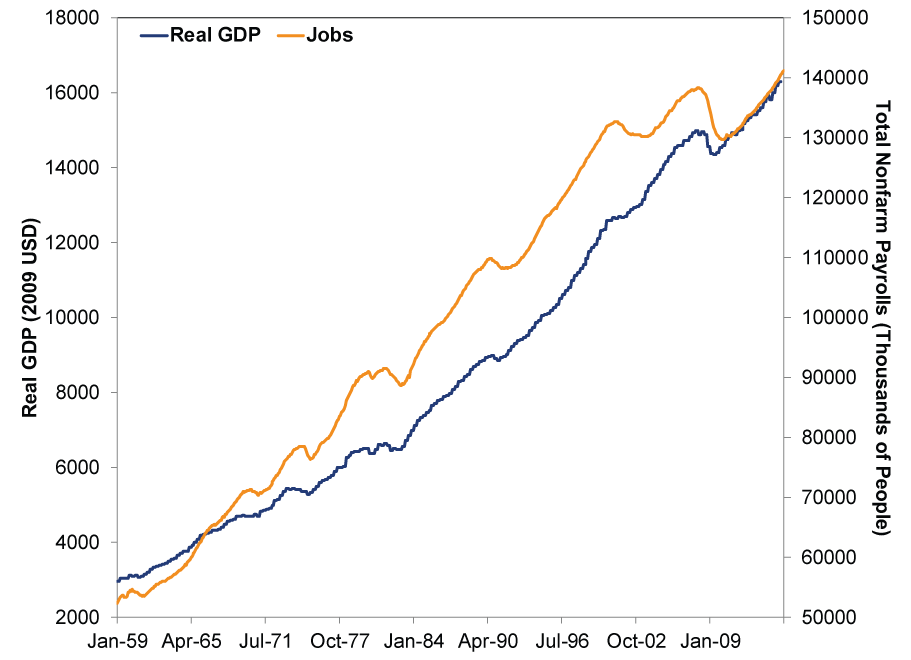

Exhibit 4: GDP and Jobs

Source: FactSet, as of 4/6/2015. Total nonfarm payrolls, January 1959 - March 2015, and real GDP, Q1 1959 - Q4 2014.

In those last two charts, the blue line turns before the orange line almost without fail. Jobs turn last.

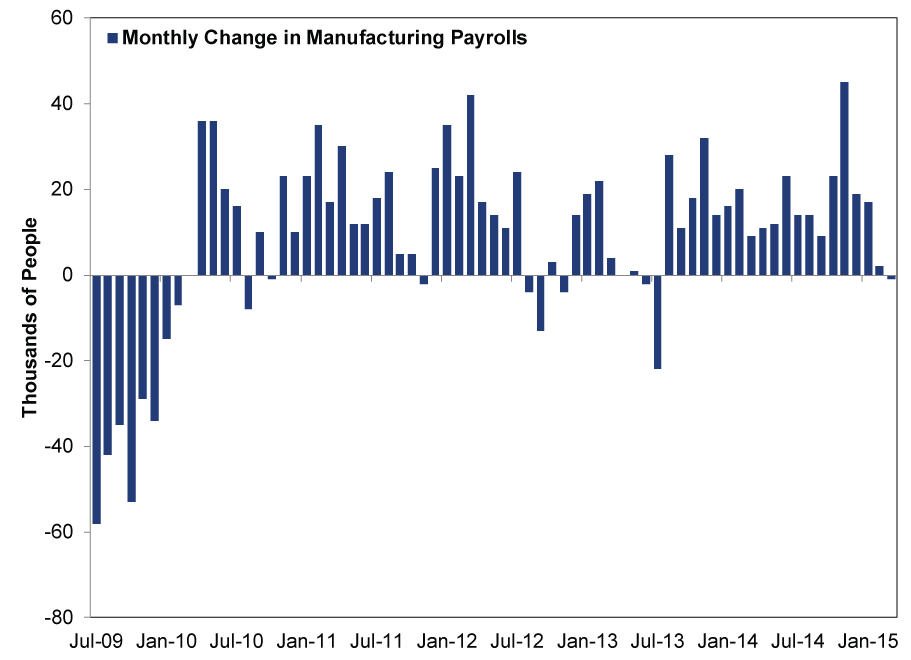

As for the strong-dollar-killing-job-growth chatter, we'd chalk that up as an overreaction to a 1,000-person drop in manufacturing employment. A thousand jobs is not a big number when scaled against America's economy. Neither, for that matter, is 11,000-the number shed in the mining and logging industry (which includes oil and gas extraction and related support activities) in March. Here is how manufacturing job growth has looked during this expansion:

Exhibit 5: Manufacturing Job Growth

Source: FactSet, as of 4/6/2015. Monthly change in manufacturing payrolls, July 2009 - March 2015.

By the way, the dollar was weaker than it is today during those 2010, 2012 and 2013 manufacturing employment blips.

Whether or not March's dip is a blip, it's a bridge too far to blame the dollar. The Bureau of Labor statistics doesn't separate exporters, so there is no way to prove weaker overseas revenues drove firms to cut headcount here. What if firms cut back because Q1's nasty weather hit demand temporarily? What if they were responding to the West Coast Ports labor dispute, which bottlenecked trade for a couple months, creating inventory backlogs? What if 1,000 manufacturing workers got tasty managerial or service-sector jobs and firms were slow to backfill because the supply of available workers is dwindling? These are all plausible, simple alternate theories, and none require convoluted mental gymnastics to accept.

Besides, even if the stronger dollar does turn out to be the culprit, this isn't an automatic negative for stocks. This will sound callous, and we're sorry, but owning a stock is not owning a share in future employment. Stocks are shares in companies' future earnings. If firms cut headcount a bit to tame costs when they fear revenues are slowing that is generally good for earnings. Business can be a cold, efficient place. Investing often requires folks to turn off their hearts and value cold efficiency. If you own a US-based multinational, and you worry the stronger dollar might hurt their overseas revenues more than it helps cut their import costs, you want them to do what's necessary to protect profitability. Trimming expenses-especially if it involves boosting productivity, not trimming output-is logical. Again, that doesn't mean it is necessarily a thing right now! Maybe it is, maybe it isn't, and it will take time to gather evidence either way. But if it's a thing, for stocks, it doesn't have to be a bad thing. It can be good.

Anyway, we'll learn more about all that as firms announce earnings for Q1 and beyond, but we suspect the strong dollar is as much of a bogeyman today as it was in the mid-to-late 1990s, when the dollar was even stronger and large US multinationals' stocks soared.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today