Personal Wealth Management / Market Analysis

There Was Never a Trump Rally to Trade

Whether up or down, stocks are not tied to whatever passes through the President's head.

With Trumpmania about to reach fever pitch as the greatest reality show on Earth makes its debut-and all the attention it garners (we can't get enough!)[i]-the financial press unsurprisingly continues to connect every market gyration to the President-elect's actions. We documented this phenomenon on the upswing and during the holiday interregnum. Now, with stocks flattening out in the wake of a much ballyhooed Trump press conference and the inauguration nearing, the narrative has flipped. Media is atwitter with fears the Trump Rally has reached its zenith! Hold. Your. Horses. The "Trump Rally" narrative always seemed to us to far exceed what the data supported, and stocks' latest miniscule -0.2% pullback from January 6's all-time high to date[ii] seems like markets being markets.

Trump Isn't Responsible...

Seeing every market move through a Trump lens is an error. Considering his election wasn't even a glimmer in pundits' eyes when stocks rallied from February 2016's correction low, it seems a stretch to presume the rally continuing after the election is all about him. The flat two weeks since a record high likely isn't a Trump phenomenon either. The rally to new highs since the election could well have occurred if Hillary Clinton won. As we said all last year, the motivating force behind last year's rally is falling political and economic uncertainty. While there is no counterfactual, it seems highly likely markets would have rallied no matter who won, even if it were Jill Stein, Gary Johnson or Evan McMullin. Maybe it would have been bigger!

The common factor isn't the outcome-they all have different ideologies that might have led to (marginally) different policies-it's that after markets know who's going to be in the hot seat, they can move on. Markets can discount policies, whether they'll be implemented or not and, if enacted, how effective (or not) they'll be. For the most part, little gets done and what does is watered down. Gridlock is good because more than any particular outcome, markets dislike uncertainty. Gridlock prevents sweeping changes from upsetting the status quo-economic and earnings growth-which stocks have cheered since 2010.

While falling political uncertainty is a plus, what it allows investors to better see is key. Economic growth remains firm, if unspectacular, around most of the globe. Forward-looking indicators point to continued growth. Earnings have improved and expectations are rising, as Energy's drag is waning (another source of falling uncertainty). When it comes to individual stocks, Trump supposedly wields his greatest influence. But don't overstate it. It isn't like Trump is on the board or a major shareholder. Investors buy and sell shares based on companies' prospects. What one guy thinks, even if "leader of the free world," matters less than corporate accomplishments under prevailing market conditions. Heck, even his chosen outlet for these proclamations got no Trump bump in corporate results. In short, pay attention to fundamentals, not media hype and presidential tweets.[iii]

...Not Just for the US, but the World!

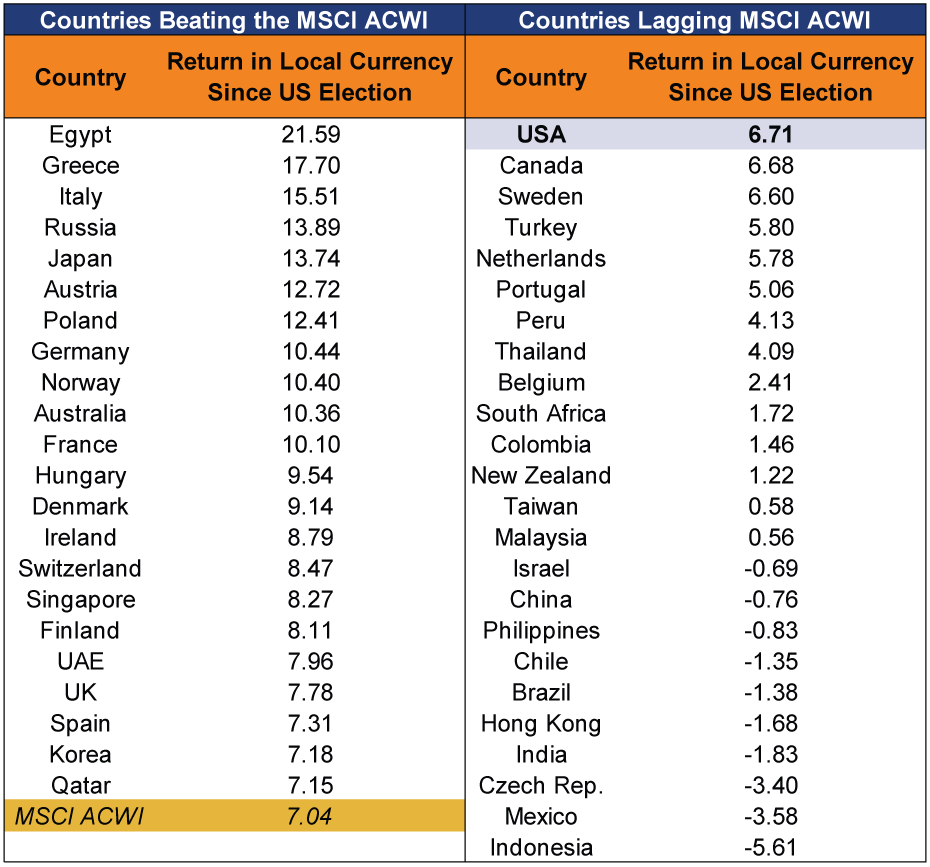

Of course, Trump has some agenda-setting control over the US economy, so it's plausible he has a degree of influence over US stocks. But besides making war and potentially affecting trade, the theory the global economy bends to his whim stretches credulity. He seems likely to face hurdles getting the US political system to fall in line outside a very limited area under the executive branch's purview. So if this rally is all about Trump, then one would presume the US would top rankings of country returns since the vote. Exhibit 1 shows you where America stands among the 46 developed and Emerging Markets nations in the MSCI All-Country World Index when you denominate returns in local currencies (to eliminate currency conversion skew).

Exhibit 1: America's Rally Middling Since Election

Source: FactSet, MSCI All-Country World Index local currency total returns by country, percent change 11/8/2016 - 1/13/2017. Click here to see a version that is denominated in US dollars. To spoil the surprise, the US outperformed the ACWI, but ranks 12th.

Yet America isn't even close to the top.[iv] Sure, you could make the case-"NAFTA, bad!"-looking at Mexico, but then what about Canada? Or, if Russia is a prime beneficiary of Trump's presidency given his allegedly budding bromance with Pootie-Poot, shouldn't Europe have suffered as a result? (Plus, Russia was beating long before the vote, tied to oil's rebound.) Europe's largest economies and markets-Italy, Germany, France, the UK and Spain-have all outperformed the world and the US. What will it mean if/when US stocks continue to lag Europe?[v] Potentially less about Trump, and much more about underlying economic reality and what markets have priced in.

Searching for Meaning in Bouncy Times

While humans are great at seeing cause and effect, even where they're absent, the media is positively desperate to put a narrative on everything, especially when it comes to markets. When the big, click-receiving story of the year happens, rest assured the media will want to connect those dots. But following the media narrative can be extremely detrimental to investors' long-term success.

Trump's election and tweets have affected certain stocks, but only drive sentiment momentarily. Stocks' rally after the election just continues the post-Brexit, post-correction rally from February, with industry leadership mostly unchanged. So the "buy the rumor, sell the news" narrative the media is trying to paint around Trump's inauguration gets the whole story wrong. Mistaking market movement for Trump's failure (to do anything) before he's even president is an exercise in myopic extrapolation that is dangerous to your financial health. That said, journalism's "give 'em what they want" attitude can be a useful sentiment gauge for conventional wisdom. The fact widespread fears over a Trump presidency remain prevalent suggests this non-Trump rally has further to go.

We know (we know!) the fallacy is hard to shake. Everything right (or wrong) is because of him. That's fine for pundits selling papers, but for clear-thinking investors, don't succumb to the Trump trade.

[i] Yes, we can.

[ii] Source: FactSet, S&P 500 price return, 1/6/2017 - 1/18/2017.

[iii] And follow @kennethlfisher!

[iv] You'll notice that Egypt and Greece have led since the election. This is due to their ancient Coptic connection presaging Donald J. Trump as the next Alexander the Great. (Not really.)

[v] For more, see Ken Fisher's latest commentary, "Trump Will Struggle - but Global Stocks Will Boom."

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today