Personal Wealth Management / Market Analysis

Thinking About Bonds

As the Fed eyes QE tapering, how should investors think about bonds?

Ben Bernanke takes a thoughtful pause during his June 19 press conference, when taper talk kicked off in earnest. Photo by Alex Wong/Getty Images.

With interest rates rising lately amid the Fed’s QE tapering whispers, we’ve seen some chatter about bonds no longer being “safe.” It’s a complete misperception, in our view, considering bonds have never been inherently safe. No investment with any degree of return is. So what is the right way for investors to think about bonds? In our view, instead of seeing them as a potential safety net, investors should view them as one potential answer to the age-old question: What are my long-term goals, how long does this money need to work for me, and which asset allocation gives me the best chance of getting where I want to go over time?

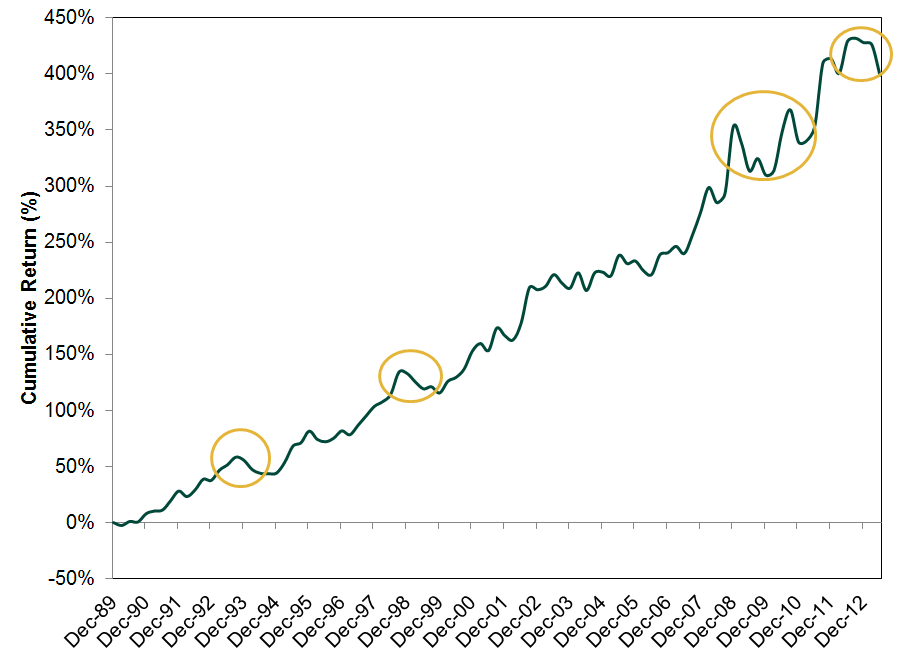

It is easy to see why bonds have their safe haven reputation. Because they provide a steady coupon payment, it is all too easy for investors to ignore their inherent risks. But bonds are volatile and subject to periods of decline, just like stocks. As Exhibit 1 shows, US Treasurys—one of the least volatile categories of bonds—have still endured their fair share of pullbacks over the past 20 years.

Exhibit 1: US 10-year Government Bond Total Return Index

Source: Global Financial Data, as of 7/12/2013

To get any sort of return over time, you have to accept some degree of risk, and bonds are no different. Bonds typically have lower expected short-term volatility than equities, but they’re not risk-free. For example, they have interest rate risk, inflation risk, default risk, maturity risk and reinvestment risk, with the magnitude of these risks varying among different types of bonds. US Treasurys, for example, are widely perceived as having the lowest default risk in the world—hence their lower volatility and relatively lower yields. Investment-grade corporates are less risky and lower-yielding than their junkier counterparts. No bond is inherently “safer” than another—each merely has different expected risk and return characteristics.

Looking at bonds as a potential source of “safe” yield is folly. They can be a very useful component in a long-term investment strategy, but not as a safety net. This is an easy trap to fall into though. For example, fixed income investors might grow impatient with ultra-low US Treasury yields and search high and low for an alternate “risk-free” asset with higher-than-market-level yields. This doesn’t exist—yield is by definition compensation for the amount of risk taken—but many products (wrongly, in our view) claim to offer it. Investors treading this perilous path could veer from their long-term goals—and, potentially, into costly, illiquid products.

Instead, investors should consider their long-term goals and whether bonds might play a role in reaching them over time. For many investors, bonds can play a key role. For example, used in concert with equities, they can help reduce a portfolio’s expected short term volatility, aiding investors with ongoing cash flow needs or those simply looking to smooth out some of the equity market’s short-term ups and downs.

That’s true over time regardless of bonds’ near-term outlook. That said, while interest rates may have recently risen, they appear unlikely to spike in the near term. The Fed has long suggested rates will stay low until unemployment improves to 6.5% and inflation accelerates to 2% y/y. At the moment, the unemployment rate remains well above the Fed’s stated goal and inflation remains comfortably below its target—so the Fed likely maintains the status quo for some time. Even when the Fed begins tapering QE, rates likely won’t spike overnight—just as gilt yields didn’t spike in the UK after the BOE stopped purchasing them in late 2012. Recent yield volatility, in fact, could be bonds pricing in QE’s eventual end. Bond markets, like stock markets, are forward-looking.

So while bonds aren’t inherently “safe,” their near-term risks have been vastly overstated, in our view. And more importantly, over time, bonds can be a useful tool for many investors, depending on their long-term goals, time horizon, cash flow needs and other similar factors.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today