Personal Wealth Management / Market Analysis

Thinking About ‘Selling in May’? Think Again.

Your friendly annual reminder to put this seasonal saw to bed.

With April almost in the books, stocks have added to their fast start to 2019. As pundits have documented well in recent days, US stocks are off to a rip-roaring start this year—up 17.4%, the best start for the S&P 500 since 1987.[i] With many still smarting from last year’s disappointing returns, skeptics abound. The strong returns haven’t quelled that, with many suspecting the rally won’t last. Some think stocks’ rise won’t just slow—it might reverse. With May right around the corner, it may seem conditions are ripe for the ol’ seasonal adage—“Sell in May and Go Away”—to work this year. While short-term negative volatility is always possible, we think such calendar-based tactics are fatally flawed. History shows markets don’t move with the calendar and seasons—neither should investors, in our view.

“Sell in May” has its origins in British markets, referring to light trading volumes during the summer months as brokers took their holiday. These days, though, it seems most “Sell in May” proponents use the Stock Traders’ Almanac definition, which argues market returns from April’s end through October’s end are weak—so investors should leave and return during the stronger period.

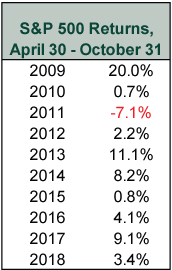

However, both recent and historical data toss cold water on this thesis. Consider the S&P 500—which we use here because it provides the longest reliable historical market dataset. Since the bull market started in March 2009, the stretch from April’s end through Halloween has been negative only once: 2011. That particular period featured a big summertime correction, with fears roiling sentiment in both the US (e.g., the US credit-rating downgrade and debt-ceiling fight) and Europe (e.g., eurozone sovereign debt crisis). While “Sell in May” would have worked nicely that one year, the other nine periods were all positive. (Exhibit 1) For long-term, growth-oriented investors, this means selling in May spelled missed gains in 9 of this bull’s 10 years—unwise, in our view.

Exhibit 1: Sell in May’s Spotty Record

Source: FactSet, as of 4/25/2019. S&P 500 Total Return Index, reflecting returns from 4/30 – 10/31 for 2009 – 2018.

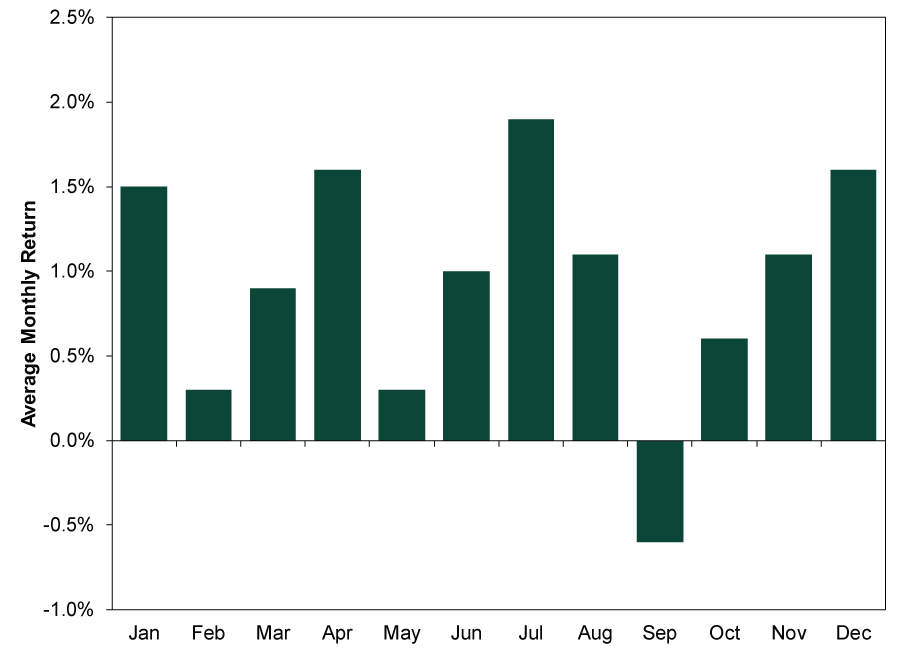

This doesn’t apply just to the current bull market. Going all the way back to 1926, the S&P 500 enjoyed an average 4.2% total return from April 30 – October 31.[ii] That is less than the October – April stretch, but it is positive, which seems a strange thing to sell and avoid. Seen differently: Selling in May would have “worked”—as in, dodged declines—25 times from 1926 – 2018.[iii] If you like percentages, that is a 27% success rate. For the glass nearly three-quarters empty folks, that is a 73% failure rate. Plus, selling in May would mean missing out on July—which has the strongest average monthly return. (Exhibit 2)

Exhibit 2: S&P 500 Average Monthly Returns

Source: Global Financial Data, Inc., as of 4/10/2019. S&P 500 Total Return Index, average monthly returns, 12/31/1925 – 3/31/2019.

We aren’t saying you should own stocks in July because of its stronger historical numbers. But this also highlights the folly of “Sell in May.” If the past was predictive, why not just cherry pick the strongest months to own stocks and stay out during the weakest months? Here is why: Markets just don’t work that way.[iv]

Seasonal adages ultimately argue past performance tells you something about the future. Yet markets are efficient discounters of widely known information, in our view, which means they have already dealt with and moved on from the past. Instead, markets care about what is coming next, particularly in the next 3 – 30 months. While it is possible seasonal quirks affected stocks in the distant past, when market liquidity wasn’t as robust, that isn’t the case in today’s global marketplace. Any potential advantage from calendar changes has long been priced in.

Of course, maybe Sell in May “works” this year. In short-term stretches, markets can be volatile. A correction—a short, sentiment driven downturn of about -10% to roughly -20%—could strike again at any time. However, coincidence isn’t causality and, whatever happens, we are quite sure it won’t be that April showers brought bad May stock returns. Ultimately, we would counsel looking at more meaningful forward indicators. To us, the market drivers underpinning the bull market—skeptical sentiment and a brighter-than-appreciated political and economic reality globally—remain intact. So even if returns are slower and choppier for the rest of the year, 2019 should still be a great overall year for global stocks. To benefit, we believe investors should “stay in May.”[v]

[i] Source: FactSet, as of 4/26/2019. S&P 500 Total Return Index, 12/31/2018 – 4/25/2019.

[ii] Source: Global Financial Data, Inc., as of 4/9/2019. S&P 500 Total Return Index, 12/31/1925 – 10/31/2018. Average return for the six months from April 30 – October 31.

[iii] Source: Global Financial Data, Inc., as of 2/27/2019. Based on S&P 500 Total Return index, monthly, January 1926 – December 2018.

[iv] Also, “Sell in May, return in July, bounce before September, and return after Halloween” doesn’t really roll off the tongue.

[v] We are thinking of having t-shirts made.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today